I really enjoyed listening to this week's feature interview from The Market Huddle podcast. The guest, Robert Mullin, is the founder of Marathon Resource Advisors. The back half of the interview is largely about his specialty, natural resources and commodities, which as many SMI members know, has been an area of particular interest (for me) since late 2020. That said, after writing a lot about the subject from 2020–2022, we haven't written as much about them lately, so it's interesting to get Mullin's current thoughts on that space.

But that's not why I'm highlighting the interview. The first half of the interview touched on several other topics that we have been focusing on quite a bit over the past year or so — specifically, the changing correlations between stocks and bonds, how that is influenced by higher inflation, the impact of the dollar decline earlier this year particularly on foreign/European investors, and how all these factors impact the thinking of those trying to construct portfolios for clients.

I'll touch on a few of these specific points below and unpack them a bit. But the whole interview is well worth the time if you're interested. It's not anything SMI members need to listen to, but I think you'll find it enlightening and worthwhile if you do. I suggest starting at the 15:26 mark of the podcast (it should start there automatically below).

Why bonds aren't as attractive as they used to be

One of the foundational pillars beneath SMI's Dynamic Asset Allocation strategy was that with interest rates having declined so drastically over the prior few decades, bonds would eventually be mathematically unable to provide the same type of support to balanced stock/bond portfolios that investors had grown accustomed to. We were early on that idea, but it was proven out in 2022 when bonds not only failed to cushion the decline of a falling stock market, any exposure to long-term bonds made portfolio losses even more dramatic.

What we didn't recognize a decade ago was the role inflation would play in this changing stock/bond correlation dynamic. From the late 1990s through 2021, whenever stocks fell, bonds tended to rise in value, cushioning the impact for the overall portfolio. In finance terms, stocks and bond prices were negatively correlated during that period (meaning they tended to move in opposite direction). But that 20ish year period was the exception in the historical record — through most of the 120 or so years of decent data we can observe, stock and bond prices have been either positively correlated or uncorrelated.

Our friends at 3Fourteen Research highlighted inflation as the key driver of this changing stock/bond correlation in the research underpinning their Real Asset Allocation model. And it's the first big point Robert Mullin makes in the interview above as well, identifying that historically, when inflation is higher than about 2.5%, the correlation of stocks and bonds flips from negative to positive.

Said simply, when inflation is low, as it was for most of the 20 years prior to 2022, bonds will cushion declines within an equity portfolio. Low inflation gives central banks the leeway to step in and quell market problems without the fear of spiking inflation and crashing bond prices, and investors know this. But when inflation is above 2.5%, that hasn't been the case historically. Given that we haven't been able to get inflation below 2.5% sustainably for the past 3-4 years, this is quite possibly the most important issue facing investors today, given the widespread reliance on big bond allocations to manage portfolio risk.

As I stated yesterday in the August Private Client video (which will be available to Premium SMI members here next week):

"More important than which bonds were owned was the decision to allocate less money to bonds than many advisors (or default target-date portfolios)."

The falling U.S. Dollar

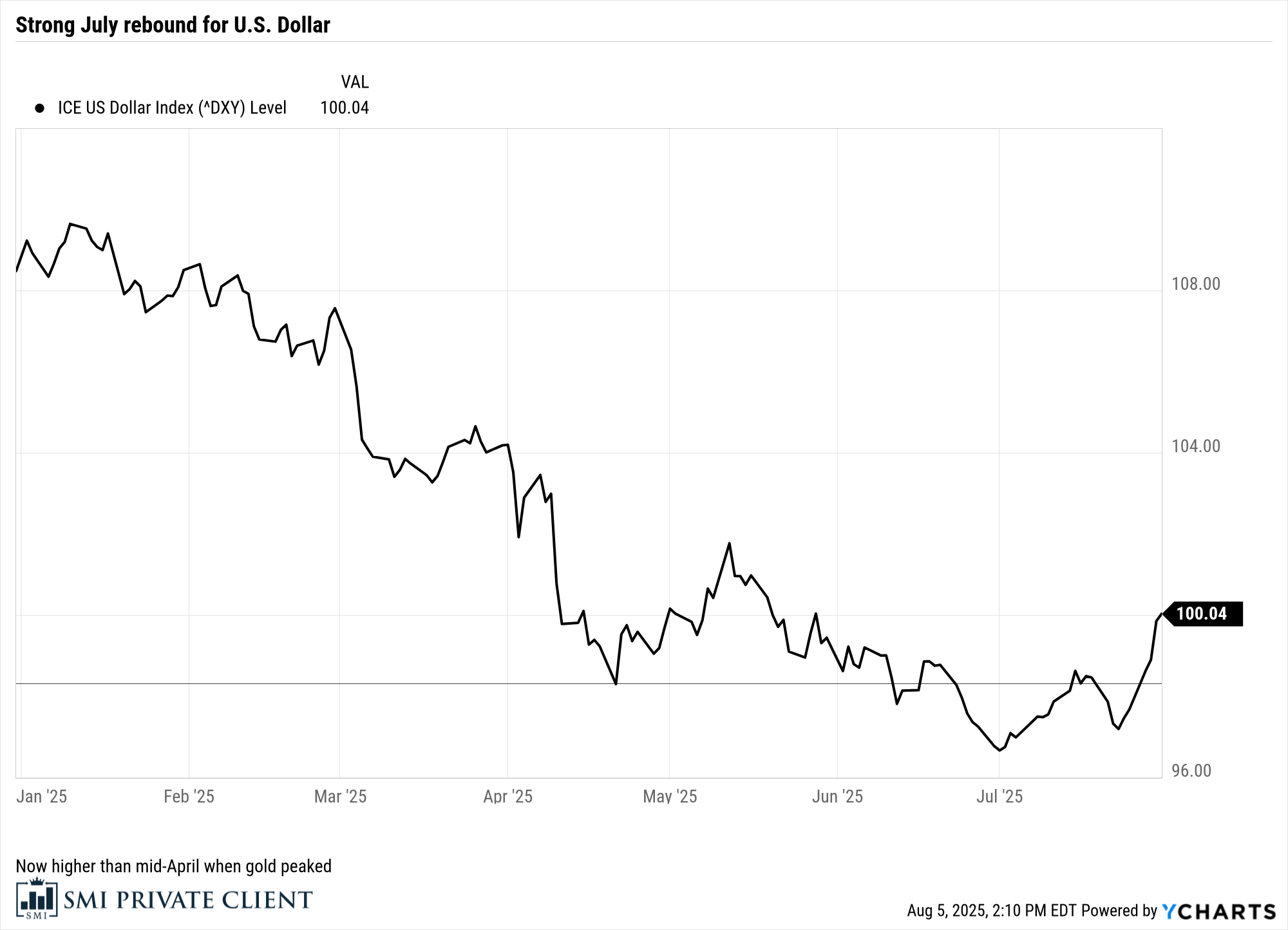

Another theme I've been discussing lately is the impact the falling U.S. dollar has had on various asset classes in 2025. Gold and foreign stocks have been the primary examples here, as they tend to trade in the opposite direction as the dollar. So as the dollar fell -10.9% during the first half of 2025, it wasn't terribly surprising that they were both great, with gold rising +25% and foreign stocks +17% or so.

If we look just at 2025, we can see this dollar decline vividly, as well as the July catalyst for both gold and foreign stocks to take a breather when this dynamic temporarily reversed and the dollar bounced:

That's all well and good, but Mullin pulls the lens back and takes a longer view, explaining that the dollar story since the Global Financial Crisis in 2008 has been that it has tended to be a safe haven during every period of market stress. Plus, as the longer-term chart below shows vividly, the U.S. dollar rose in value pretty relentlessly for many years.

The triple whammy for foreign investors

So far, we've discussed how U.S. stock and bond prices have been negatively correlated in recent years (until 2025), which added an element of safety for investors who bought both. In addition, the dollar was relentlessly rising in value, which both added a further safety element (it tended to spike higher during crises) and an extra return kicker for foreign investors (in the same way the opposite dynamic has boosted returns from foreign stocks for U.S. investors in 2025). The third leg of the stool — huge gains in U.S. stocks since 2009.

Mullin explains that the combination of those three elements led to foreign investors gradually building their allocation to U.S. assets (stocks and bonds) to enormous levels. Which brings us to the jaw dropper of the whole interview at the 19:00 mark.

According to Mullin, during the 2008-09 GFC, foreign investment in U.S. stocks and bonds was roughly $10 trillion. Over the 18 months of that crisis, largely because U.S. bonds rose in value as stocks fell and the dollar rose in value during the crisis, foreign investors only lost roughly -10% in their local currency terms, or about one trillion dollars overall.

Fast-forward 15 years to this year's tariff crash, which lasted roughly two months. Because of the factors discussed a moment ago, foreign investors entered it hugely overweight U.S. assets, to the tune of $47 trillion. This time around, U.S. stocks fell only half as much (~20% vs. 40%+). But because U.S. bonds and the U.S. dollar also fell in value at the same time, foreign investors lost roughly -20% on their U.S. assets during that two-month decline.

Not only is the loss twice as big in percentage terms (-20% in 2025 vs. -10% in 2008-09), but it happened in two months vs. 18 months back then. Factor in the much higher level of assets, and the total loss was roughly 10x the total amount foreigners lost on U.S. assets during the GFC.

What does it mean?

This has already gotten quite long, so I'll wrap a bow on it. Mullin's contention is that many large foreign investors (especially European, who hold much of the U.S. assets) are extremely slow to adjust their asset allocations. Think turning an aircraft carrier.

But he thinks the implications are fairly stark. When an asset allocator looks at a situation like what transpired for foreign investors in U.S. assets over two months this spring, they're going to come to a simple conclusion: we've allowed ourselves to become too heavily allocated to U.S. assets. From there, it's a relatively straightforward process to start dialing that exposure downward. Whether that occurs by slowing/stopping future purchases of U.S. assets or outright sales isn't clear. But he thinks it could be a noticeable trend going forward, one that really hasn't even started yet.

If true, the implication for SMI members is that it would tend to extend the good performance of foreign stocks. This would be further helped if the dollar were to resume its decline, which would be more likely should the Fed start cutting interest rates this fall (September looks increasingly likely).

More importantly though, it reinforces the broader theme SMI has been hammering since late 2020. The market post-COVID is different than it was for the couple of decades pre-COVID. We need more than U.S. stocks and bonds to navigate this new landscape. Gold, commodities, foreign stocks, new approaches like RAA provides...these are excellent complements to our U.S. stock/bond core portfolios.

If you listen to the interview (which goes to roughly 1:09:00), I'll be curious to hear what you think. Drop a comment below.