Imagine going back in time to evaluate a stock portfolio on Dec. 31, 1999. Over the prior five years (1995-1999), foreign stocks have performed well, nearly doubling in value (+95%). But then you look at your U.S. stocks, which have gained 2.5 times as much (+244%)!

That huge performance disparity caused many global investors to pile into U.S. tech stocks during the dot-com bubble. Alas, from the dot-com bubble peak in March 2000, performance for these classes flipped back the other way. Over the next 7½ years, U.S. stocks earned a meager +13.5% (total), while foreign stocks were much better, gaining +69%.

Global investors have recently relived a similar, if even more dramatic, setup. Over the past 14 years, U.S. stocks have gained four times more than foreign stocks: +493% vs. +114% (13.6% vs. 5.6% annualized). As during the 1990s’ dot-com bubble, the default decision for many global investors has been to increasingly pile into large U.S. growth stocks.

Catalysts are emerging

The effect of 14 years of U.S. outperformance on stock valuations has been profound. The average weighted Price-to-Earnings (P/E) ratio for the MSCI U.S. Index is 26.5. For the MSCI World ex-US index, it’s just 16.1.

However, as SMI has written countless times, valuation is not a helpful timing indicator. Foreign stocks have been cheap for years now. The valuation gap tells us that if/when investors favor foreign stocks again, the reversal could pack a powerful punch. But it doesn’t tell us anything about when that is likely to happen.

What factors should we be watching for signs of a reversal between U.S. and foreign stocks? SMI has covered some of this ground before, specifically in the January 2024 article, Uncomfortable Regime Shifts. That article explained how the higher inflation environment since COVID has led to rising interest rates. Higher rates make “tangible” businesses more attractive relative to the more “ethereal” tech businesses that thrived during the recent era of ultra-low interest rates. Not coincidentally, the U.S. market is dominated by big tech companies (Magnificent Seven, etc.), while foreign markets are much less heavily weighted toward tech.

That’s a solid over-arching thesis to keep watch on. But as we’ve watched the opening months of the new Trump 2.0 administration with keen interest, other factors have emerged to cause global investors to question their devotion to the “U.S. Exceptionalism” trade that has been the default in recent years.

New administration policies tipping investor preferences?

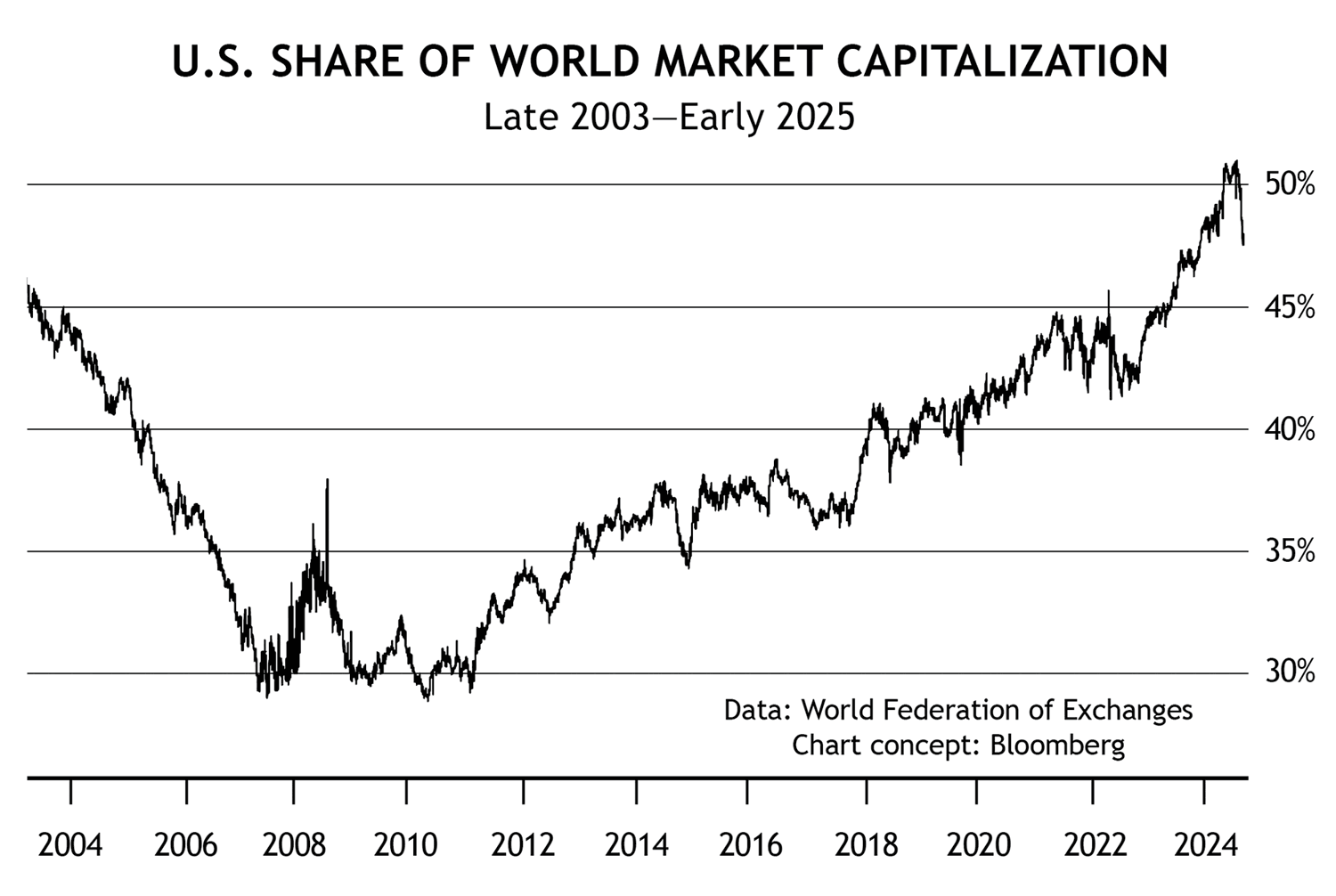

There’s considerable recent evidence that global investors are starting to vote with their feet. February and March have seen significant outflows of U.S. stocks, while foreign stocks are seeing huge inflows. Given the extent and duration of U.S. stock dominance in recent years (see chart below), we’re not willing to say this trend has definitively reversed. But given the massive degree of mean reversion possible after such a long one-sided move, it’s something we’re watching closely.

Click Chart to Enlarge

Here are a few reasons investors may be inclined to favor foreign stocks.

Fiscal impulses are reversing.

Over the past five years (since COVID), the U.S. has run enormous deficits, allowing the government to spend at a rate unprecedented outside of past wars or recessions. U.S. deficits of roughly 7% of our GDP have dwarfed the spending of other countries (most of whom have run deficits of 2-3% of their much smaller GDP levels). The net effect of this gusher of U.S. government spending has been much stronger U.S. economic growth than other countries.Suddenly, and somewhat unexpectedly, this is reversing. Much of the attention since President Trump’s inauguration has focused on cutting U.S. government spending. At the same time, tariff and treaty uncertainty has triggered numerous foreign nations to significantly boost their own plans for government spending.

Put simply, the U.S. is reducing its fiscal spending while the rest of the world is increasing theirs. Government spending has a powerful short-term impact on the companies that receive it and their stock prices.

Growth expectations are diverging.

This is another angle on the prior point. The U.S. avoided a recession when most expected one in 2022-2024. In contrast, Europe and China suffered through recessions and now appear to be emerging out of them. Declining growth here vs. improving growth elsewhere changes the relative attractiveness of high-priced U.S. stocks vs. the relative bargains available overseas.Re-writing the global economic agreement.

For many years, the global economy ran on the following rough equation: the U.S. bought everyone else’s stuff (exports), and then the rest of the world recycled many of the dollars used to buy those goods back into U.S. financial assets (stocks and bonds). That’s arguably been a bad deal for U.S. workers, but it’s been great for U.S. asset prices which have boomed.Now, President Trump has clearly stated his intent to rewrite this equation by increasing U.S. manufacturing. This means less U.S. buying of everyone else’s exports...and by logical extension, less foreign buying of U.S. financial assets.

Interest rate differentials are closing.

Interest rates are impacted by many factors, but one of the biggest is growth expectations. So it’s not surprising that after several years of very low growth expectations in major economies like Europe and Japan (plus China fighting through their own 2008-type financial crisis the past several years), improving foreign growth prospects are causing foreign interest rates to finally rise from the extreme lows of the past decade.More competitive rates at home make foreign investors incrementally more inclined to bring their capital home, rather than seeking higher yields in U.S. assets, including U.S. Treasuries. These global capital flows matter to national economies (money flowing in to a country creates a virtuous cycle for business, money flowing out tends to create challenges). And these flows matter a lot to financial markets.

National pride.

It’s easy to forget that while U.S. financial markets are disproportionately large relative to U.S. population or the U.S. share of global economic activity, the rest of the world combined isn’t far behind. International money managers control vast amounts of capital, assets that could potentially be on the move as the U.S. appears to become a less reliably friendly place for global capital.Opinions vary widely on some of the international decisions being taken by the Trump Administration. But even if they are necessary and appropriate, they clearly are triggering other nations to perceive them along a sliding scale ranging from pulling back from long-time friendships (Europe) to outright economic warfare and threats (Canadians are mad!). In addition to the purely logical points listed here, it wouldn’t be shocking to see emotions play a role in some foreign investors choosing to bring their savings back home

Currency revaluation.

Currency fluctuations are complicated, but here’s a high-level overview. When the dollar is rising in value relative to foreign currencies, foreign investors get a secondary benefit by owning U.S. stocks, as dollar profits are more valuable when converted back into their native currencies. Meanwhile, U.S. investors see the opposite effect from their own holdings of foreign stocks — foreign profits are less valuable because it takes more of them when being converted into stronger dollars.This dynamic flips when the dollar is falling relative to foreign currencies — foreign investors become relatively less enthused by U.S. returns, while U.S. investors get a boost from foreign stock returns.

Many factors impact the value of currencies, so we don’t want to oversimplify here. But generally speaking, lower U.S. growth should lead to lower interest rates. Higher foreign economic growth should lead to higher foreign interest rates. These trends appear to be contributing to the dollar’s roughly -6% decline in value relative to foreign currencies since peaking in early January. The dollar decline has provided a recent tailwind to U.S. investors owning foreign stocks while potentially incentivizing foreign investors to reduce their holdings of U.S. stocks.

Broader options are a good thing for SMI strategies

The factors we’ve reviewed here help explain why President Trump and Treasury Secretary Bessent keep repeating the idea that an adjustment period is required for the U.S. economy and that some pain may be ahead for U.S. asset prices. Starting points matter a lot in investing, and the reality is U.S. markets began 2025 with some of the highest valuations ever. In contrast, many foreign markets have very attractive valuations after being largely ignored for years.

Even if a rebalancing between U.S. and foreign markets is underway, it’s difficult to know whether this will be a rapid repricing vs. a trend that unfolds gradually. Either way, the SMI strategies will monitor this via our trend and momentum processes. Those processes led DAA into foreign stocks at the end of January, which has helped blunt the recent correction in U.S. stocks. (DAA’s foreign stock holding was up +11.2% year-to-date through March 25, while the S&P 500 was down -1.5%.) This month, Stock Upgrading is buying a new foreign stock fund for the first time since December 2023.

Importantly, this isn’t the first time SMI has navigated a potentially significant trend shift away from large U.S. stocks and into foreign stocks. The years following the dot-com bubble saw huge outflows from large U.S. growth stocks that went into other parts of the market, including foreign stocks. Those years were some of SMI’s strongest relative performance years ever.

The simple fact is that it’s difficult for active management to outperform when the biggest U.S. growth stocks are beating every other investment type by a wide margin. In contrast, active management tends to thrive when market activity broadens out to include foreign, small company, and value-oriented stocks. It’s too early to say definitively the trends have shifted in this direction, but the recent pickup in foreign stock returns has certainly grabbed our attention.