Borrowing money comes at a cost, and not just in dollars and cents. As Proverbs 22:7 warns, “The borrower becomes the lender’s slave.” Unfortunately, high prices and widespread access to credit don’t discourage debt servitude. They encourage it.

Consider the housing market. Today, only about one in 20 mortgages is a 15-year loan, down from roughly three in 20 a decade ago. Even though 15-year loans usually have a lower interest rate than the more common 30-year mortgage, buyers have increasingly opted for the lower monthly payments of a 30-year loan.

With U.S. home prices up nearly 25% since 2021, federal policymakers recently floated the idea of lowering monthly payments by introducing 50-year home mortgages. So far, the Trump administration hasn’t strongly promoted the idea. However, Bill Pulte, director of the Federal Housing Finance Agency, says it is among “30 to 50 different options” the White House is considering to address housing affordability.

Supporters of 50-year mortgages argue that lower monthly payments would help potential buyers who can’t afford a 30-year loan start on the path to homeownership and wealth building. Opponents of the idea argue that the interest paid on a 50-year loan would greatly slow the buildup of equity to the point that homeowners with 50 years of mortgage payments might hardly be considered “owners” at all for decades.

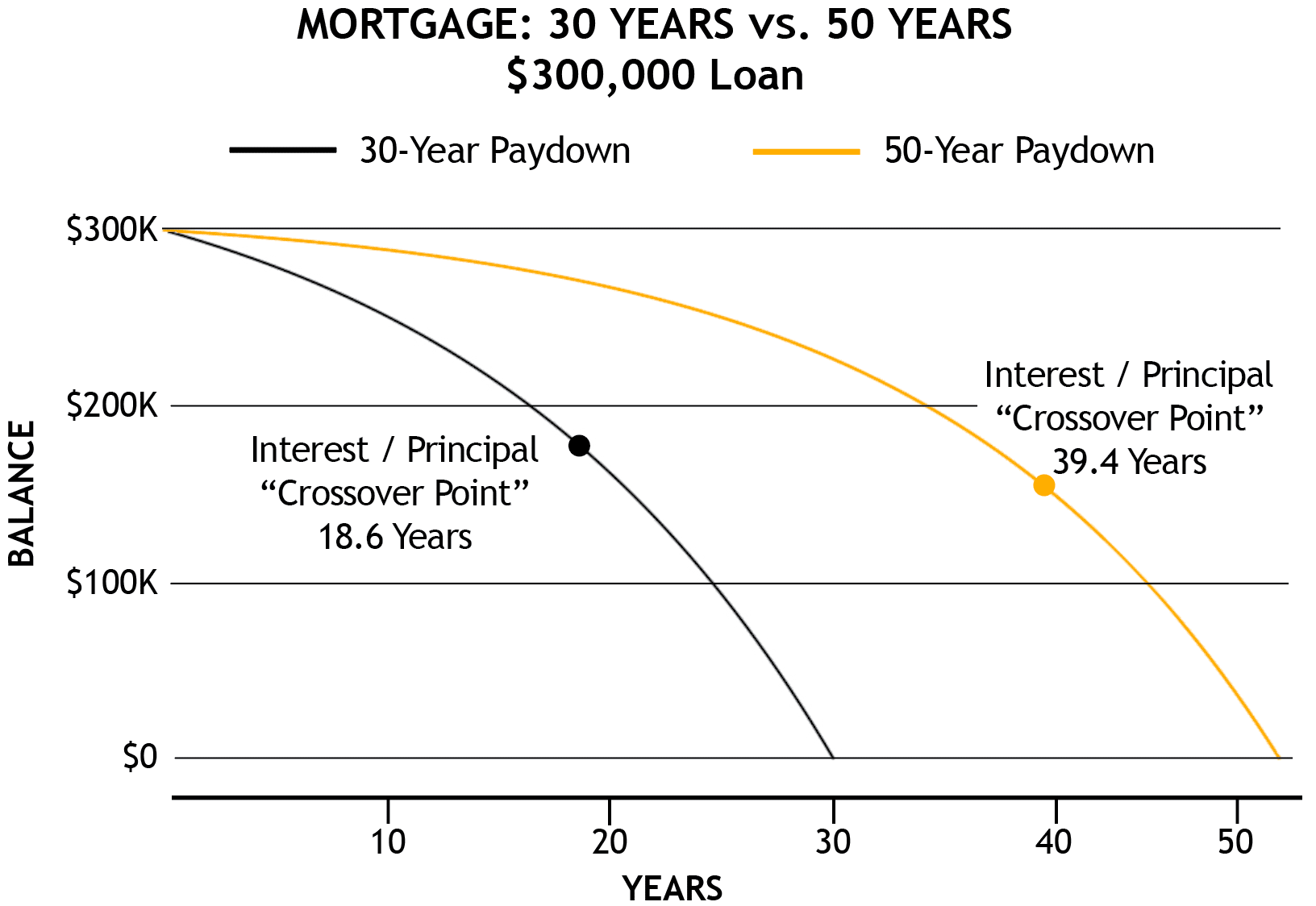

Look at the graph below, which compares the paydown of a 6.5% 50-year loan with that of a 6.0% 30-year loan (longer loans usually have higher rates than shorter loans because lenders face greater risk). The starting principal in each case is $300,000. Monthly payments on the 50-year loan are roughly $1,691, excluding taxes and insurance. The majority of each monthly payment would go toward interest for the first 39 years.

In contrast, the “crossover point” — when principal repayment begins to exceed interest payments — occurs at 18 and a half years on a 30-year mortgage. This is true even though the monthly payment on the 30-year loan is only $108 more than for the 50-year loan. Overall, the holder of the 50-year mortgage would pay $714,690 in interest, more than twice the interest paid on the 30-year mortgage.

Critics of 50-year mortgages point to a broader issue, too: If extended mortgages attract more buyers without a matching increase in housing supply, the laws of supply and demand would push home prices up, making it more difficult for policymakers to meet affordability goals.

Drive now, pay later

While longer-term mortgages remain mostly hypothetical, extended-term car loans are a reality. Once-common four-year and five-year car loans are becoming increasingly rare. (Today, the average loan term is between five and six years, even for used cars.) And, according to the automotive information company Edmunds, one-fifth of new-car purchases now involve terms of at least seven years.

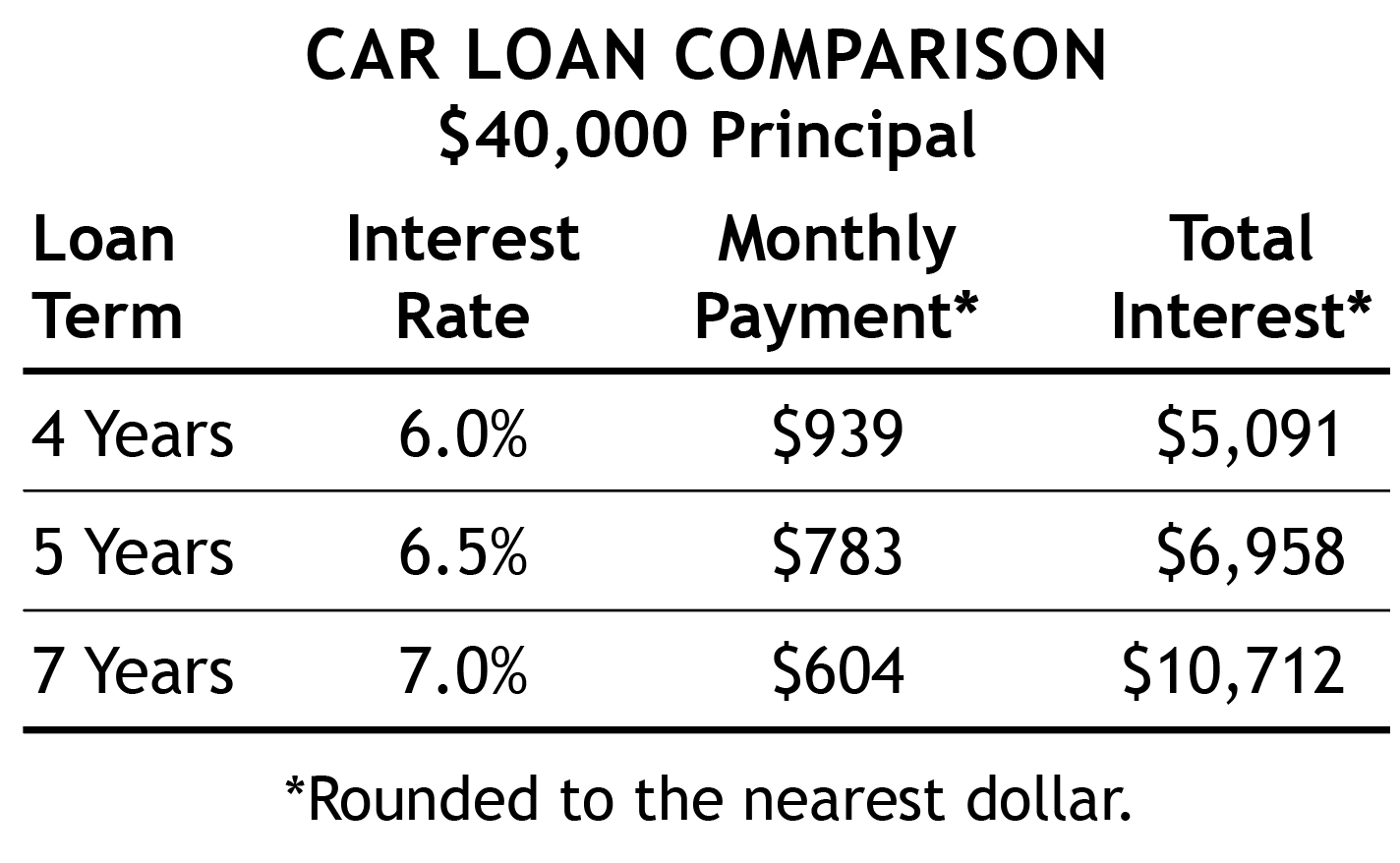

Longer-term loans are promoted as offering consumers a clear benefit: smaller monthly payments. Take, for example, the purchase of a new automobile. With the average price of a new car now at roughly $50,000, according to Kelly Blue Book, it is common for a new-car buyer to finance at least $40,000 of the purchase price. Assuming a 6% interest rate, a buyer who financed with a four-year loan would have a monthly payment of about $939. In contrast, the payment on a seven-year loan at a 7% interest rate would be $604. That’s a monthly “savings” of $335.

Unfortunately, those “monthly savings” come at a much higher total cost. As shown in the table on the right, the seven-year borrower would pay about $10,712 in interest, compared to roughly $5,091 for the borrower with a four-year loan — a $5,621 difference in financing costs.

Not only do car buyers who choose longer loans pay much more interest, they also face greater risk. Since automobiles depreciate quickly, borrowers with large loan balances and extended payoff periods often find themselves “underwater” or “upside down,” meaning the loan balance owed is more than the car is worth. If the car is totaled in an accident, the insurance payout might not cover the remaining balance. The shortfall, possibly amounting to thousands of dollars, would be the borrower’s responsibility. (Some lenders require borrowers to purchase additional “GAP” insurance, which covers the difference between the value of a vehicle and any balance still owed.)

According to Edmunds, the average amount owed on upside-down car loans reached $6,905 in 2025. Additionally, a record 24.7% of recent trade-ins involved vehicles for which buyers still owed more than $10,000. In most cases, “negative equity” on a trade-in is rolled into another car loan, continuing the cycle of long-term auto debt.

Once you sign…

The “smaller monthly payments” of a longer-term loan may seem like an attractive option if you’re financially stretched. But once you sign on the dotted line, the reality will be ongoing payments that continue month after month, year after year, with very slow progress toward getting out of debt.

As Proverbs 22:7 makes clear, debt is a type of servitude. Remember that when deciding how much debt to take on and for how long.