Is it more financially advantageous to buy a place to live or rent one? The answer can be elusive. However, in light of higher interest rates, steeper home prices, limited availability, and the larger standard deduction introduced in the 2018 tax law, many of today’s would-be buyers are opting to rent instead of buy.

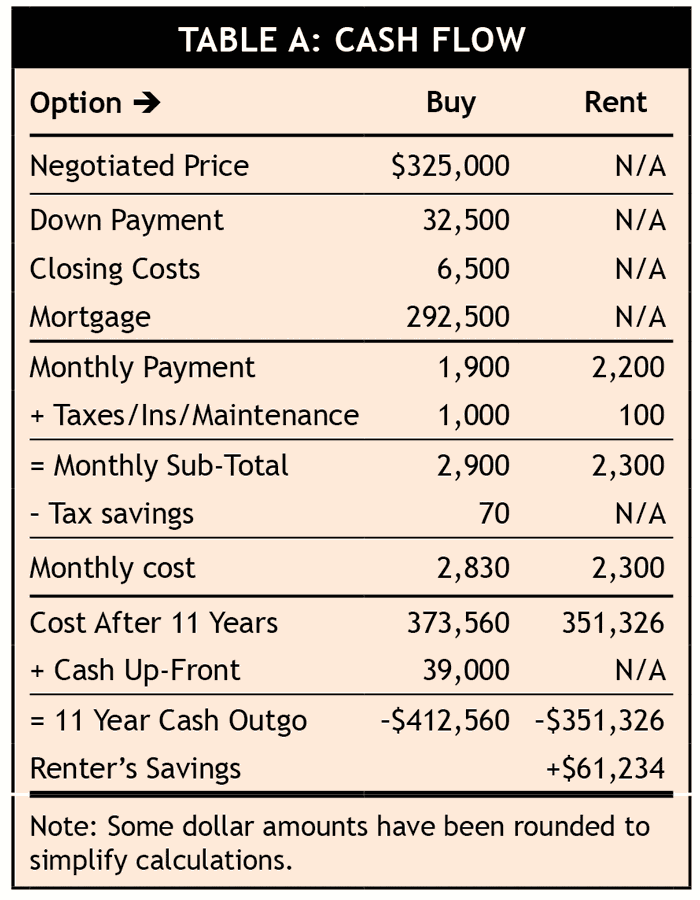

Here’s a hypothetical case. Hank and Hannah Homeseeker rent an apartment for $2,200/month. However, they have their eye on a $325,000 house. They’d like to know if taking the homeowner plunge would be a better use of their money.

Many variables are at play (described below and shown in Table A):

Mortgage Rate

Hank and Hannah could get a 30-year fixed-rate loan at 6.75%, close to the national average as of early 2025.Up-front Costs

They can afford to put 10% down ($32,500) and cover $6,500 in closing costs. So, their upfront outlay would be $39,000 and their monthly mortgage payment would be about $1,900.Taxes/Ins/Maintenance

Initially, Hank and Hannah would budget $1000/month. (That amount will change over the years, but we’ll keep it static to make the calculations easier.) That $1,000 includes property taxes amounting to 1% of the purchase price or $325 per month; homeowner’s insurance of $275 per month; $300 per month for maintenance and repairs; and roughly $100 per month for private mortgage insurance (PMI) — since their down payment is less than 20% of the purchase price.Time Frame

We’ll assume that if the Homeseekers buy, they’ll stay put for at least 11 years. Why 11? According to real estate company Redfin, that’s roughly the average number of years homeowners remain in a given home. That is also slightly less than the average time it takes to break even on the transaction costs (down payment and fees) related to a home purchase, assuming the down payment is 10% of the purchase price.Tax Implications

Other than $10,000 in annual charitable contributions, the Homeseekers have had no other potential sizable tax deductions, so they’ve been taking the standard deduction (currently $30,000). If they buy a house, they’ll be able to itemize deductions. Instead of using the standard deduction of $30,000, they could deduct $37,000 ($10,000 in charitable contributions, roughly $19,000 in mortgage interest in the first year, and state/local taxes of $8,000).

Given their 12% tax bracket, this additional $7,000 in deductions ($37,000 minus the previously used $30,000 standard deduction) would save $840 in the first year, or roughly $70 per month, in taxes. That’s not a big savings, and the amount will decline as the years go by, but we’ll keep it static for this example.

Renting, of course, doesn’t come with a property tax bill, and maintenance and personal-property insurance costs are less for renters than homeowners. We’ll assume monthly expenses of $50 for renter’s insurance and $50 for maintenance. Unfortunately, the cost of rent tends to rise each year, so we’ve built in a yearly rent increase of 3.0%. (The “Cost After 11 Years” in Table A reflects those increases.)

After crunching the numbers, the Homeseekers learn that their monthly housing cost — at least initially — would be $530 more if they bought than if they continued renting ($2,830 vs. $2,300). At the end of 11 years, their Net Cash Outgo from owning (including down payment and closing costs) would be $61,234 greater than if they had rented.

Owning builds equity – maybe

Of course, home ownership has upsides that renting lacks. For one thing, a fixed-rate mortgage acts as a protection against inflation. Unlike rent, the monthly principal-and-interest payment will not increase (however, there may be increases in taxes and the cost of insurance).

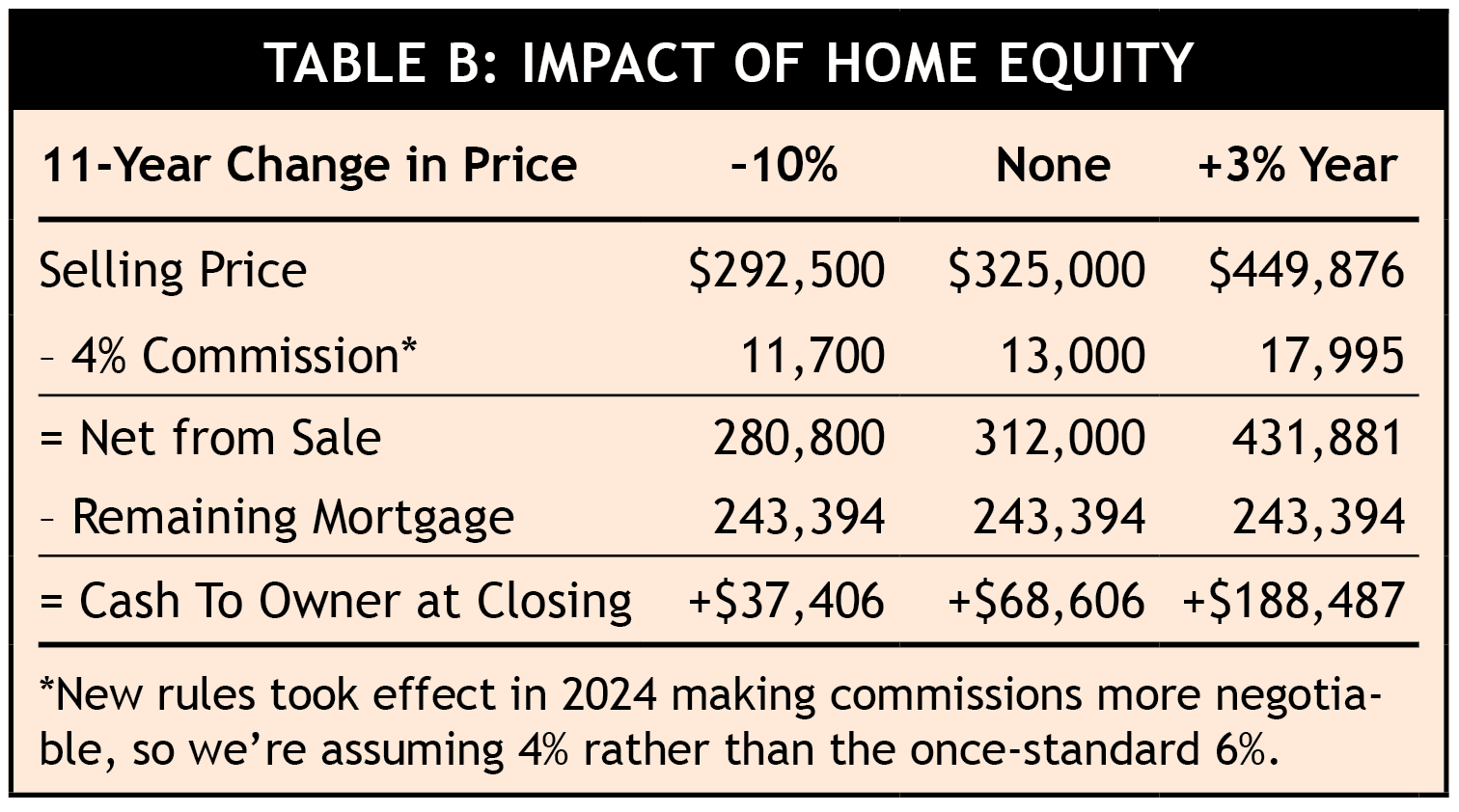

Another upside is that a homeowner can build equity as the mortgage is paid down and the property’s value goes up. Unfortunately, there is no guarantee a house will appreciate.

Table B presents three appreciation-related scenarios, ranging from negative to static to positive (housing appreciation can vary widely by property type and location). The “–10%” column assumes the Homeseekers buy a property that doesn’t appreciate. In fact, after 11 years, a fair price for their house is 10% less than their original purchase price. Ouch.

The “None” column assumes their home’s value holds steady in dollar-amount terms, although it fails to keep up with inflation. After 11 years, they could sell the house for the same price they agreed to when they bought it.

The final column in Table B assumes a better outcome — a steady (though not exorbitant) appreciation. The perceived value of Hank and Hannah’s house grows annually by 3% (slightly less than the national average increase over the past several decades). Over 11 years, the result is a total price gain of 38.4%.

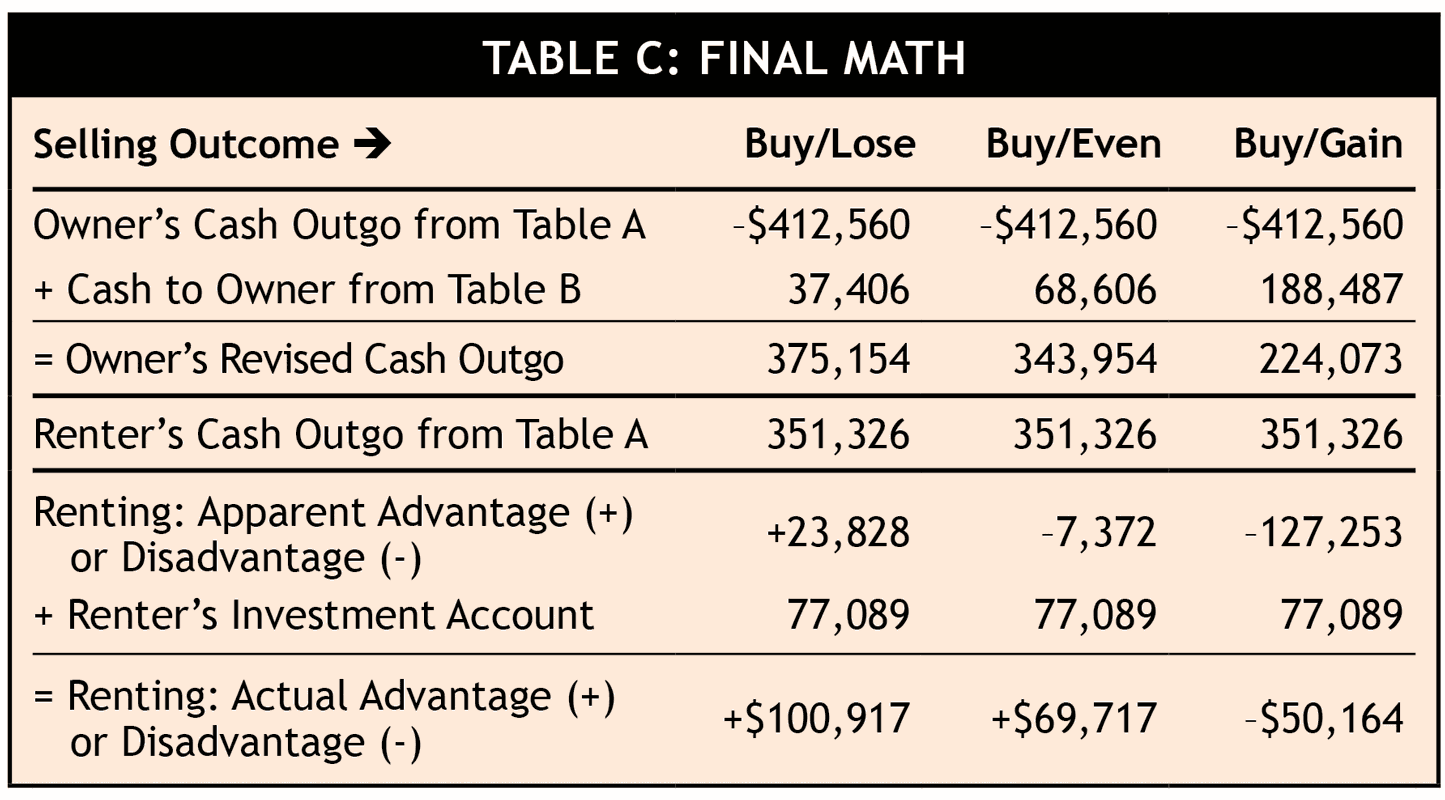

Let’s look now at the final math, which is shown in Table C nearby. If the Homeseekers suffered a 10% loss in value, at closing they would receive non-taxable proceeds of $37,406 after paying off the remaining mortgage. (Married couples filing jointly typically can exclude up to $500,000 of capital gains from the sale of their primary residence. For singles, the exclusion is $250,000.)

The proceeds would partially offset their 11-year Cash Outgo of $412,560, resulting in a Revised Cash Outgo of $375,154 (see Table C). Since this is more than the Cash Outgo for renting during those 11 years ($351,326), renting would cost less than buying under this “Buy/Lose” scenario.

Now, suppose the Homeseekers could sell their house for the same price they paid for it. In such a case, they could pay off the remaining debt and walk away with non-taxable proceeds of $68,606, resulting in a Revised Cash Outgo of $343,954 (see “Buy/Even” column) — slightly better than renting, assuming they don’t have a costly home repair during the 11 years.

The “Buy/Gain” column reflects the steady appreciation that allows Hank and Hannah to sell their home for nearly $125,000 more than their original purchase price. After paying off the mortgage, they would enjoy non-taxable proceeds of $188,487.

Investing the down payment money

Now, let’s consider one more factor. We’ll assume the Homeseekers decide to continue renting rather than buy. Instead of using $39,000 for the upfront costs of buying, they invest it in a diversified stock portfolio.

With an average annual return of 7%, that investment would grow to $82,089 over 11 years, as noted in Table C. If the money were in a taxable account, Hank and Hannah would incur capital gains taxes on a portion of their earnings. Their effective tax rate would depend on several factors, but we’ll assume about $5,000 would be taxed away, leaving them with $77,089 at the end of 11 years — nearly double what they invested.

Here’s the bottom line of rent-or-buy calculations: If the “Buy/Lose” scenario plays out, the Homeseekers would come out ahead financially by renting rather than buying — even more so if they invest the money they otherwise would have used for a down payment and closing costs. The “Buy/Even” scenario is close to a wash but would favor renting if Hank and Hannah invest the money they would have used for the upfront costs of buying. Only in the “Buy/Gain” scenario would they clearly come ahead by buying (see the bottom line of Table C).

Many moving parts

Future home values are a crucial yet unknowable variable in the rent-or-buy decision. Another unforeseeable factor is the possibility that a home could require significant repairs during one’s years of ownership (paying for a new roof would change the calculation quite a bit).

Another thing that would alter the rent-vs-buy comparison is the property one chooses to rent. A four-bedroom house will likely require much higher rent than a two-bedroom apartment, tipping the scales more in favor of buying.

As for investment returns, they are always unpredictable! A renter who invests money he could have used for the upfront costs of buying has no guarantee his investment will perform well.

More than a financial decision

This article targets only the financial aspects of the rent-or-buy decision. You must consider non-financial factors, such as family size, too. Proximity to work and church is also important.

You may buy because you want to put down roots and have a place to tailor to your liking. Or, you may prefer the flexibility to relocate without dealing with the sometimes drawn-out process of selling a property.

If you’re facing a rent-or-buy decision, run your own numbers and prayerfully decide, based on your particulars and assumptions, which path is best for you and yours.