The One Big Beautiful Bill Act, signed into law on July 4, brings good news for many older investors planning to convert money from traditional retirement accounts into Roth accounts.

A new "bonus" deduction for taxpayers aged 65 and up will allow many seniors to transfer more money into a Roth account without moving into a higher tax bracket. The deduction is already in effect, applying to 2025, and also to 2026, 2027, and 2028.

As with any tax matter, there are many details. But the key point is this: The new law offers an extra $6,000 deduction for filers who are 65 or older (whether they itemize or don't itemize their deductions). Married couples filing jointly can get a combined $12,000 bonus deduction if both are 65+.

When combined with the existing standard deduction for older taxpayers, the new deduction allows single filers aged 65 or older who don't itemize to exclude $23,350 of their 2025 income from taxes (up from $17,350 under the previous law). Joint non-itemizers can exclude $46,700 (up from $34,700 previously). Non-itemizers, by the way, account for roughly 90% of household tax returns.

It is important to note that the new deduction starts phasing out for single filers with modified adjusted gross incomes above $75,000 and for couples filing jointly with incomes above $150,000. (More on that below.)

A little more room to maneuver

Roth conversions can be a valuable retirement-planning tool because they help protect future retirement income from taxes. However, the downside is that a conversion is a taxable event. Making a Roth conversion means paying taxes now in exchange for potentially avoiding a larger tax bill in the future.

Money withdrawn from a traditional account for conversion to a Roth is "stacked" on top of other income. Ideally, you want to avoid a situation where converting money pushes you into a higher tax bracket.

Because the new bonus deduction can offset some taxable income from a Roth conversion, it creates "room" for many middle-income taxpayers to convert a larger amount of money without crossing (or perhaps only minimally crossing) the tax-bracket threshold from 12% to 22%.

But wait: For some, conversion costs could go up

Unfortunately, the phaseout provision can make Roth-conversion scenarios more expensive for some higher-income taxpayers than under the previous law.

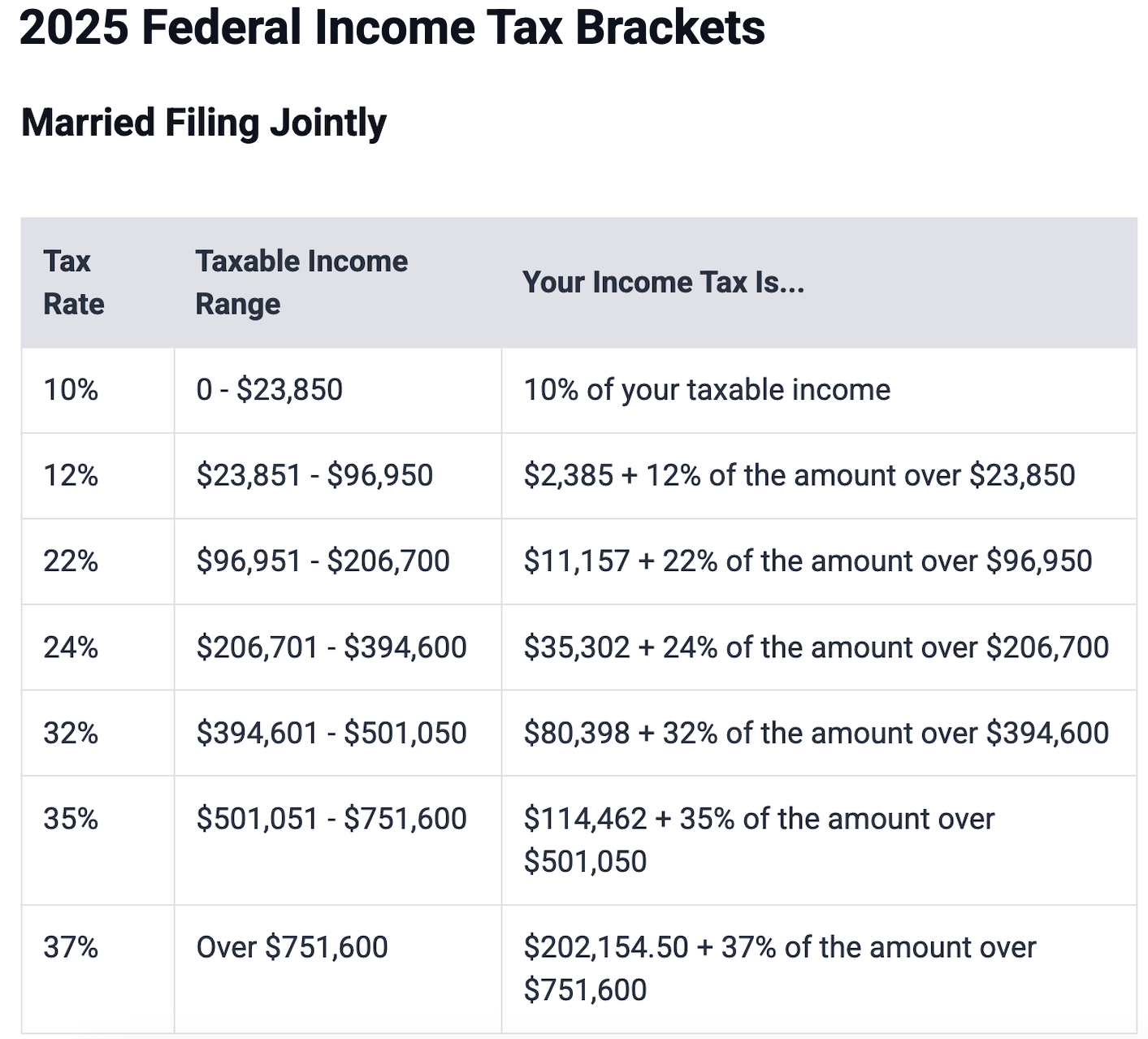

For example, filers already in the 22% tax bracket (which begins at $48,476 of modified adjusted gross income for singles / $96,951 for couples) will face a higher effective tax rate on conversions if the converted amount pushes their total income into the phaseout range for the bonus deduction. When an income ceiling is breached, the bonus deduction is reduced by 6% (12% for couples) of the amount that exceeds the limit.

For example, a single person who exceeds the $75,000 threshold by $10,000 would lose $600 of the bonus deduction. A married couple filing jointly (if both are 65 or older) who went $10,000 past the $150,000 threshold would see their deduction reduced by $1,200.

Financial blogger Harry Sit calculated the tax rate on Roth conversions for those who trigger the phaseout reductions.

If you're single...and you're in the 22% tax bracket, the tax cost for your Roth conversion goes from 22% to 22%-x-1.06 = 23.32%. If you're married and both of you are over 65, it goes from 22% to 22%-x-1.12 = 24.64%.

Roth conversion is always about the tax rate you're paying now versus the tax rate you expect to pay in the future if you don't convert as much.

If you think it's still worth converting at 23.32% or 24.64%, you would continue converting the same amount, ignoring the effect on the senior deduction. If you think it's not worth it to convert at 23.32% or 24.64% (but it's worth it to convert at 22%), you would convert only enough to $75k or $150k AGI to get your full senior deduction.

Act with care

If you're 65 or older and making Roth conversions, the new bonus deduction could help you convert more money at a lower cost over the next four years. However, before you convert, make sure you understand how different parts of the tax law work together.

A large Roth conversion could erode the new bonus deduction, making it less beneficial. Further, boosting your income "too high" could result in higher Medicare premiums.

So do your homework, and if necessary, consult a tax advisor.