A SMI member wrote to us this week with an important warning for investors planning Roth conversions.

I recently went on Medicare and I have to pay a hefty IRMAA surcharge (for both myself and my wife) due to Roth conversions and other IRA withdrawals two years before going on Medicare.

I didn't know these conversions and withdrawals could cost me thousands two years later.

– Carl in Chattanooga, Tenn.

Ouch. Carl got caught in the IRMAA trap.

IRMAA stands for Income-Related Monthly Adjustment Amount. In simple terms, higher-income taxpayers — whether they have traditional Medicare or a Medicare Advantage plan — are required to pay higher premiums for Medicare Part B. IRMAA affects premiums for Medicare Part D, if applicable (Part D is optional prescription coverage).

IRMAA can sneak up on you

IRMAA is tricky in two ways.

If you exceed a government-set income limit by as little as $1, you'll face significantly higher premiums.

"Income" used for IRMAA calculations isn't current-year income or even income from the previous year. Instead, the government determines IRMAA based on "Modified Adjusted Gross Income" (MAGI) from two years prior. In other words, Medicare beneficiaries like Carl in Chattanooga are paying IRMAA surcharges in 2025 based on income earned in 2023.

To understand the surcharge, it is helpful to know that Medicare premiums don't cover the full cost of Parts B and D. Most beneficiaries pay a monthly premium that covers approximately 25% of the actual costs. "The government" pays the remaining 75%.

However, higher-income taxpayers are required to pay considerably more toward actual costs, as The Finance Buff blogger Harry Sit explained in a recent post:

Depending on [their] income, higher-income beneficiaries pay 35%, 50%, 65%, 80%, or 85% of the program costs instead of 25%. As a result, they pay 1.4 times, 2.0 times, 2.6 times, 3.2 times, or 3.4 times the standard Medicare premium.

The threshold for each bracket can cause a sudden jump in the monthly premium amount you pay. If your income crosses over to the next bracket by $1, all of a sudden, your Medicare premiums can jump by over $1,000 per year.

If you are married filing a joint tax return and both of you are on Medicare, $1 more in income can make the Medicare premiums jump by over $1,000/year for each of you.

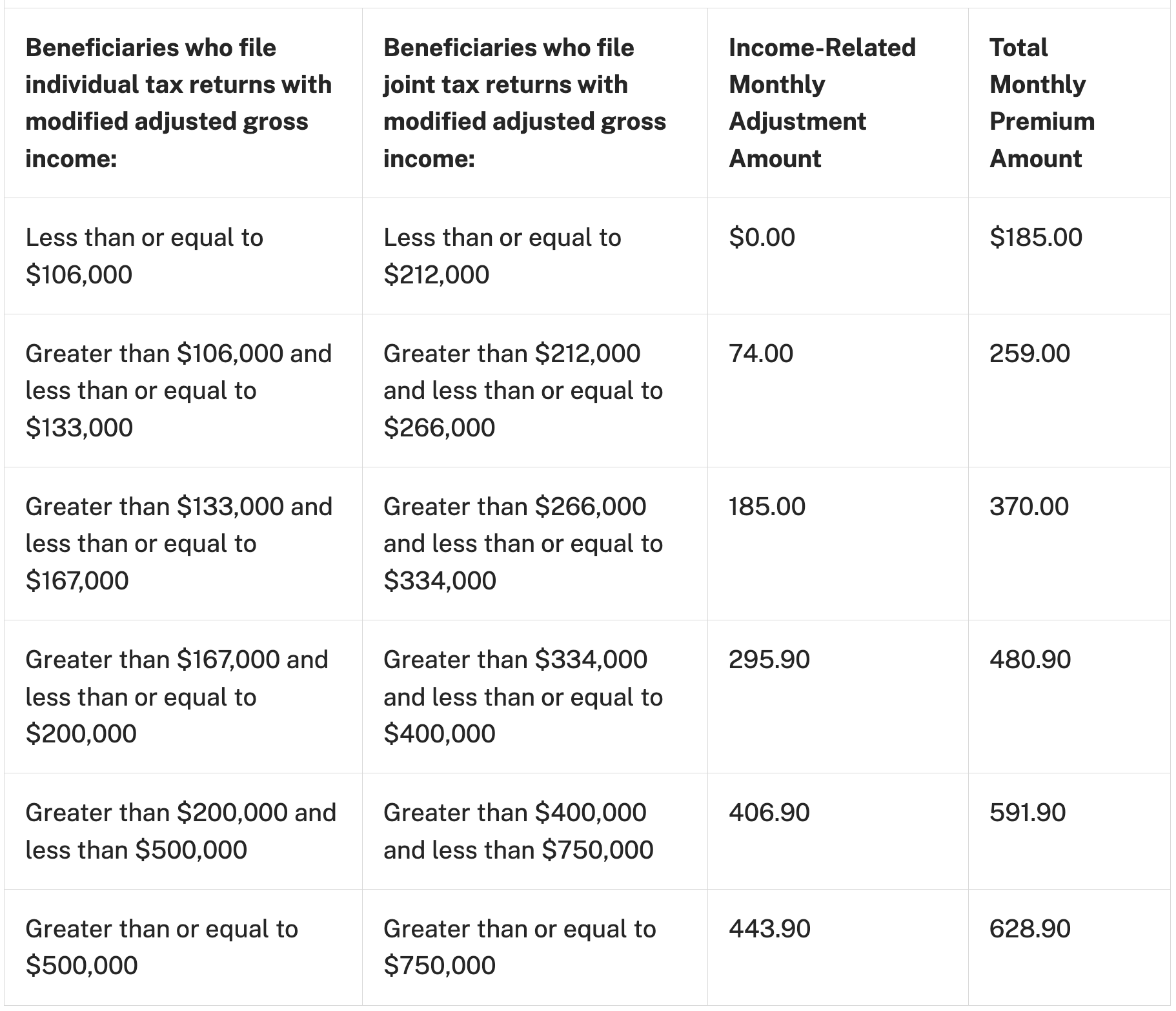

The table below, from the government's Centers for Medicare & Medicaid Services website, shows the latest income brackets and the corresponding IRMAA surcharges. But again, these are 2025 surcharges, based on 2023 income (i.e., tax returns filed in 2024).

The first column lists the brackets for single taxpayers. The second column has the brackets for married couples filing jointly (the surcharges shown in the third column are per person).

Here's a hypothetical example. Let's assume Fred and Wilma Taxpayer's regular retirement income (married filing jointly) is about $150,000. However, in 2023, due to a $100,000 Roth conversion and $20,000 of one-time extra income, their MAGI spiked to $270,000.

That means IRMAA would kick in this year. Fred and Wilma (now both on Medicare) must each pay Medicare Part B premiums of $370 a month ($8,880/year total for both) instead of the standard premiums of $185/mo each ($4,440/year total for both). Their income spike in 2023 resulted in their 2025 Medicare premiums doubling.

Avoiding IRMAA

Older readers may remember a 1950s sitcom (and film series) called My Friend Irma. Well, the Medicare IRMAA is definitely not your friend and should be avoided if possible.

Of course, if you're consistently earning a high income, you can't steer clear of IRMAA. However, if a temporary situation, such as converting funds from a traditional retirement account to a Roth, significantly boosts your income, be sure to consider how that additional income might result in IRMAA surcharges later.

The helpful Harry Sit has preliminary estimates of the IRMAA brackets for 2026 (2024 income) and 2027 (2025 income).

Additionally, SMI Premium-level members with access to Envestnet's MoneyGuide software can use it to map out and evaluate the impact of IRMAA (go to Goals > Health Care and enter your income information).

In MoneyGuide, the projected Income-Related Monthly Adjustment Amount will appear in the Health Care Expenses schedule (shown at right) and will be included in the software's cash-flow projections.

Caught by IRMAA? You can appeal

Fortunately, Medicare recalculates income annually (although with a two-year lag). So a single-year income spike won't affect Medicare premiums over the long term.

Even better, the government offers a review process if you've already been hit by a surcharge. Taxpayers can argue they shouldn't be subject to IRMAA, or that the surcharge percentage should be reduced.

Kiplinger covered this recently:

If you were working full-time in 2023 and have since retired, you might qualify [for an IRMAA cancelation or reduction] based on the decline in your income. You could also get a break if...your spouse retired.

Other life-changing events that could make you eligible for a reduction in your premiums include: Marriage, divorce or death of a spouse [and]...loss of income-producing property....

If you're subject to the surcharge, you should have received a notice from Social Security known as an initial determination. To request a review, complete the Medicare Income-Related Monthly Adjustment Amount-Life-Changing Event (Form SSA-44) (PDF) and provide supporting documents.

Thanks to Carl in Chattanooga for suggesting this topic! Carl has just filed a "Life-Changing-Event" appeal with Medicare/Social Security based on his wife's recent retirement.