Many Americans assume Medicare pays all medical expenses for people 65 or older. That isn’t so and never has been. Congress created Medicare 60 years ago to cover routine medical costs and short-term hospital stays, and Medicare’s main program has remained essentially unchanged since then.

However, in the 1970s, as healthcare costs rose and treatments expanded, the gap between what Medicare paid toward medical bills and how much patients had to pay grew larger. Congress then authorized Medicare Supplemental Insurance (in 1980), which led to the creation of optional add-on plans — offered by private insurers — called “Medigap.” The state-regulated, federally standardized plans pick up where Medicare benefits leave off.

In 1997, Congress went further, creating another option for supplemental coverage. The result was what is now called Medicare Advantage. These private plans, subsidized by Medicare, combine the specific benefits of “Original Medicare” with a gamut of additional benefits designed by private insurers.

Having choices in health coverage is a good thing. But that doesn’t mean navigating the range of Medicare options is easy. Indeed, it can be challenging and confusing.

This or that?

When approaching age 65 — the age at which most people become eligible for Medicare — seniors must choose between Original Medicare (also known as Medicare Parts A and B) or a private Medicare Advantage plan (Part C), although delaying enrollment is possible under certain conditions.

Those who opt for Original Medicare face a second decision: whether to purchase optional Medicare Supplement Insurance (Medigap). A senior wanting a supplement plan must choose among at least eight Medigap offerings, each with a different benefit structure and cost. (A further choice: whether to purchase optional “Part D” prescription coverage.)

Of Medicare’s 67 million current enrollees, about 20% have Original Medicare without a supplement plan, while 30% have Original Medicare along with an add-on Medigap supplement. The remainder — slightly more than half of Medicare beneficiaries — have selected an Advantage plan.

To be clear, the only choice required at age 65 is between Original Medicare and Medicare Advantage. Selecting a Medigap plan to supplement Original Medicare is a separate decision that can be made later. However, seniors who select Original Medicare tend to choose a Medigap policy at about the same time.

Supplementing with Medigap

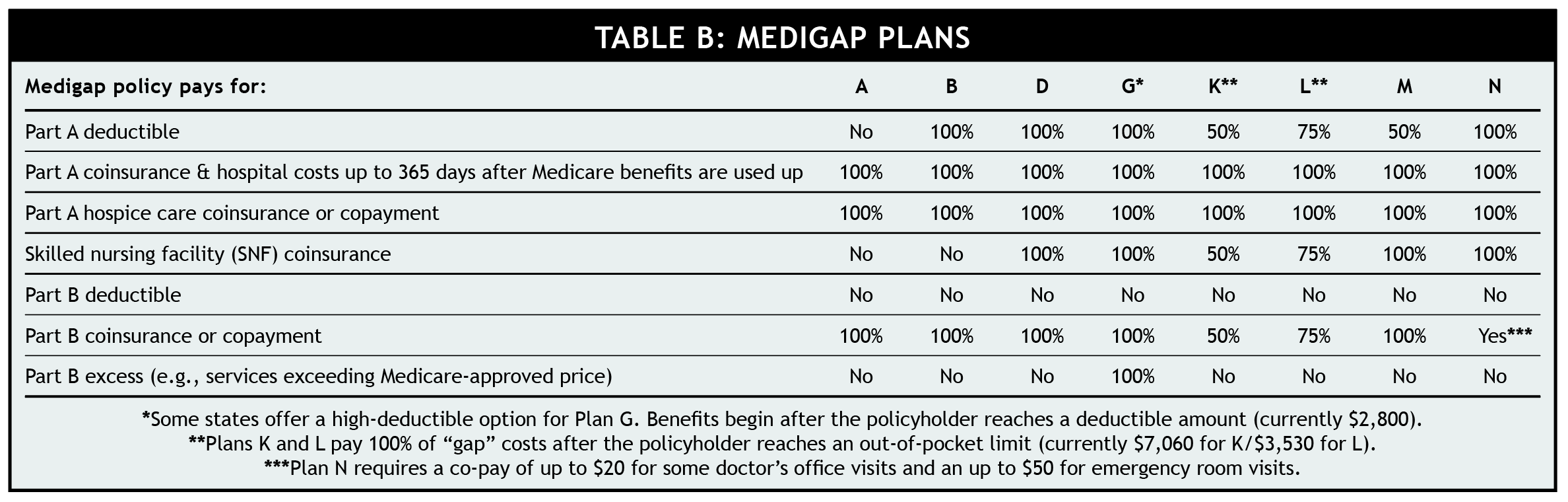

Medicare supplement policies cover costs — primarily deductibles, copays, and coinsurance — not paid for by either Part A (hospital insurance) or Part B (coverage for doctor visits and other medical services). Most Medigap plans cover all hospital charges and most of the non-hospital medical expenses that are excluded by Medicare. Certain coverage parameters vary depending on the type of supplement plan selected (see table below).

In most states, supplemental policies come in eight varieties, known as Plans A, B, D, G, K, L, M, N. (Don’t confuse Medigap “Plan A” or “Plan B” with Medicare’s Part A and Part B!) Medigap Plans C and F are available only to seniors who turned 65 before Jan. 1, 2020.

Every Medigap “A” plan — regardless of insurance company or state — has the same benefits, each “B” plan likewise is the same, and on down the line. However, Medigap premiums — even for the same plan type — can vary widely from company to company, so shop around.

(Be aware that Massachusetts, Minnesota, and Wisconsin have different Medigap plans. Also, a few states offer Medicare SELECT, a reduced-cost supplement plan.)

Because most supplement plans pay “first-dollar” coverage (i.e., they cover all of the “gap” between what Medicare pays and the total obligation), premiums aren’t cheap — typically $150 to $450 a month, depending on one’s location, age, and particular policy. That premium is in addition to the Part B premium all Medicare beneficiaries must pay, which is currently $174.70/month for most beneficiaries (higher-income beneficiaries pay more).

During the sixth-month Open Enrollment Period surrounding when a person first enrolls in Medicare Part B, Medigap policies are “guaranteed issue.” In other words, a person with a health condition who applies during that period can’t be refused or made to pay higher rates. However, once the sixth-month window has passed, an insurance company can deny a Medigap application or set a higher premium based on a pre-existing condition.

If you decide to purchase a Medigap policy, choose carefully. Although switching to another supplement plan is possible later, switching is cumbersome (except in a handful of states that allow switching once a year). In addition, any new policy likely won’t be “guaranteed issue,” meaning an insurance company could deny an application or require a higher premium for a person with a health condition.

Taking Advantage

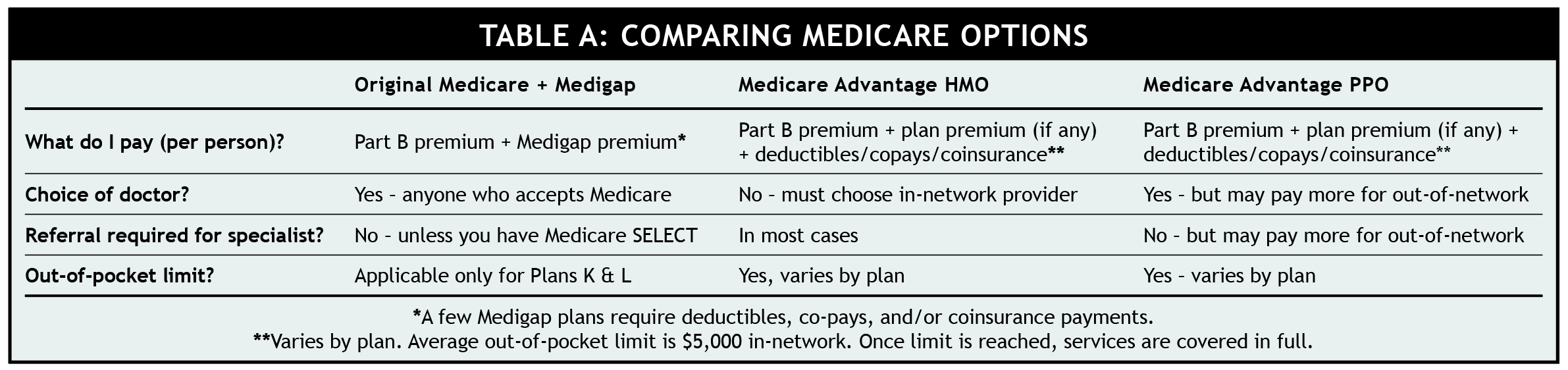

Companies that sell Medicare Advantage plans contract with Medicare and agree to cover everything Original Medicare covers. Instead of getting Plan A’s hospital coverage and Plan B’s medical insurance directly from Medicare, a senior with Advantage receives them from a private company.

However, Advantage plans go beyond the Medicare-designed A and B benefits. Many include coverage for Medicare deductibles and coinsurance costs (similar to what Medigap policies cover for enrollees in Original Medicare). Some plans include vision, hearing, dental coverage, and even health-club memberships. Many (but not all) incorporate a Medicare Part D prescription benefit too.

Compared to most Medigap plans, Medicare Advantage comes at a remarkably low monthly cost. According to the federal government’s Centers for Medicare & Medicaid Services, the average Advantage monthly premium in 2024 is less than $20. The average is so low because nearly three-fourths of seniors in Medicare Advantage pay no plan premium at all. In part, that’s because competition is keen. The typical Medicare beneficiary can choose from more than 40 Advantage plans.

(Even if an Advantage plan has no premium, Advantage enrollees, just like beneficiaries in Original Medicare, must still pay the government-mandated Part B premium.)

While Advantage plan premiums are attractive, policyholders do face restrictions not encountered by those who choose Original Medicare, such as being limited to a defined network of providers. Medicare Advantage plans can’t refuse an applicant based on a pre-existing condition, but some plans may limit access to certain specialists or treatments, so shop carefully.

Advantage beneficiaries also face potentially higher out-of-pocket expenses (i.e., expenses not reimbursed by insurance) than enrollees who select Original Medicare and Medigap. However, that liability isn’t open-ended. Federal law requires Advantage plans to limit annual out-of-pocket costs.

In 2024, the limit for in-network services is $8,300. However, according to the Kaiser Family Foundation, most plans set the limit much lower—at an average of about $5,000. The 2024 legal limit for combined in-network and out-of-network services is $12,450. Once the out-of-pocket limit is reached, the plan pays all covered expenses in full.

Some Medicare Advantage plans use an HMO (health maintenance organization) approach, while others use a PPO (preferred provider organization) structure (see Table A below). In addition, Special Needs Plans (SNP) exist for people with particular health problems.

click to zoom

Making the Original vs. Advantage decision

There is no simple answer for deciding whether to select Original Medicare or Medicare Advantage nor is there an easy template for choosing a Medigap plan. Your choices will depend on your current (and anticipated) health needs, your budget for premiums and out-of-pocket expenses, and how comfortable (or uncomfortable) you are with exposure to the “gaps” in Medicare coverage.

From a premium standpoint, the cheapest approach to Original Medicare is to forgo any supplement policy. About 4-out-of-10 of people who enroll in Original Medicare choose this route. However, choosing Original Medicare without adding a Medigap policy carries significant financial risk. Without Medigap, a beneficiary with Original Medicare is responsible for paying the Part A deductible ($1,632 for each hospital stay) plus 20% coinsurance for Part B medical expenses. Medigap policies typically pay these costs in full (see Table B below).

Further, Medigap policies usually cover extended hospital stays (beyond the 60 days Medicare will pay). In some cases, supplement plans will pay for a limited number of days in a skilled nursing facility. (They do not pay for assisted living, Alzheimer’s care, custodial care, or adult daycare.)

For people unwilling or unable to pay a premium for a Medigap supplement, the best approach is to choose a low- or no-premium Medicare Advantage plan. This would reduce financial exposure at little or no additional monthly cost.

click to zoom

Where to get more information

Medicare’s website offers a plan finder tool that lists the Medigap and Medicare Advantage plans by zip code, including price ranges for premiums and estimates of potential out-of-pocket outlays. In addition, the Centers for Medicare and Medicaid Services has a free 52-page guide online titled “Choosing a Medigap Policy” (PDF).