It was a year of extremes in SMI portfolios. Certain components produced best-ever results, while others were closer to the worst-ever side of the spectrum. Combining them to take a whole-portfolio view produced returns that were strong in an absolute sense, as SMI’s blended portfolios notched a second consecutive year of double-digit gains, ending 2025 at all-time highs. But some significantly lagging components contributed to a feeling that results could have been better.

The stock market followed a rocky road in 2025, rising early in the year, falling sharply in March and especially April (tariff announcement!), then staging a strong rally through the rest of the year before fizzling in December. As we’ve noted each of the past three years, the headline index returns (S&P 500 Index, +17.9%) were heavily skewed by the strong results of the largest stocks. For example, the S&P 500 Equal-Weight Index (+11.4%) was up substantially less, showing that many stocks didn’t really participate in the gains.

Bond returns were strong in 2025 for the first time in five years, providing a substantial boost to traditional 60% stock, 40% bond portfolios. A generic 60/40 portfolio gained +13.8%.

While the market environment has been much more favorable to indexed portfolios than SMI’s active strategies in recent years, there were signs of a market rotation late in 2025 that has continued strongly into the first half of January. Investor preference for the largest tech and “AI” (artificial intelligence) stocks has been so extreme the past three years as to seem unsustainable. If the recent rotation away from these former winners into the broad range of sectors and companies that haven’t participated much until recently continues, it would represent a big shift in the relative performance landscape between the headline indexes and SMI’s active strategies. To use a sports analogy, it would be like shifting from your opponent’s home field to your own. This has indeed been the case in early January and is something we’ll be watching closely.

Just-the-Basics (JtB) & Stock Upgrading

There was a wide performance split between the JtB components in 2025. While the S&P 500 Index gained +17.8%, the small/mid-sized stock component (+11.4%) gained much less. On the other end of the spectrum, the International component soared +32.4%. JtB only has a 10% weight in the international holding, limiting its impact. But a larger foreign stock allocation via Stock Upgrading and DAA was an important theme in SMI’s 2025 portfolios. JtB’s foreign stock holding helped the strategy (+18.2%) slightly outperform the U.S. stock indexes.

Stock Upgrading had a disappointing year, gaining just +4.2%. As we discussed in detail last year, FCTE was the primary cause of the lagging performance. Its focus on Quality stocks, with an equal-weight tilt to the strategy, was caught in the crossfire of the Quality factor’s worst relative bear market ever, along with severe underperformance by equal-weight strategies of all types.

Having dug deep into the causes of last year’s poor performance and the likelihood of it persisting, we remain confident in FCTE’s role going forward. We have reduced its allocation within the portfolio, but expect it to outperform the large company indexes in the future as our testing shows it would have in the past. Signs of a turnaround began late in 2025 and have accelerated strongly in early 2026, as FCTE outperformed the S&P 500 by a whopping +6.0% to +1.5% margin through the first half of January.

Stock Upgrading did have some bright spots in 2025. We’re very optimistic about the reintroduction of an updated “index switching” large company approach, which adeptly caught the trend shift from growth stocks to value late in the year. While our old growth index holding was down -0.6% through the first half of January, our new value index holding gained +4.2%.

Stock Upgrading also shifted us into international funds last year with good results. There were other standouts as well, such as Aegis Value, which more than doubled the S&P 500’s return in gaining +49.6% from the end of March through year-end (and which is up another +6.1% through the first half of January).

Bond Upgrading (BU)

SMI’s BU strategy was very conservatively invested in 2025, which led to it underperforming the Bloomberg U.S. Aggregate Index +5.8% to +7.3%. Bond Upgrading was revamped for 2026 to better position it for what we believe is a secular bear market in bonds that started in 2021. Early returns are positive: through the new lineup’s first month since being rolled out on Dec. 19, 2025, the new BU lineup has beaten the index +0.8% to +0.4%.

Dynamic Asset Allocation (DAA)

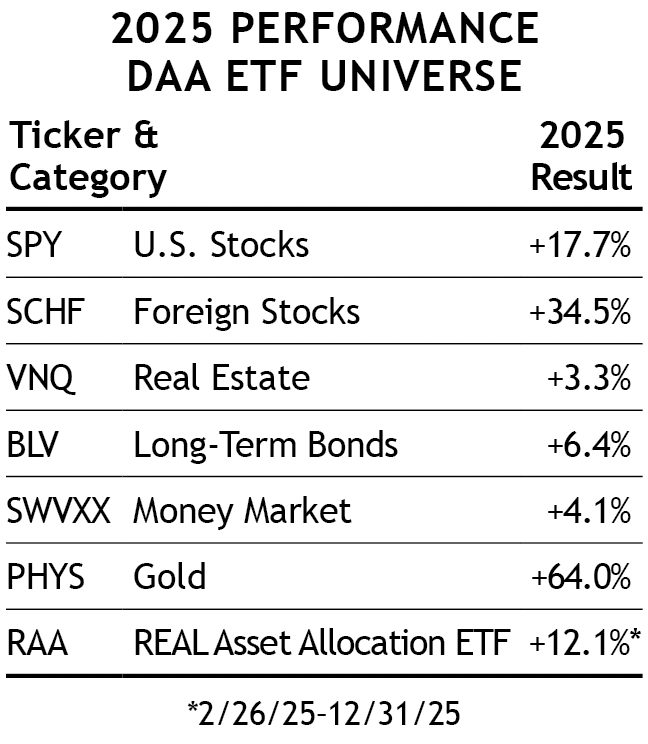

DAA outdid its strong 2024 gain of +17.3% with a huge gain of +26.7% in 2025. Given that DAA is the largest component of SMI’s blended portfolios, this had a powerful impact on the total returns earned by SMI members last year.

Gold is the biggest reason for DAA’s strength over the past two years, with PHYS more than doubling since DAA added it at the end of February 2024. Gold was up +64% in 2025, its largest calendar year gain since 1979. And it has kept on rolling through the first half of January, adding another +6.5%.

Gold wasn’t the only trick up DAA’s sleeve last year, however. Foreign Stocks also contributed big gains after being added last February. DAA’s foreign component more than doubled the S&P 500 Index’s gain (+30.6% to +14.7%) from that point through year-end. DAA also provided a good signal to diversify our foreign stock holdings into emerging markets at the end of September, with the emerging market holding outperforming DAA’s normal foreign holding +9.7% to +6.2% over the final three months of the year (vs. SPY +2.7%).

The REAL Asset Allocation ETF (RAA) launched in late February and was incorporated into DAA almost immediately. Its first-year performance has been solid, beating its 60% stock, 40% bond benchmark +15.0% to +12.8% from its inception through Jan. 15, 2026.

This was despite the environment since its debut being very strong for traditional 60/40 portfolios (both stock and bond indexes have performed very well). When broad stock and/or bond indexes are not performing well is when we really expect RAA to shine, given its ability to pivot into alternative asset classes (like commodities, gold, energy stocks, or strategies such as managed futures that can actually short — or bet against — stocks or bonds). RAA outperforming this past year, when both stocks and bonds were strong, was like winning on our opponent’s home field...and bodes particularly well for when conditions change and RAA gets to play to its own relative strengths!

As strong as these individual asset classes were in 2025, the real magic for DAA last year was being on the right side of the market’s major trends. The table above shows the importance of owning the winners and avoiding the weaker performers. Last year also vividly illustrated how powerful it can be to own the right classes at the right times, as opposed to simply owning all the classes all the time.

Sector Rotation (SR)

SR lost -18.9% in 2025, a painful result particularly in light of the fact that the strategy was actually a strong performer for much of the year. It ran into miserable luck in April, when its pivot into positively trending energy stocks was blindsided by the 1-2 punch of President Trump’s tariffs and OPEC+’s announcement of rapidly increasing oil production. By April 8, SR was down -40% for the year. From the end of April through year-end, SR outperformed the S&P 500 Index, cutting that year-to-date loss by more than half.

As with FCTE, an extensive review of all our past SR research (including a few tweaks in recent years) has us confident the strategy is on track to deliver in the future. Early January gains of +5.7% vs. +1.2% for the S&P 500 Index are encouraging.

50/40/10 (with 60/40 stock-bond Upgrading)

This portfolio refers to the specific blend of SMI strategies — 50% DAA, 40% Upgrading, 10% Sector Rotation — that SMI has often discussed as a general starting point for member strategy allocations. Last year, we started reporting this portfolio (using a 60/40 split between Stock and Bond Upgrading within the 40% Upgrading allocation). This is a reasonable reflection of how most SMI investors utilize such a “whole portfolio” blend and is an example of the type of diversified portfolio we encourage SMI readers to consider.

(Note: Blending strategies add complexity. Some members may prefer the automated approach offered by SMI Private Client.)

This version of a 50/40/10 portfolio gained +13.4% in 2025, following a +13.9% gain in 2024. The path to those returns varied, but the overall absolute return was similar, speaking to the power of a diversified approach to portfolio building.

In any given year, various assets’ gains will ebb and flow — for example, international stocks lagged badly in 2024 before soaring in 2025. But a commitment to sound process and broad diversification has a way of evening out a lot of the turbulence along the way, even when certain components of the portfolio run into historically bad problems (as FCTE and SR did last year).

Carefully considered, deliberately implemented

We’ve invested a great deal of time and effort over the past two years refining the SMI strategies to make sure they’re fit for today’s shifting market environment. Last month, we discussed the significant economic and market changes since COVID in explaining why we believe bond investing is going to be more challenging in the years ahead than it has been in recent decades. Those big-picture changes — which include the reversal of globalization, negative demographic trends in most developed economies, persistently higher inflation and rising interest rates, populist politics, and the emergence of a multi-polar world order amid considerable geopolitical conflict — are likely to impact every facet of investing.

As a result, SMI portfolios have evolved quite a bit compared to what we recommended a decade or two ago. Those changes have been carefully considered and deliberately implemented. It’s recognition that the world has changed, and we need a broader array of tools to handle the broader range of potential outcomes. Most investors are still using the playbook of the pre-COVID stock and bond secular bull markets. We think that may be a costly mistake.

Not all of those changes to SMI’s model portfolios have paid off in better relative performance — yet. But we believe “home field advantage” is in the process of shifting in our favor. As it does, so will our performance relative to the broad markets. That change may have begun last year, and SMI’s strategies have been firing on all cylinders so far in 2026.