Children learn the best lessons about money by using real money (their money) in the real world. That’s certainly true with investing.

It’s one thing to talk about compounding, the cyclical nature of the stock market, and the importance of taking the long view. But it’s something very different for kids to experience these lessons. This year’s market volatility offers especially good teaching opportunities.

Compounding is a force to be reckoned with

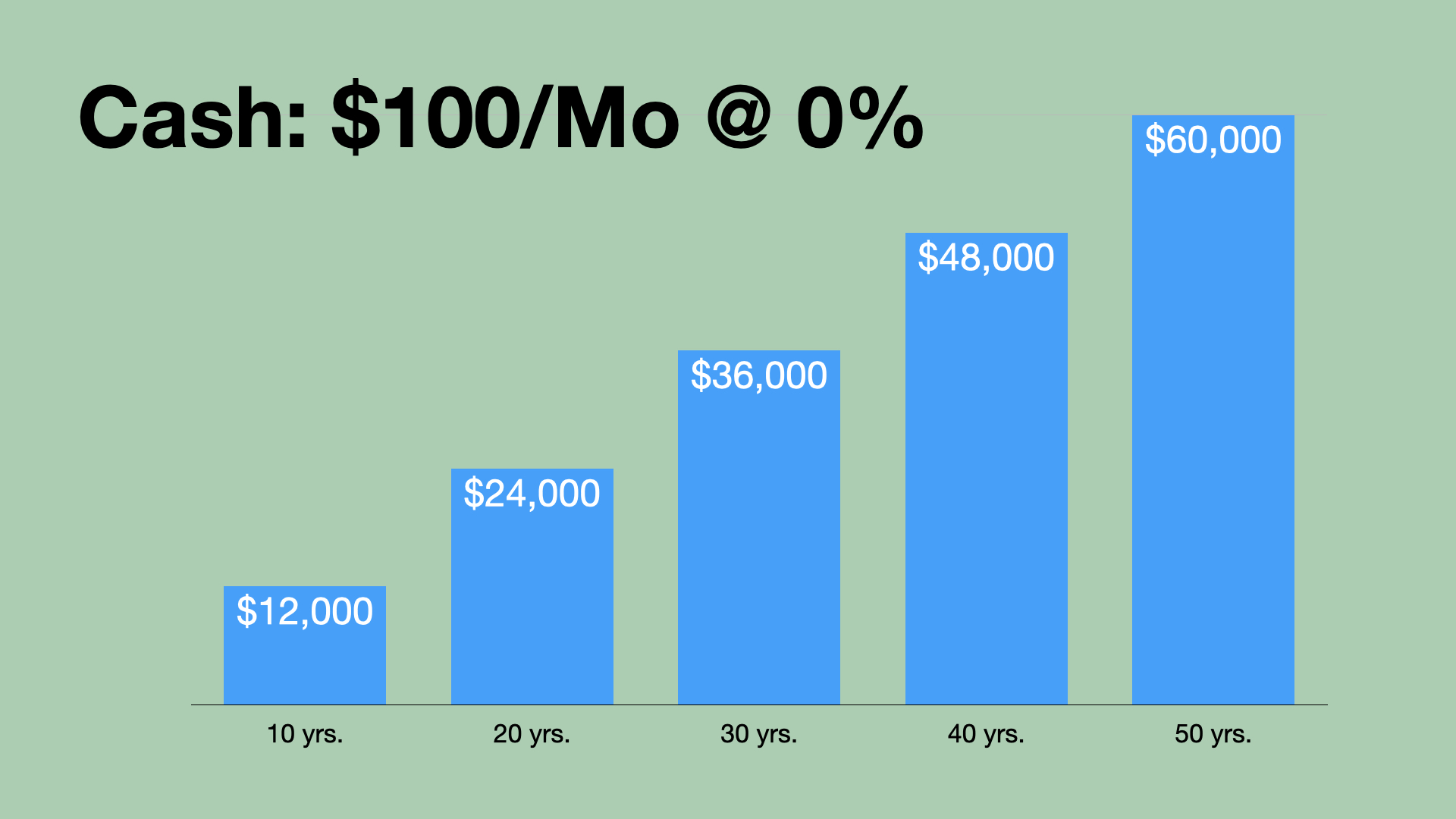

During a recent talk to a high school economics class, I showed what could happen if someone sets aside $100 per month for 50 years. First I showed them what would happen if they stuffed the money under their pillow each month. In 50 years, they’d have $60,000 (and a very lumpy pillow).

Their money would grow in a linear fashion. After one year, they’d have $1,200. After two, they’d have $2,400, and on and on.

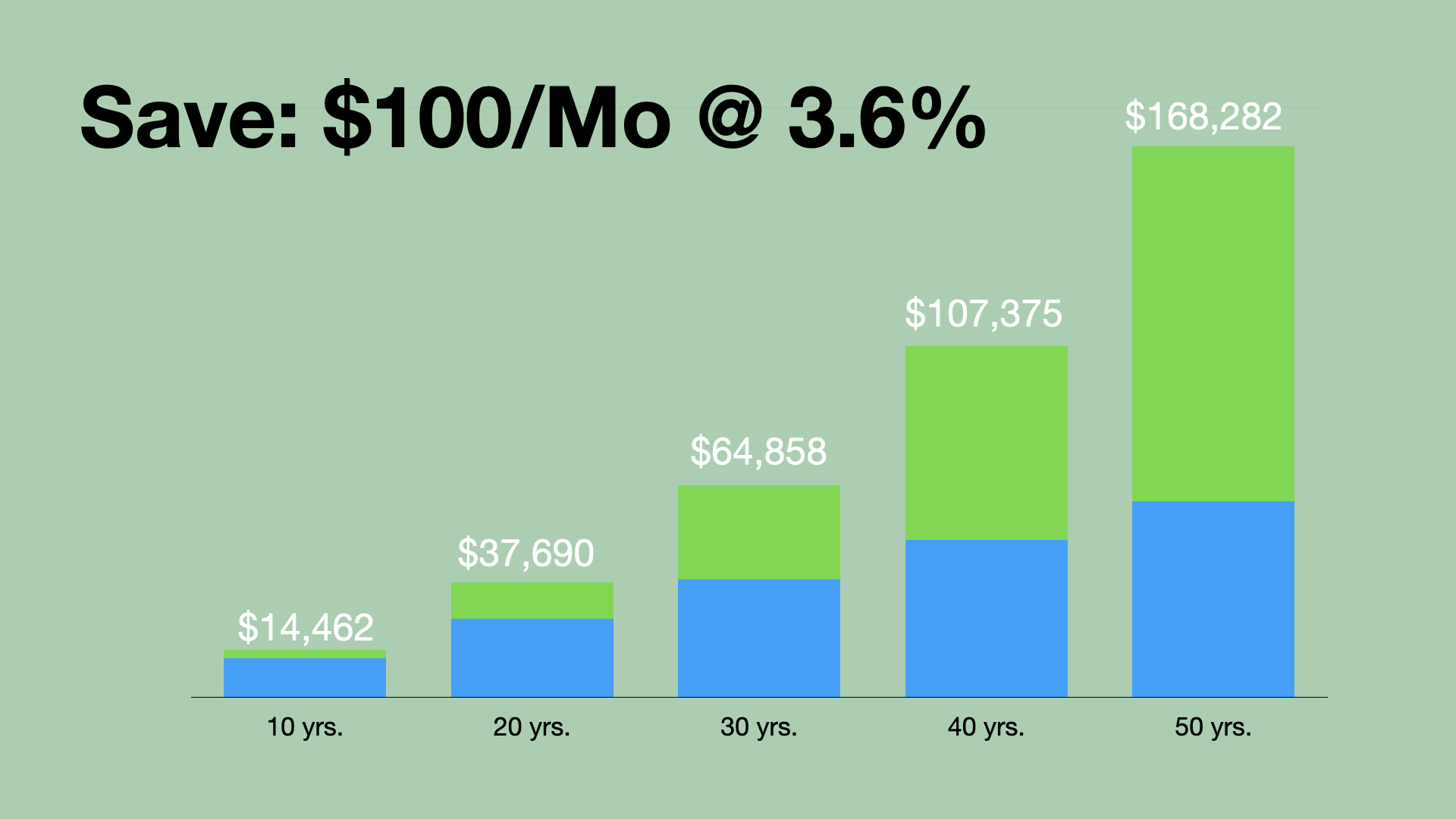

If they put the money in a bank savings account paying 3.6%, the money would not grow in a linear fashion, but exponentially. After 50 years, their $60,000 would turn into nearly $170,000.

I told them there are important reasons to have money in savings. However, while nearly tripling your money in 50 years is nice, a savings account isn’t the best vehicle for long-term growth.

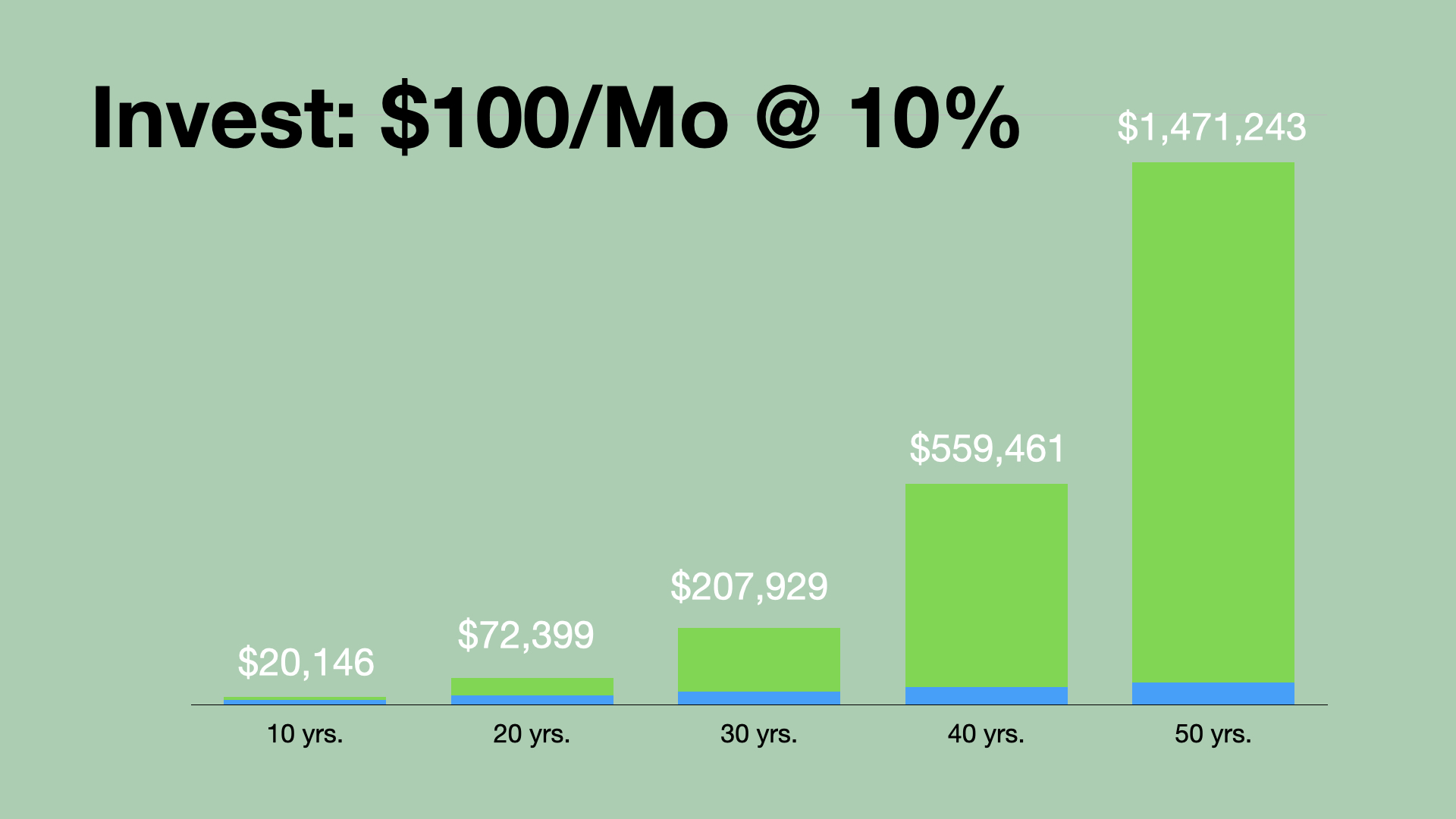

Next, I showed what would happen if their $100 per month were invested in a way that generated an average annual return of 10%, which is the market’s long-term growth rate. Their $60,000 would turn into nearly $1.5 million. Wow. That’s pretty amazing!

But here’s where today’s market offers especially valuable teaching opportunities

Compounding doesn’t happen on a straight line

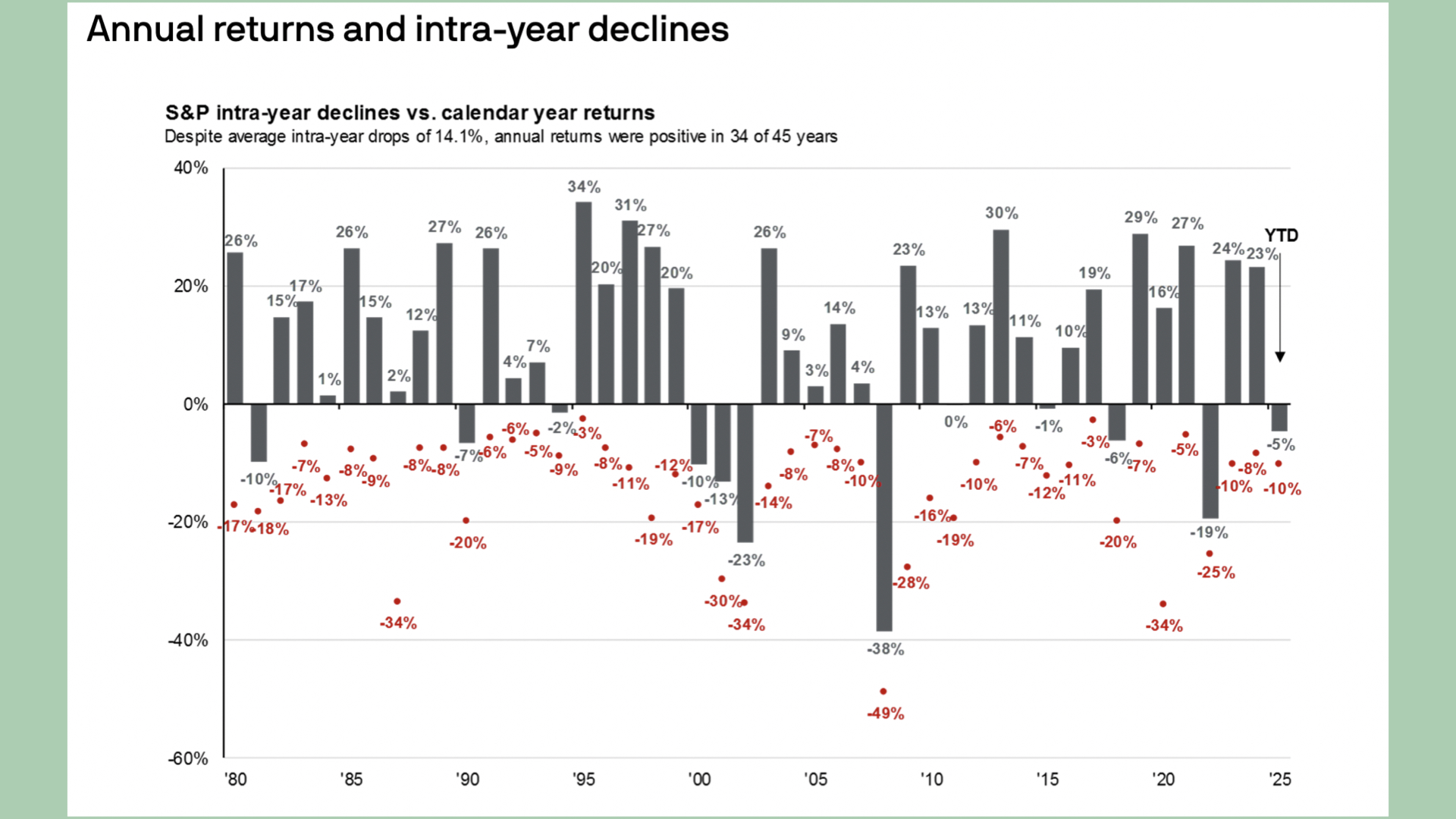

A +10% average annual return can generate incredible long-term growth, but I stressed to the students that it’s rare for any given year to generate that return. Instead, the market might be up +27% one year only to fall -19% the next (in fact, that’s what happened in 2021 and 2022).

I presented this graphic, which shows each year’s return as well as its intra-year low.

Click to enlarge.

A lesson taught by that graphic? Just because the market is down right now doesn’t mean it’s going to end the year down. Look at what happened in 2020. The market was down -34% at one point only to end the year up +16%. Then again, the market very well could end up lower this year. There’s no predicting the market.

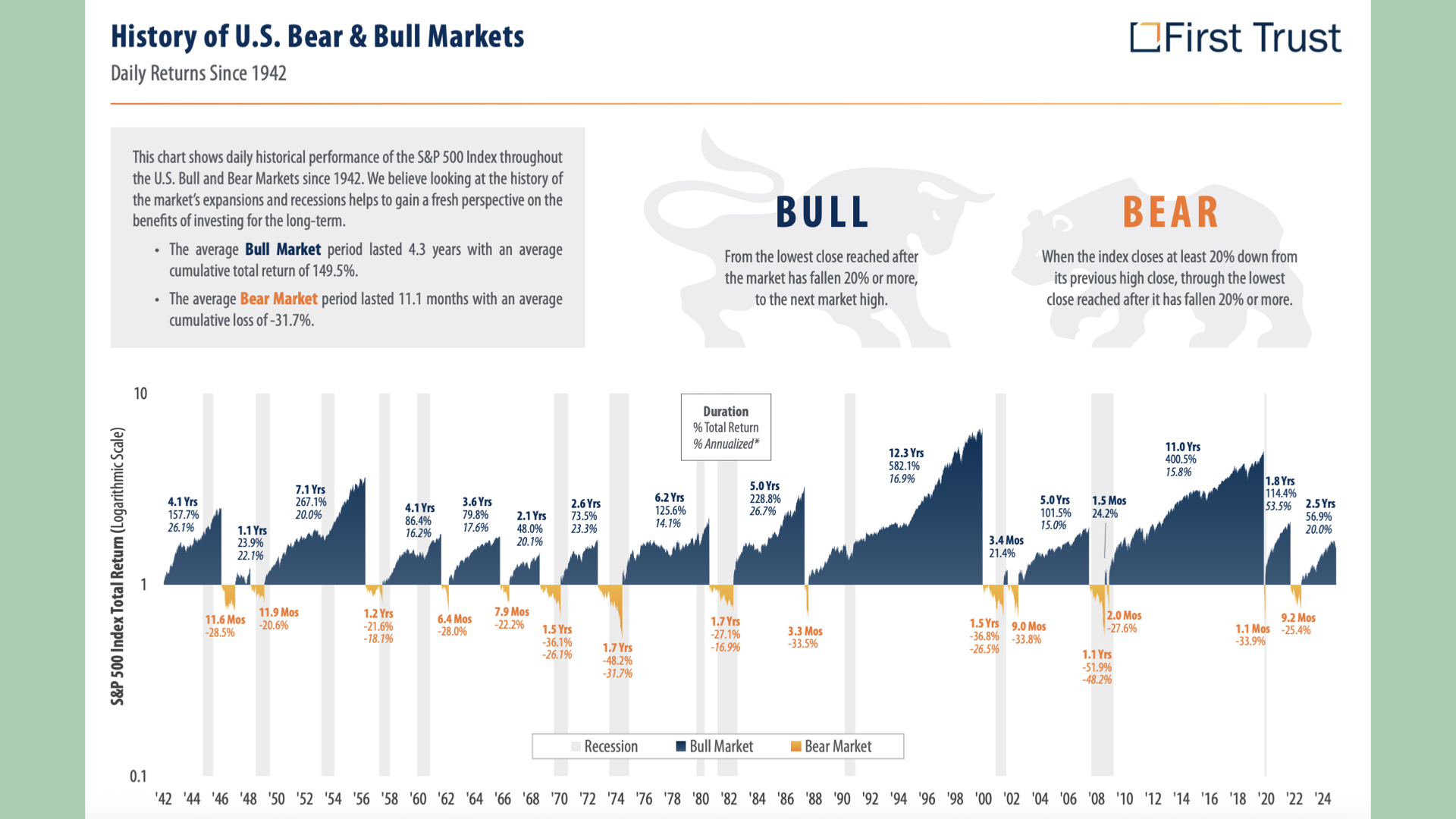

Next, I showed them this graphic — all of the bull and bear markets since 1942.

Click to enlarge.

It teaches two important lessons. First, the market cycles between bull markets and bear markets. And, historically, bull markets have lasted longer than bear markets and they’ve added more value than bear markets have taken away.

It shows the importance of taking a “steady plodding” (Proverbs 21:5, TLB) approach to building wealth.

The biggest risk

I told the students that to invest is to put money at risk. There’s “market” risk. What you invest in might go up, but it also might go down. There’s “inflation” risk. The cost of living could grow faster than your investments. Older people face “longevity” risk. They might outlive their money.

But the single biggest risk is you. You might get greedy and take on more risk than you should. Or you might succumb to fear and pull money out of the market when the market falls.

That is one of the most important reasons why it’s so helpful to get kids started with investing at a young age. Seeing a $50 investment lose half its value is one thing. Seeing $50,000 lose half its value feels very different. It’s important for kids to experience market downturns when they’re young and don’t have that much at stake. It takes time to build the intestinal fortitude necessary to live through market downturns without sabotaging one’s own portfolio.

To teach your kids more about money, pick up a copy of Trusted: Preparing Your Kids for a Lifetime of God-Honoring Money Management.

What are you doing to teach your kids (or grandkids) about investing?