Today’s typical teenagers probably don’t feel very wealthy. They might be working a part-time job at a restaurant or grocery store, but still, the money they earn probably doesn’t feel like very much.

In another sense, though, they have an asset that’s incredibly valuable. In fact, countless older people who have a lot of money wish they had more of the asset that today’s teens have. Of course, I’m talking about time.

All of us who have a young person in our life — whether a child, grandchild, niece, or nephew — would be wise to help them understand just how valuable this asset is.

I’ve been thinking about this lately because I’m in the midst of teaching a workshop for parents based on my book, Trusted: Preparing Your Kids for a Lifetime of God-Honoring Money Management. We just covered the section on investing.

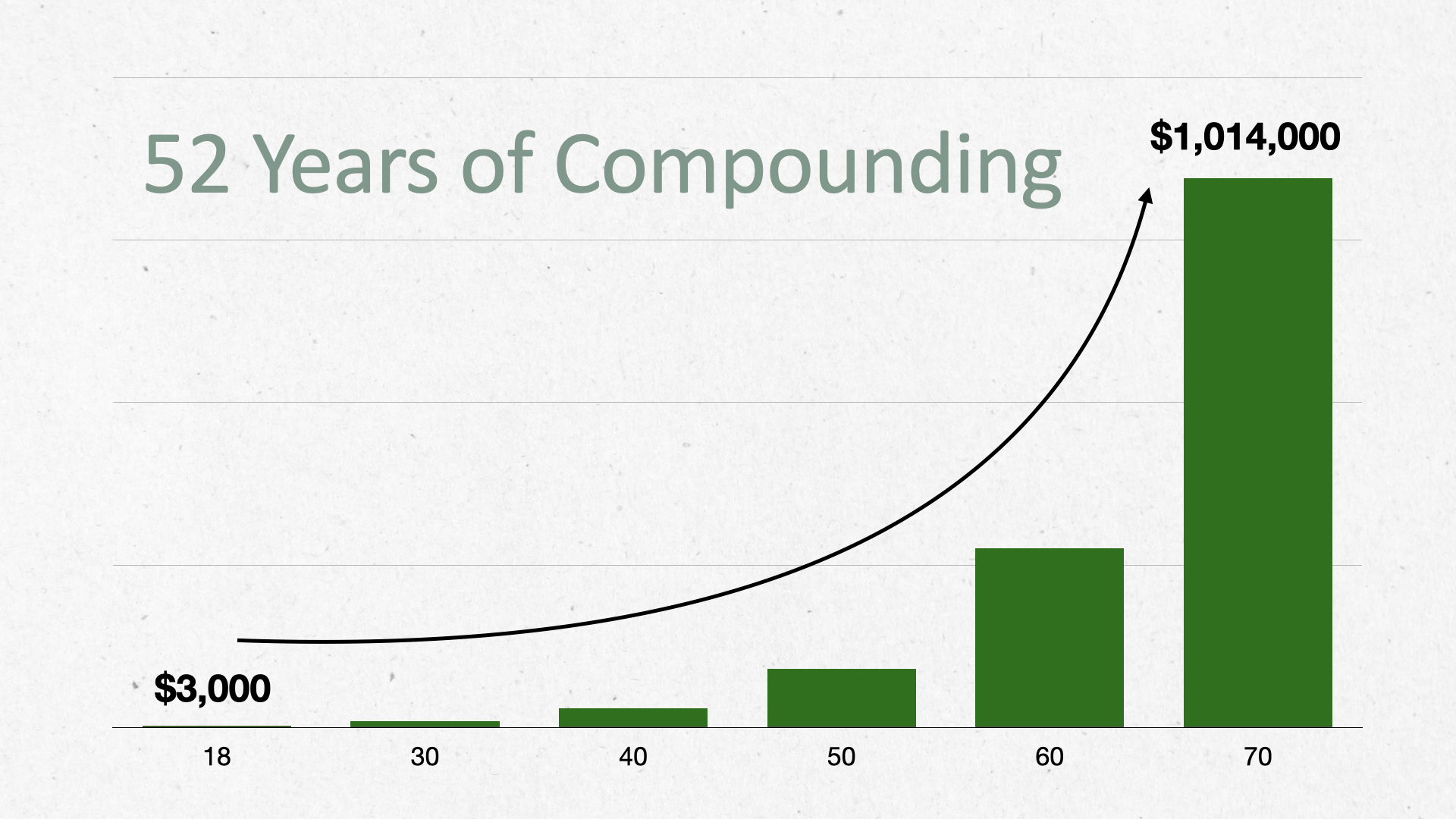

Here’s one of the examples I use in the workshop. Let’s say a young person saves $3,000 by the time she’s 18 and then invests the money in something as simple as an S&P 500 index fund. Even if she never adds another penny to the account, that $3,000 could realistically turn into over $1 million dollars by the time she’s 70, assuming she earns the stock market’s long-term average annual return.

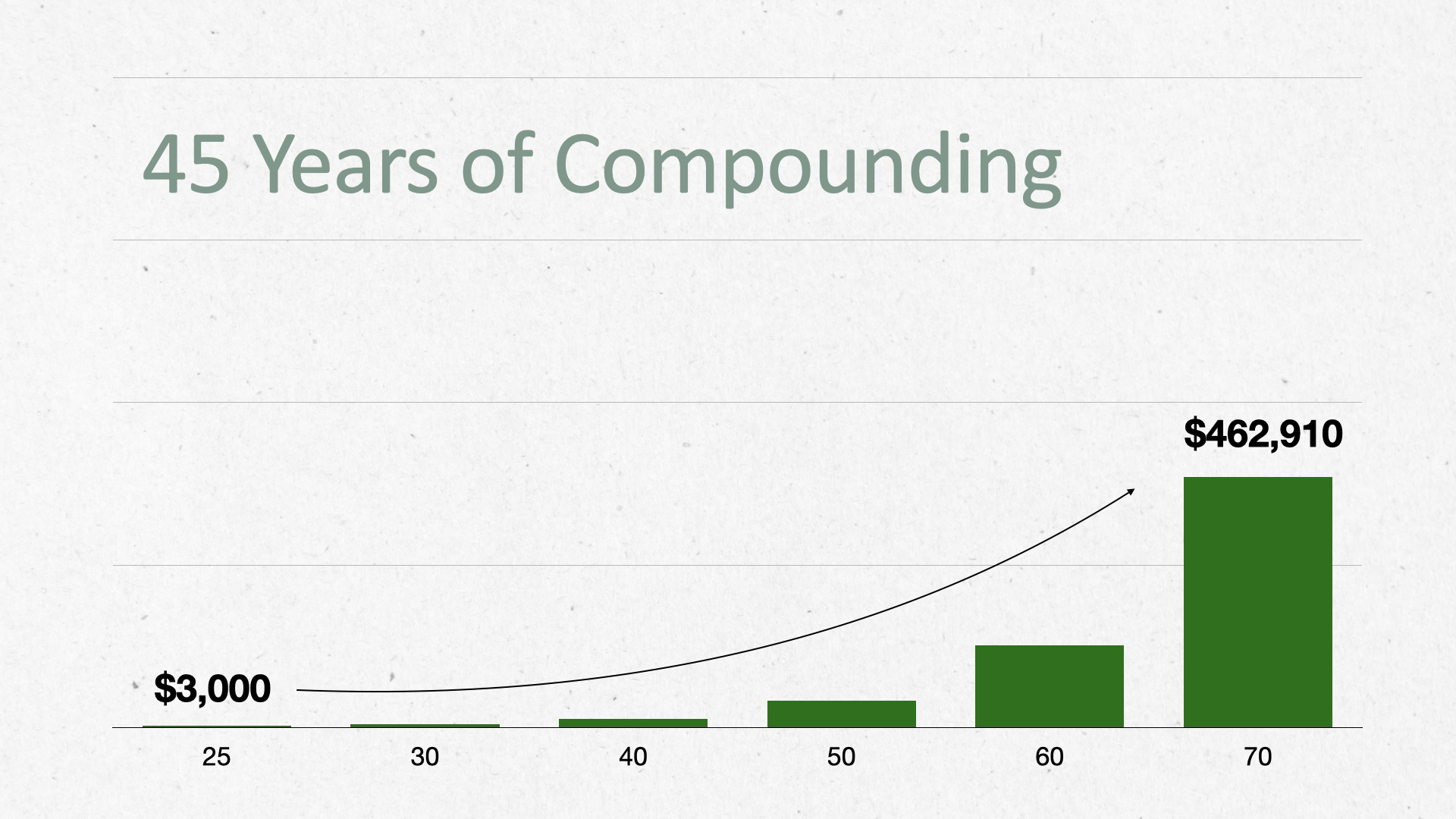

But what if she has other plans for her money at age 18 — things she wants to buy, trips she wants to take? What if she waits until she’s 25 to begin investing?

Wow. Waiting just seven years could mean missing out on over $500,000!

Of course, those sorts of returns are far from guaranteed. However, the longer a person stays invested, the more the odds move in their favor.

An incredible time to be an investor

Today, a young person could invest in an S&P 500 index fund for $1 and with no commission. That’s incredible. It has never been easier or less expensive to invest in the stock market.

Of course, it’s one thing to read about all of this. It’s something very different to actually get some money invested. Only then will a young person experience the market’s volatility, and that is a very good thing for them to experience while they are still living at home so that we can speak into that.

So that we can help them understand that the market moves in cycles. That there will be pull-backs and corrections and bear markets. That downturns are a normal part of investing. That feeling bad when the market goes down is normal. That they only lose money if and when they sell after the market has declined.

All are invaluable lessons that are best learned by having real money, their money, in the market, and with us walking through it with them.

I remember a day when our oldest was 14 and he wanted to see his investment account. So, we went online together and he had a look around. He noticed some terms he didn’t understand, like “cost basis,” and he wanted to learn.

If our kids had no money invested and I brought up the topic of cost basis over dinner, the conversation probably would have put them to sleep. But since our son had real money invested, his money, he was interested.

A three-pronged approach

In order to cultivate good habits in our kids that truly take hold — financial or otherwise — it’s important to take a “heart, head, and hands” approach. All three are needed.

Heart is all about identity, that we (and our kids) are stewards/managers of God’s resources, not consumers. That’s our overall orientation with money—managing it according to God’s principles and for His purposes.

Head is about knowledge. Knowledge of God’s Word and knowledge of how to apply it in practical ways. I want our kids to know that investing from a biblical perspective means taking a long-term, “steady plodding” approach (Proverbs 21:5, TLB) and diversifying our holdings (Ecclesiastes 11:2, NLT). What does that look like in the real world? Adding money to an investment portfolio on a regular basis, holding on through the market’s ups and downs, and not putting all your eggs in one basket.

Hands means using real money (their money) in the real world. Just as it’s far easier for our kids to spend mom and dad’s money than to spend their own, it’s a very different experience to have some of their own money invested in the market than to invest money that we give them.

Who are you paying attention to?

This topic is also on my mind because of a recent post I read that highlighted all of the bad investing advice being given on TikTok, which is a leading source of news for many of today’s young people.

The article highlighted one guy who said,

"Max out your 401(k) could be the dumbest advice that I’ve ever heard for anyone that wants to take financial control of their future. Why? ‘But Chris, it’s free money. You do max contribution and the company matches you. It’s awesome.’ I’m like, are you kidding me? First of all, I give you my money and I’m never going to see it for decades. Why would I give that to you even if you’re matching it. It’s not real. It’s fake, funny money."

The post also included a TikTok favorite from the height of the pandemic in which a couple explained their stock market investing strategy this way:

"I see a stock going up and I buy it, and I just watch it until it stops going up and then I sell it. And I do that over and over and it pays for our whole lifestyle."

I realize that a blog post with links to such TikTok posts can seem like an old guy rant against “those kids!” So, I showed it to our two teens who are still at home, and our 18-year-old said it was very misleading. He said there are a lot of people on TikTok giving really solid advice.

Out of all the content on social media these days, I’m glad he’s taking in some financial content and he finds some of it to be helpful. However, he acknowledged that he doesn’t follow any financial speakers in particular, just what pops up as recommended videos.

I told him that I skim over 100 finance sites and blogs each week, and out of them, there are less than 10 that I consider to be consistently really good. So I’m encouraging him to identify the producers he thinks are consistently good, and we’re having conversations about what that means.

The point is to get our kids, grandkids, or other young people in our lives interested in investing and help them put their most valuable asset to good use. The financial habits they build now, at a time of life when they don’t have access to a lot of money, are really important because those habits will be magnified (for better or for worse) as they get older and have access to more.