As expected, tax thresholds, deductions, and limits will rise in 2024, just as they did in 2023. Although the increases won't be quite as significant this time, they still may reduce your tax liability next year.

Here is the lay of the land, according to the IRS.

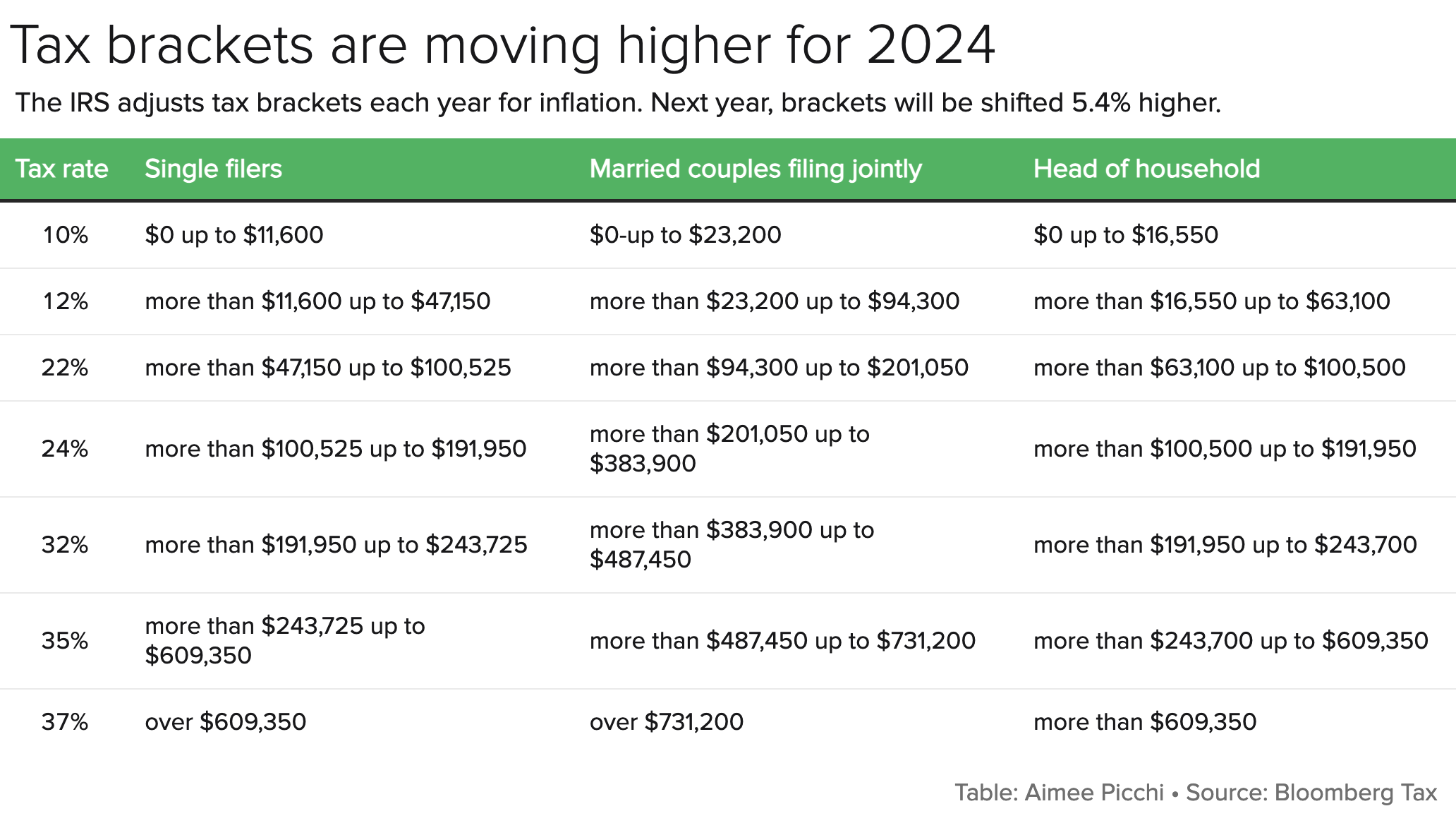

First, the income tax:

Note that the tax rates aren't changing. The rates for the seven federal brackets remain 10%, 12%, 22%, 24%, 32%, 35%, and 37%. However, because of inflation, the thresholds for each bracket have shifted, which means you'll be able to earn a bit more in '24 before being bumped into a higher bracket.

The same is true for income derived from capital gains. Here are the 2024 brackets/thresholds for the long-term capital gains tax. (Short-term gains — on assets held for one year or less — are taxed at the income-tax rates shown in the table above.)

Capital Gains Rate | For Singles with Taxable Income... | For Married Couples (Joint Returns) with Taxable Income... | For Heads of Households with Taxable Income... |

|---|---|---|---|

0% | Up to $47,025 | Up to $94,050 | Up to $63,000 |

15% | Between $47,026 and $518,900 | Between $94,051 and $583,750 | Between $63,000 and $551,350 |

20% | Over $518,900 | Over $583,750 | Over $551,350 |

Standard deductions

The standard deduction is rising for 2024, which means you can exclude more income from taxation even if you don't itemize. (The standard deduction is claimed by roughly 85% of taxpayers.)

Single taxpayers: $14,600 (up from $13,850 this year);

Married couples filing jointly: $29,200 (up from $27,700);

Heads of households: $21,900 (up from $20,800).

IRAs and 401(k)s

For those age 49 or younger, the contribution limit for traditional and Roth IRAs will increase to $7,000 in 2024 (up from $6,500 this year). However, the "catch-up contribution" limit for those age 50 or more will remain at $1,000.

Contributions to a traditional IRA are allowed at any income level, but that's not true for Roth IRAs. The income limit for taking full advantage of Roth contributions will be $230,000 in 2024 (married filing jointly), up from $218,000 this year.

Below are the 2024 contribution limits for workplace 401(k) accounts, showing the change from 2023. (These limits also apply to 403(b) plans, most 457 plans, and the federal-employee Thrift Savings Plan.)

Contribution Limit | 2023 | 2024 | Change |

Maximum employee elective deferral | $22,500 | $23,000 | + $500 |

Employee catch-up contribution | $7,500 | $7,500 | + $0 |

Defined contribution maximum limit, employee + employer | $66,000 | $69,000 | + $3,000 |

Defined contribution maximum limit | $73,500 | $76,500 | + $3,000 |

Health Savings Accounts

Allowable contributions to HSAs will rise by more than 7% in 2024. Individuals can contribute up to $4,150 to an HSA account (up from $3,850 in 2023), while families can contribute up to $8,300 (up from $7,750).

People 55 or older by Dec. 31, 2024, can contribute an additional $1,000. (Note that the age for extra contributions is 55 for Health Savings Accounts, not 50, as with other accounts.)

However, along with the increase in the contribution ceiling, HSA holders will face slightly greater exposure because deductibles are going up.

Under the law governing Health Savings Accounts, an HSA must be combined with a high-deductible health plan (HDHP). In 2024, the size of those high deductibles will increase. An HDHP must have a deductible of at least $1,600 for self-only coverage (up from $1,500 in 2023) or $3,200 for family coverage (up from $3,000).

2024 out-of-pocket expenses for an HDHP (not counting premiums) will top out at $8,050 for individual coverage (up from $7,500 this year) and $16,100 for family coverage (up from $15,000).