The June cover article of the SMI newsletter covered much ground about Envestnet MoneyGuide, the planning software available to SMI Premium-level members. However, one aspect of MoneyGuide mentioned only briefly is that it can help you plan your Social Security claiming strategy.

Although you can find free tools online for projecting Social Security benefits, MoneyGuide's advantage is that it helps you choose an SS claiming strategy in the context of your overall financial picture rather than looking at Social Security alone.

A brief walk-through

If you have MoneyGuide, here's how to locate the Social Security optimization: Go to Results > Recommended Scenario > Social Security.

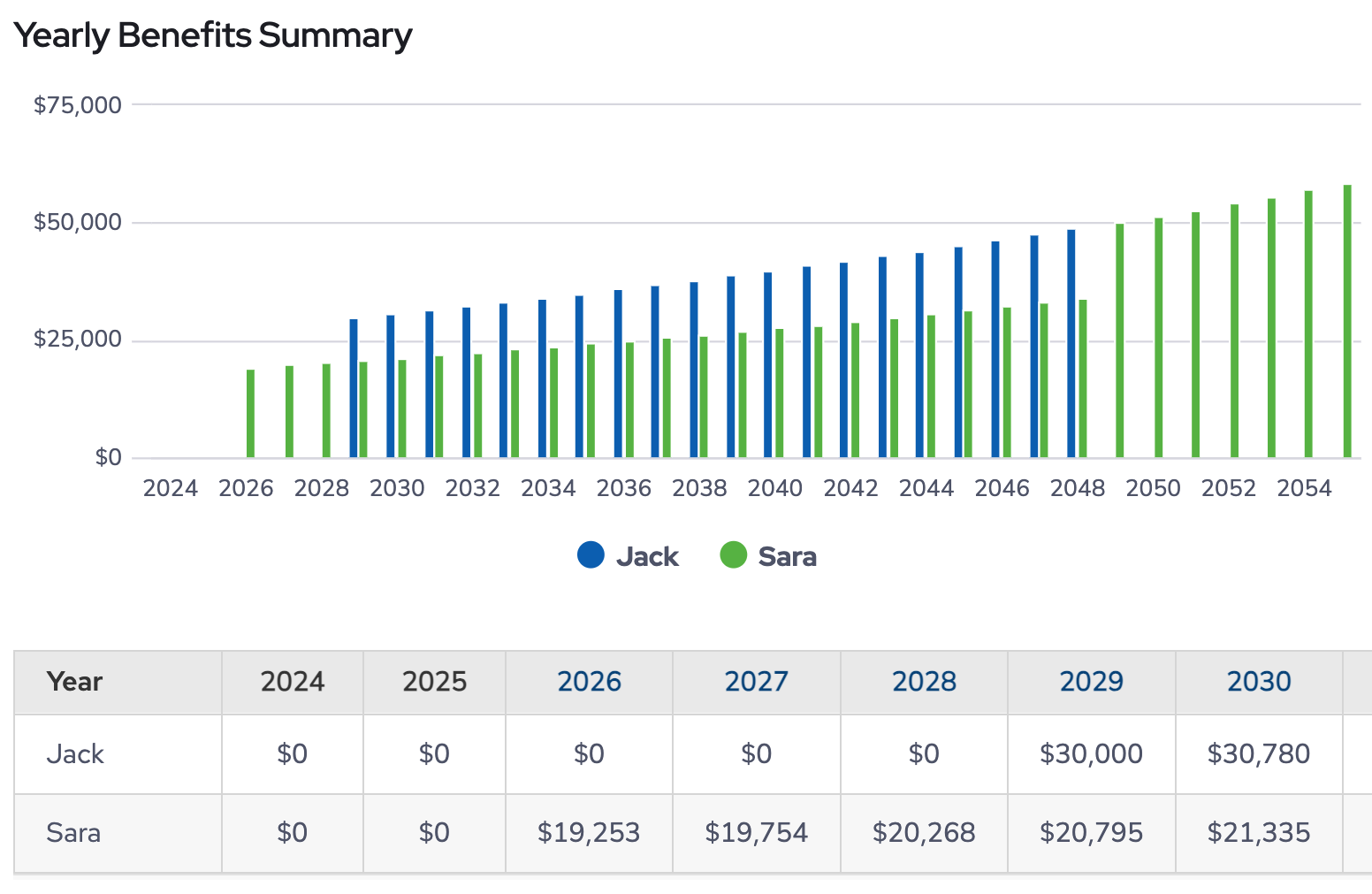

Below is a MoneyGuide screen capture showing claiming options for the hypothetical couple from our recent cover article, Jack and Sara Rogers. The options in the columns are based on Jack and Sara's ages, earnings records, and projected death dates. (These data are input during the MoneyGuide set-up process.)

Click to enlarge.

Sara is considering claiming her Social Security benefits this year (she's not quite 65 yet), while Jack plans to wait until age 70. This option is shown in Strategy 1 above.

("Probably of Success" relates to the likelihood that following this claiming strategy, combined with Jack and Sara's other financial choices/resources, will enable them to meet the financial goals outlined during the set-up process.)

From a purely dollars-and-cents standpoint, Strategy 5 above is the optimal choice, but that approach would require Sara to wait 5-plus years before claiming (at age 70).

However, Jack and Sara note that the "success" difference between options 5 and 6 is small and that using Strategy 6 would allow Sara to begin receiving benefits at age 66.

To them, that seems like a better option — not optimal financially, but better suited for some of their chosen goals. They want to travel, for example, and they'd prefer to do as much as they can in their 60s rather than wait until their 70s.

By clicking the "Detail" link at the bottom of the Strategy 6 column, Jack and Sara can see how their projected benefits would stack up year by year.

The colored vertical lines in the chart illustrate what happens at Jack's projected death date in 2049. In that year, Sara's benefit ends and she inherits Jack's benefit. (The Social Security Administration provides a more complicated explanation of how Sara's widow's benefit is calculated, but the practical result is that Sara will start getting a total monthly benefit equal to Jack's benefit.)

Having compared the claiming options shown in MoneyGuide, Jack and Sara decide on Strategy 6. However, that doesn't mean the other options are "wrong." They are simply different.

The "best" claiming option(s) depends on one's situation.

Knowledge is power

As SMI noted in a recent article, "By running the numbers for various [Social Security] claiming scenarios, you can compare the dollars-and-cents impact of different approaches. Weighing the options is particularly important for married couples because one spouse's benefits can affect the other's in several ways. Coordinating benefits is crucial to achieving an optimal result."

Using MoneyGuide, you can find the "best for you" approach to meeting your lifestyle and financial goals.