It’s the paramount question of every retiree and near-retiree: "Will my investment savings be enough to last through the years ahead?"

That question is easier to answer than ever before with help from Envestnet MoneyGuide, the award-winning planning tool available to SMI Premium-level members.

Will you have enough money to live on for the rest of your life? That uncomfortable question haunts anyone planning their retirement, especially those closest to leaving the paid workforce. For many, the answer is a not-too-reassuring “maybe” — even for people who saved and invested diligently during their working years. Or perhaps a more common answer would be, “I have no idea.”

Planning for the “de-accumulation” phase of life — when you’re no longer building wealth but spending it — is challenging. Your “time horizon” is unknown. Will you live to 80? To 90? To 100? Long life is a blessing (Psalm 91:16, Proverbs 9:10-11), but with it comes the possibility that you might outlive your savings, known in the financial world as “longevity risk.”

Improvements in healthcare, nutrition, and workplace safety are among the factors helping people live longer now than in previous generations. According to the Society of Actuaries, if both husband and wife reach age 65, there’s a 25% chance at least one will survive to age 98. For anyone retiring at 65 or even 70, it would be wise to have a de-accumulation strategy that can survive for roughly three decades.

In addition to “longevity risk,” retirees face the same “market risk” that all investors face, but with potential consequences that aren’t easily overcome. During the decades of building wealth in preparation for retirement, a market downturn can be an investor’s friend (though that may not seem apparent then!). Those who stick to their investing plans during declines, steadily buying shares at lower prices, are rewarded when the market rebounds.

However, for retirees who are no longer making new investments, a downturn could affect how much they have to live on for years to come — especially if such a decline occurs early in retirement (this is called “sequence of returns” risk). A portfolio you worked decades to build can shrink before your eyes.

There is also “inflation risk.” A rising cost of living can relentlessly erode the purchasing power of retirement savings, making your remaining funds worth less and less.

A strategy that works

How can you be confident that your financial resources will last in the face of these and other risks? The most common strategy, recommended by many financial planners, is to withdraw 4% of retirement holdings in the first year of retirement, then stick with the dollar amount of that withdrawal in subsequent years, increasing it only to match inflation.

Others think a 4% withdrawal rate is too low. Still others believe it is too high — they suggest an initial withdrawal of closer to 3%. Some dismiss the idea of a static percentage target altogether and suggest dividing one’s age by 20 and using that number as the year-by-year percentage-withdrawal guide.

Financial writer Jonathan Clements complains that many such strategies seem “overly engineered and overly dependent on the investment returns assumed.” He suggests that “what we need is a strategy that’ll work even if markets are miserable and even if we live an extraordinarily long life.”

He’s right. And if you have Envestnet MoneyGuide — the web-based financial-planning software available to SMI Premium-level members — you have the necessary tools to figure out a withdrawal strategy based on your specific “needs, wants, and wishes” rather than on a particular percentage. MoneyGuide enables you to forecast income and expenses over several decades and consider a range of spending possibilities and earnings assumptions. You can experiment with tradeoffs — sacrificing a little of this to get more of that — and gauge how those tradeoffs change your financial forecast.

Bear in mind that your financial goals and earnings projections must be realistic. Overly optimistic aspirations and wishful thinking about future returns will produce a plan that will not work in the real world. Instead, be levelheaded about the possibilities and acknowledge that successful financial planning typically involves tough choices.

A hypothetical couple

Jack and Sara Rogers have reached the threshold of retirement and are trying to devise a sustainable withdrawal strategy. We will examine how MoneyGuide can provide the information they need to manage the de-accumulation phase of life.

MoneyGuide can handle a broad range of financial situations. However, for purposes of illustration, we’ve created a simple situation for our hypothetical couple: They are debt-free and have half of their retirement holdings in traditional IRAs and half in Roth IRAs.

We’ll assume Jack and Sara are both aged 65. They’ve saved and invested diligently for several decades and are in good financial shape. Specifically, Jack and Sara have paid off their mortgage and have roughly $700,000 (combined) in their retirement accounts. Sara also has a $3,600 annual pension (non-inflation-adjusted) from a former job.

In addition, they have Social Security benefits coming. Although they could have started taking reduced retirement benefits at age 62, both decided to wait and take a higher monthly benefit later. Sara will claim benefits at age 66 and 10 months — her “full retirement age” defined by the Social Security Administration. Her projected first-year benefit is $19,000.

Even though Jack is retiring at 67, he plans to wait until age 70 to apply for Social Security so that his monthly benefit will be about 25% greater than if he claimed at his full retirement age. (Jack’s decision to apply at 70 will also ensure the highest possible ongoing benefit for Sara if he dies first.)

Financially speaking, most people would be happy to trade places with Jack and Sara. It appears they have enough money to get through their senior years while enjoying a comfortable lifestyle and being generous. But do they? Let’s use Envestnet MoneyGuide to find out.

SMI detailed how to set up MoneyGuide in a previous article, so we won’t repeat all that information here. We’ll just assume that our hypothetical couple, Jack and Sara, have already input all the necessary information about their retirement accounts, Sara’s pension, paid-off mortgage, and Social Security claiming strategies.

They also have input reliable estimates for their “needs,” which include their general living expenses (based on their budget) and their basic healthcare expenses (MoneyGuide projects Medicare and Medigap premiums and out-of-pocket costs). Finally, Jack and Sara also estimate the cost of various future “wants” (such as travel, additional giving, and a home remodeling project) and “wishes” (in their case, a desire to leave some money to children and grandchildren).

Now, they’re ready to use MoneyGuide to help them make wise choices about how much they can draw from their retirement portfolio each year without undermining the likelihood that their money will last for the next three decades.

The known unknowns

As is the case with anyone trying to plan for their later years, Jack and Sara’s drawdown calculation is complicated by significant unknowns:

They don’t know how long they’ll live. Do they need their money to last only a few years or decades?

They don’t know the rate of return they’ll earn. Will their average rate of return be 10%? 6%? More or less?

They don’t know the sequence of returns. If Jack and Sara’s nest egg suffers a significant market loss right before or shortly after they start taking withdrawals, their portfolio will be less likely to last the rest of their lives.

They can’t predict future inflation. Inflation undermines future purchasing power. That’s why it’s often called the “silent killer” of savings and investments. (Sometimes inflation moves quickly, but that has been relatively rare.)

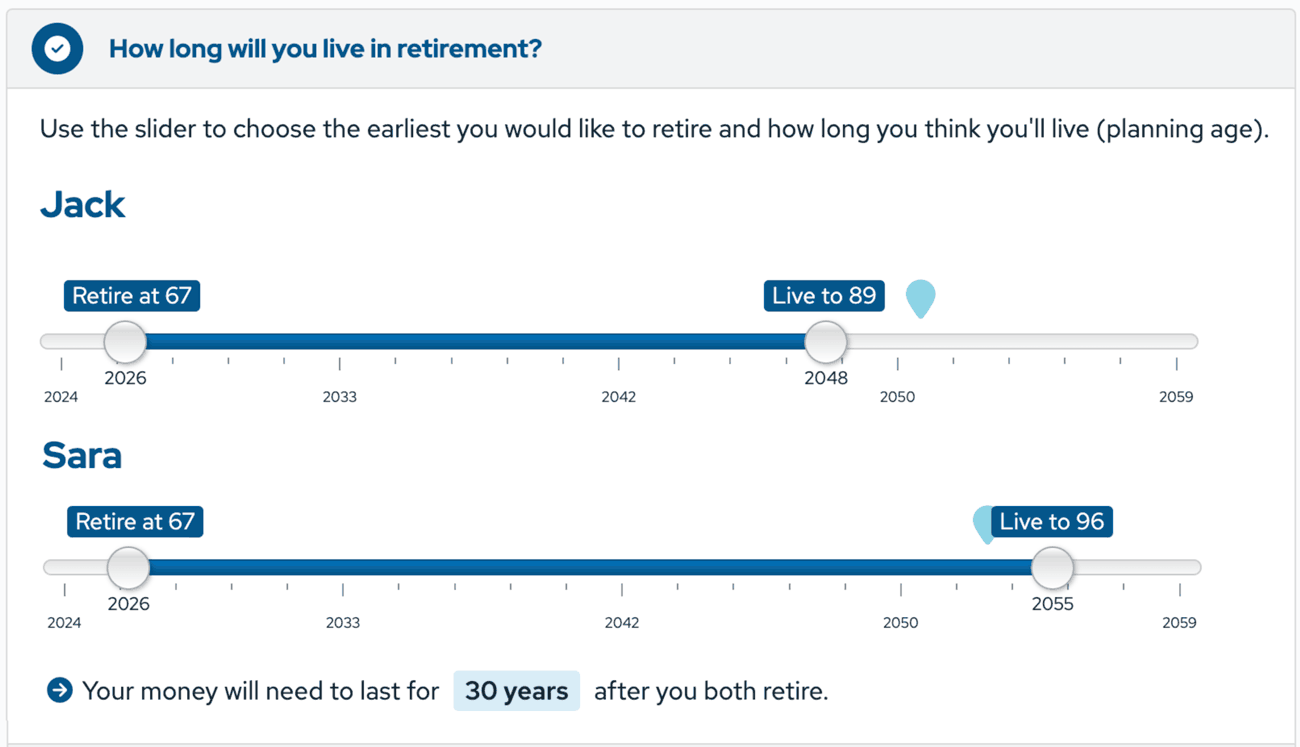

Among these uncertainties, the easiest to plan for is life expectancy: Jack and Sara must assume they will live to a ripe old age! They estimate Jack will pass away at age 89 and Sara will live to her mid-90s. That means they need their money to last for 30 more years, covering not only their needs but, if possible, their wants and wishes.

Getting ready to run the numbers

Because our hypothetical Mr. and Mrs. Rogers have already done their MoneyGuide set-up, they log in and click on the name of their account, “Jack and Sara’s Plan.” In the “About You” section, they go to the drop-down for “Goals,” and then “Retirement Period,” and choose “Live to 89” for Jack and “Live to 96” for Sara (see image below).

Jack and Sara have already input their projected retirement expenses (in the “Goals” section). MoneyGuide carries these projected expenses forward year-by-year, increasing them by a default 2.6% assumed annual inflation rate. (For now, Jack and Sara will use the default inflation rate. Later, they can alter the rate to gauge the impact of higher inflation.)

Based on their existing budget, Jack and Sara think their first-year spending will be about $40,000 in basic living expenses (food, clothing, transportation, insurance, general household costs, and taxes). They’ll also need an estimated $12,000 for health expenditures (covering Medigap policies, out-of-pocket costs, and Medicare Part B premiums).

In addition, Jack and Sara decide to earmark $18,000 in first-year spending for two of their “wants,” specifically, ramped-up giving and extended travel. (Although they also want to do a home remodeling project, they decide to wait until after Jack’s Social Security kicks in in 2029.)

In all, our hypothetical couple expects to spend roughly $70,000 in the first year of retirement—$52,000 in “needs” (basic living expenses plus healthcare) and $18,000 in “wants” (giving and travel). Sara’s Social Security and pension will cover less than a third ($22,600). That means Jack and Sara must withdraw roughly $47,400 from their retirement accounts to fund the initial year of retirement spending.

Can they afford to do that? Let’s find out.

Jack and Sara have listed their investment assets in MoneyGuide’s “Money” section (under “About You”). For simplicity, we’ll assume their roughly $700,000 portfolio is 50% invested in stocks (divided equally between stocks of large and small/mid-sized companies) and 50% in a bond-index fund.

1000 scenarios

Jack and Sara are now ready to determine if they are well-positioned for the next 30 years. They click “Results” near the top of the screen. From the drop-down menu, they choose “Current Scenario.” The heading at the top of the Current Scenario page reads: “You have a simple question: ‘Can I fund all my goals without running out of money?’”

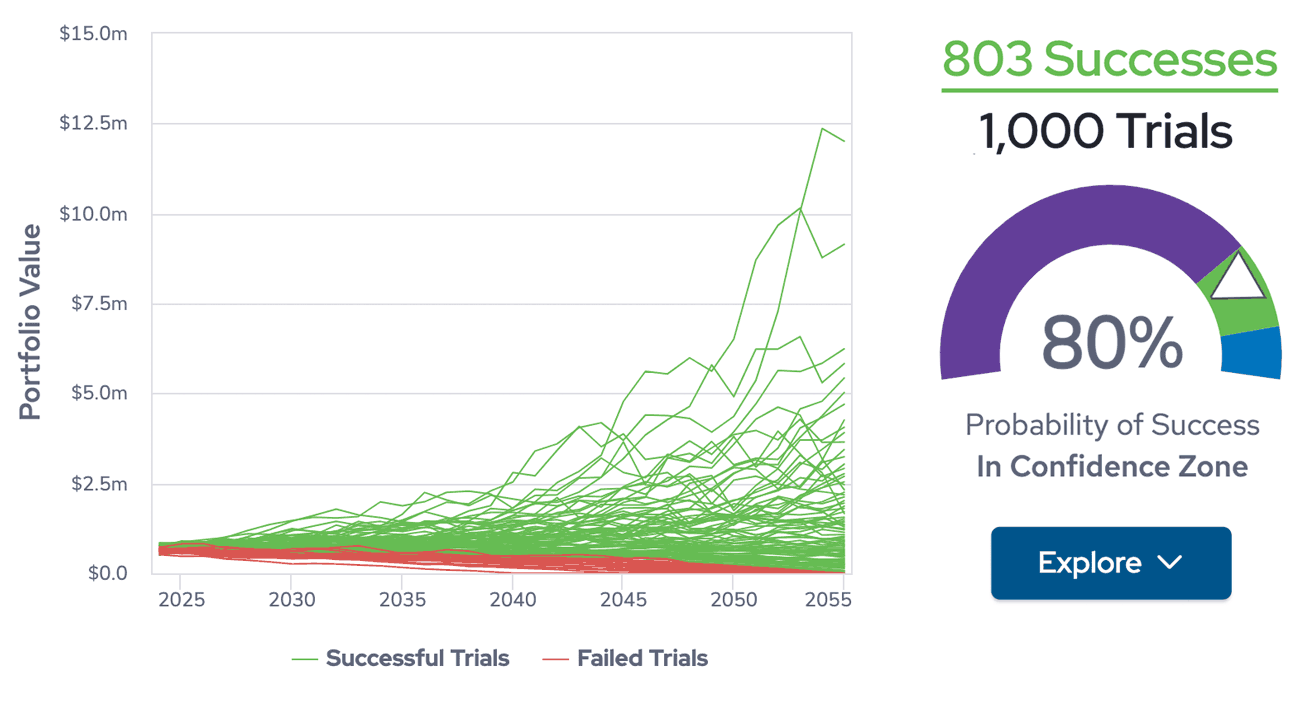

Below is a link that says “1000 Trials.” Clicking that link launches a series of Monte Carlo simulations that model possible outcomes based on Jack and Sara’s 1) longevity projections, 2) asset allocation, and 3) their needs/wants/wishes spending projections. Each of the 1000 simulations uses differing assumptions about the rate of return Jack and Sara will experience, as well as the sequence of those returns.

The results from the 1000 trials are shown in a summary graph, accompanied by a “Probability of Success” gauge. As seen in the image below, the 1000 trials based on Jack and Sara’s data found an 80% probability that their money will last if Sara lives to age 96. Eighty percent is within MoneyGuide’s “Confidence Zone” (75% - 90%), meaning that Jack and Sarah’s plan strikes a “good balance between current and future lifestyle” and “may hold up well against future shocks.” Jack and Sara would seem to be in solid financial shape as they enter retirement.

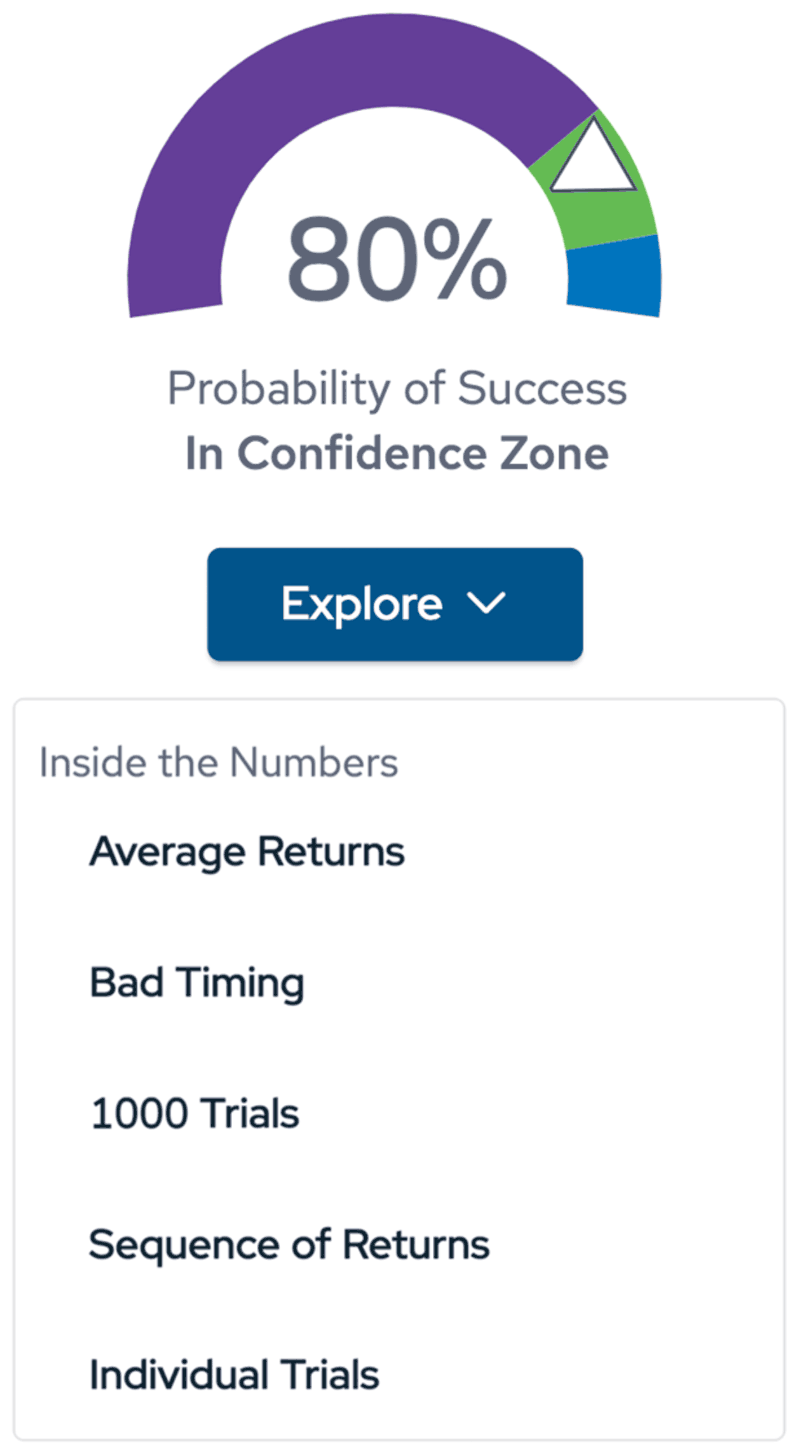

Of course, if 80% (i.e., 803) of the trials were successes, 20% (197) were not. Jack and Sara are concerned about that so they click the “Explore” button (under the Probability of Success meter) to examine what happened in specific trials.

A drop-down menu (see next image) offers several options, including a “bad timing” projection that shows the potential impact of a bear market early in retirement.

For now, Jack and Sara choose “Individual Trials” and examine the results of several specific trials using the slide bar at the top. (Sliding the bar to the left highlights the better outcomes; sliding it to the right highlights the not-so-desirable outcomes.)

Next, they choose “Cash Flow Chart” (using the “Explore” drop-down menu). This action generates a table based on the average of all 1000 trials.

The table is quite large, so we’ve reproduced a truncated and simplified version below that shows the disposition of Jack and Sara’s financial resources for only the first decade of their retirement. The full table in Envestnet MoneyGuide continues until 2055 when their plan ends. (Note: Projected investment performance is based on “average returns” for their 50% stocks/50% bonds portfolio).

Looking at the years 2026-2028, Jack and Sara see that in those years, they will need to make relatively large withdrawals from their investment holdings to meet their projected spending. However, starting in 2029, when their non-investment income rises as Jack’s Social Security benefits start, they will need lesser withdrawals, even after taking into account the added expense of their 2029/2030 home remodeling project.

Click on table to zoom

At the bottom of the table, Jack and Sara can see how their portfolio withdrawal rate changes year by year. It begins at just under 7.0% in 2026, rises slightly in 2027 and 2028, then drops below 5% once Jack’s Social Security benefits begin.

They also can see that, despite substantial withdrawals in the first three years of retirement, the value of their investment portfolio remains relatively stable because of the earnings generated. The portfolio’s low point is in 2029. After that, earnings outpace projected withdrawals until the end of the plan in 2055, meaning that they should be able to meet their needs, attain their wants, and have enough remaining to fulfill their wishes of leaving money to their children and grandchildren. (Bear in mind that the projected returns are not assured. Jack and Sara’s actual investment performance could be better or worse.)

Our hypothetical couple returns to the “Explore” drop-down menu and selects “Combined Details.” This action generates another pop-up window that, at the top, shows a “Portfolio Value Graph.” Scrolling past the graph, Jack and Sara look at a related “Portfolio Value Chart” that lays out, column by column, several key projections — beginning with the current year and continuing through the estimated year of Sara’s death. The Portfolio Value Graph enables them to look at particular years in detail by clicking on the year’s number, such as “2037.”

Playtime

Now that Jack and Sara have examined their “Current Scenario,” they can “play around” with the numbers to discover how various changes in financial assumptions and life circumstances could affect their plan. To do this, they close the pop-up windows and click again on “Results” at the top. This time, rather than selecting “Current Scenario” from the drop-down menu, they choose “Recommended Scenario.” Then, from the links on the left, they select the “Play Zone®” option.

The Play Zone® features a series of sliders that allow Jack and Sara to modify variables. Here, they can change their projected retirement age(s) and add to (or subtract from) living expenses. They can also alter projected expenditures related to health care, travel, giving, etc. In addition, they can project the impact of up/down changes in average investment returns.

Using the Play Zone®, our hypothetical couple may find they have more leeway to spend money on travel than they anticipated. They may also discover that even if their returns are somewhat lower than what they’re hoping for, they’d still be able to fund most of their goals.

After using the Play Zone® to see the impact of modifying spending goals or earnings assumptions, Jack and Sara turn to another area of MoneyGuide to “stress test” their plan. This area is called “What Are You Afraid Of?” (The link to this section is found by clicking “Return” from the Play Zone® and then scrolling to near the bottom of the page.)

At the left on the “What Are You Afraid Of?” page, Jack and Sara see a list of threats to their future financial well-being, including outsized healthcare expenditures, higher-than-expected inflation rates, a massive market decline, and the early death of a spouse. They’d like to think that none of these will happen, but Jack and Sara are realistic. Such things do happen, and they know it’s wise to consider how such events could affect their plan.

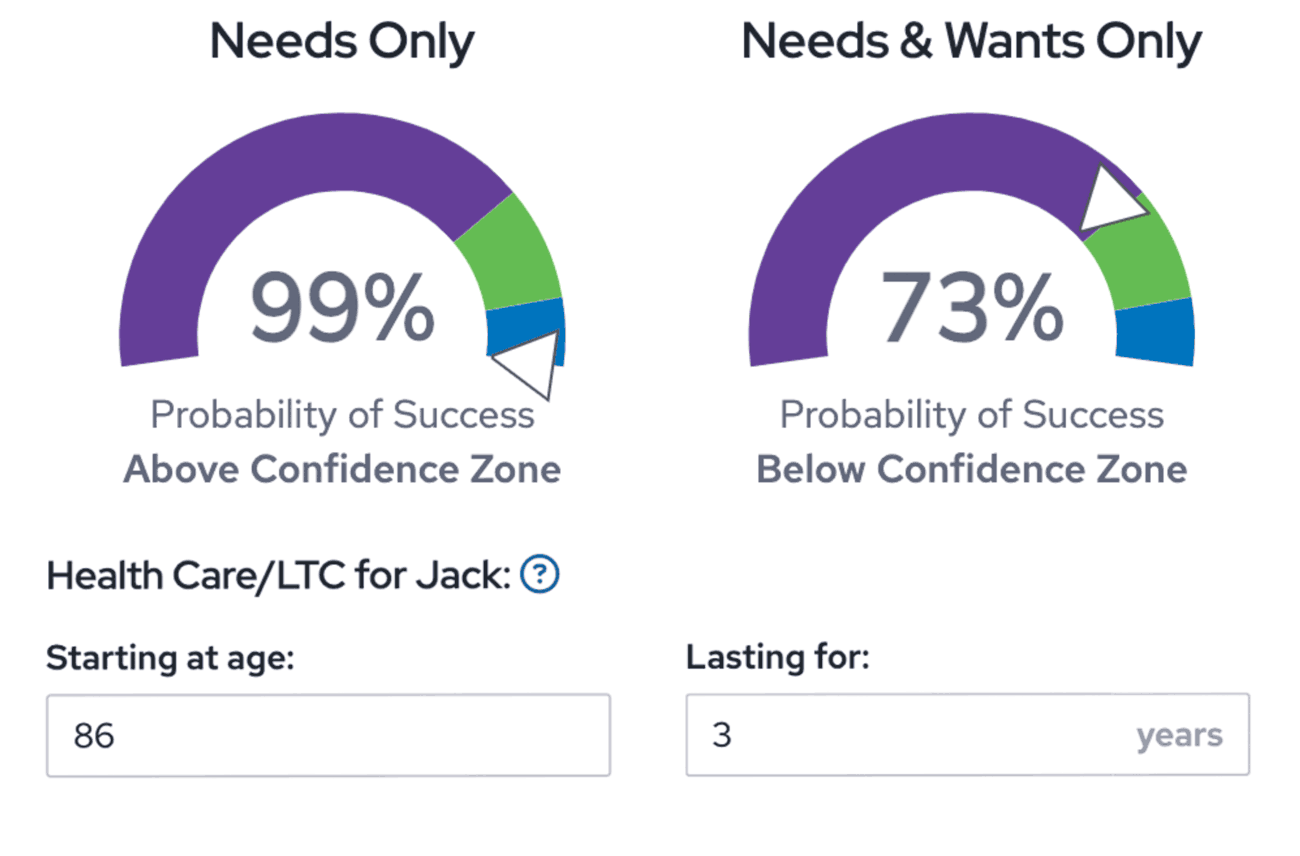

The “What Are You Afraid Of” section of MoneyGuide, rather than providing a single “Probability of Success” gauge, has three — one indicating the impact of adverse events on Jack and Sara’s ability to fund “needs,” another that combines “needs and wants,” and a third (if applicable), that combines “needs, wants, and wishes.”

To run a stress test for healthcare spending, our couple clicks the link that says “Health Care/LTC” (long-term care) and chooses a scenario. They select three years of long-term care for Jack starting at age 86 and costing $75,000 a year. The image below shows that even considering a long-term-care expense, Jack and Sara’s plan would meet basic living-expense needs. However, that additional spending would hamper their ability to fulfill their “wants.”

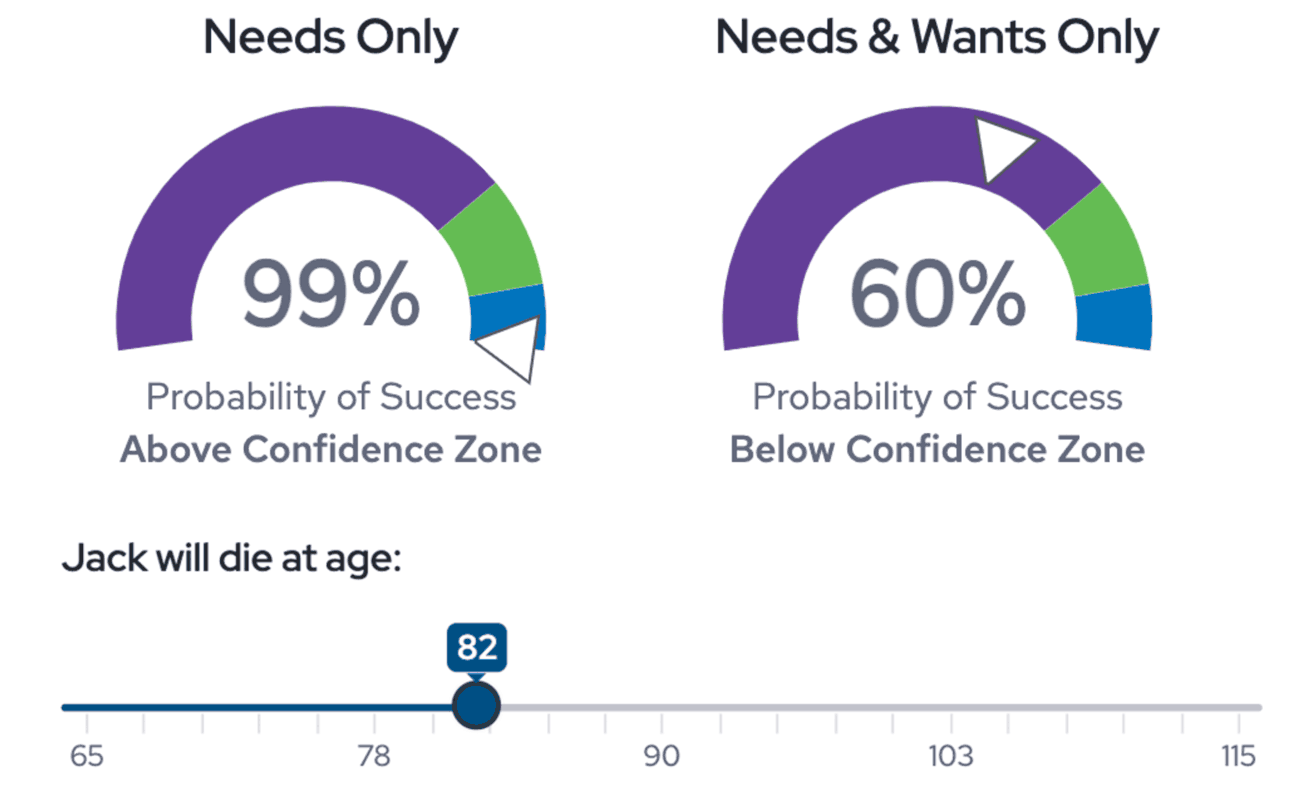

Next, Jack and Sara want to consider the possible impact of 1) a long-term care expense (this time starting at age 79) followed by 2) Jack’s death at age 82 (rather than at age 89, as in their original plan). First, they run the long-term-care scenario. Clicking the “Lock” box (not shown in the image) preserves the data so it can be combined with the next early-death test.

As the next image illustrates, even with Jack’s extended illness and early death, Sara is still able to meet her basic needs (left gauge), but the Probability of Success drops sharply on the “needs and wants” gauge (right gauge). In part, this is because of what will happen with their Social Security income. Although Sara will start receiving Jack’s higher Social Security benefit when he passes away, she will lose her own monthly benefit.

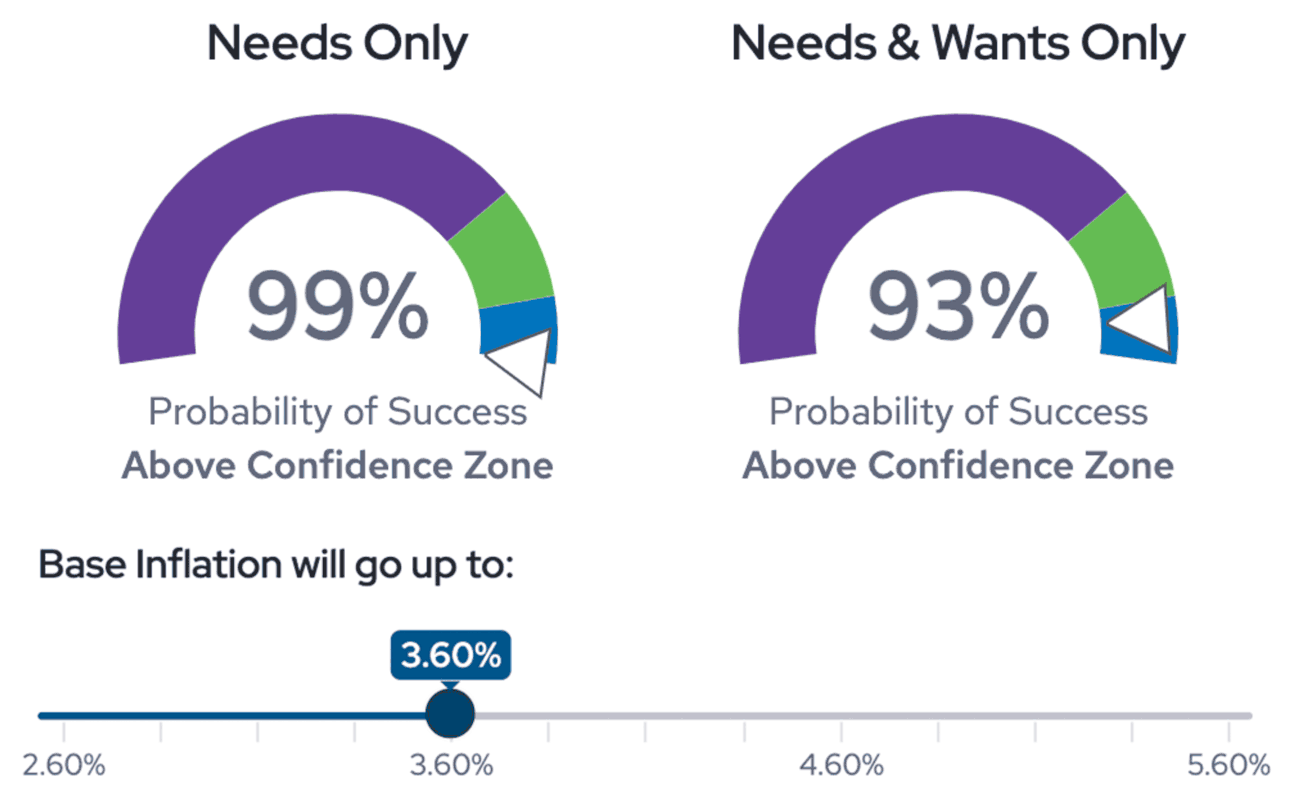

After running those two stress tests, Jack and Sara clear the variables (using the “Clear All Values” link) and run a test showing the impact of higher-than-expected inflation. They want to know what would happen if the inflation rate over the course of their plan averages 3.6% rather than the default rate of 2.6%. As seen in the final image below, that single change affects Jack and Sara’s ability to fund all their “needs and wants.”

Additional MoneyGuide tools that enable Jack and Sara to gauge various possibilities — and make informed decisions — include Choices, the What If Worksheet, and SuperSolve® — all found in the Recommended Scenario area.

After running several scenarios and tests, Jack and Sara may decide it would be better for Jack not to retire at 66 but to continue working a couple of more years (either full– or part-time). That would enable them to reduce the early-years drawdown from their retirement accounts, helping ensure they could handle financial shocks later and still have money to leave to their children and grandchildren. Or perhaps they may realize it would be wise to cut back on a few “wants” (maybe fewer or less expensive trips) to create a greater margin of safety for dealing with the possibility of a costly illness, an earlier-than-expected death, or higher inflation.

Although Jack and Sara come away from this exercise thankful that, if all goes well, they should be able to live comfortably in retirement, they also understand how their financial future could change significantly if certain events occur. They know they must plan accordingly.

They also realize using MoneyGuide to do this kind of analysis shouldn’t be a one-time thing. Life isn’t static. Living expenses and health conditions can change. Aspirations evolve. Investment returns can be worse (or better) than expected.

That’s why SMI suggests running an updated MoneyGuide analysis at least once a year. Typically, that review process will be brief. Of course, there may be occasions when you’ll want to invest more time updating and refining your plan.

For sign-up details and to learn more about using MoneyGuide, visit soundmindinvesting.com/moneyguide.