When it comes to learning to invest, there is no substitute for experience. You first have to understand some of the theory, of course, such as the difference between a traditional mutual fund and an exchange-traded fund. But much of an investor’s education comes from doing — opening a brokerage account, learning the broker’s website (or app), and, finally, making a few investments. In doing so, a new investor builds knowledge and gains skill.

To be sure, trial and error is involved, but that is true in any field of endeavor.

Until recently, it was difficult for a minor to gain hands-on investing experience. “Custodial” accounts (“UGMA” and “UTMA” accounts) require that trades be made by an adult until a young person reaches 18 (age 21 in some states). This is also true of the new Trump Accounts launching July 4. An account holder has no control over the money until age 18.

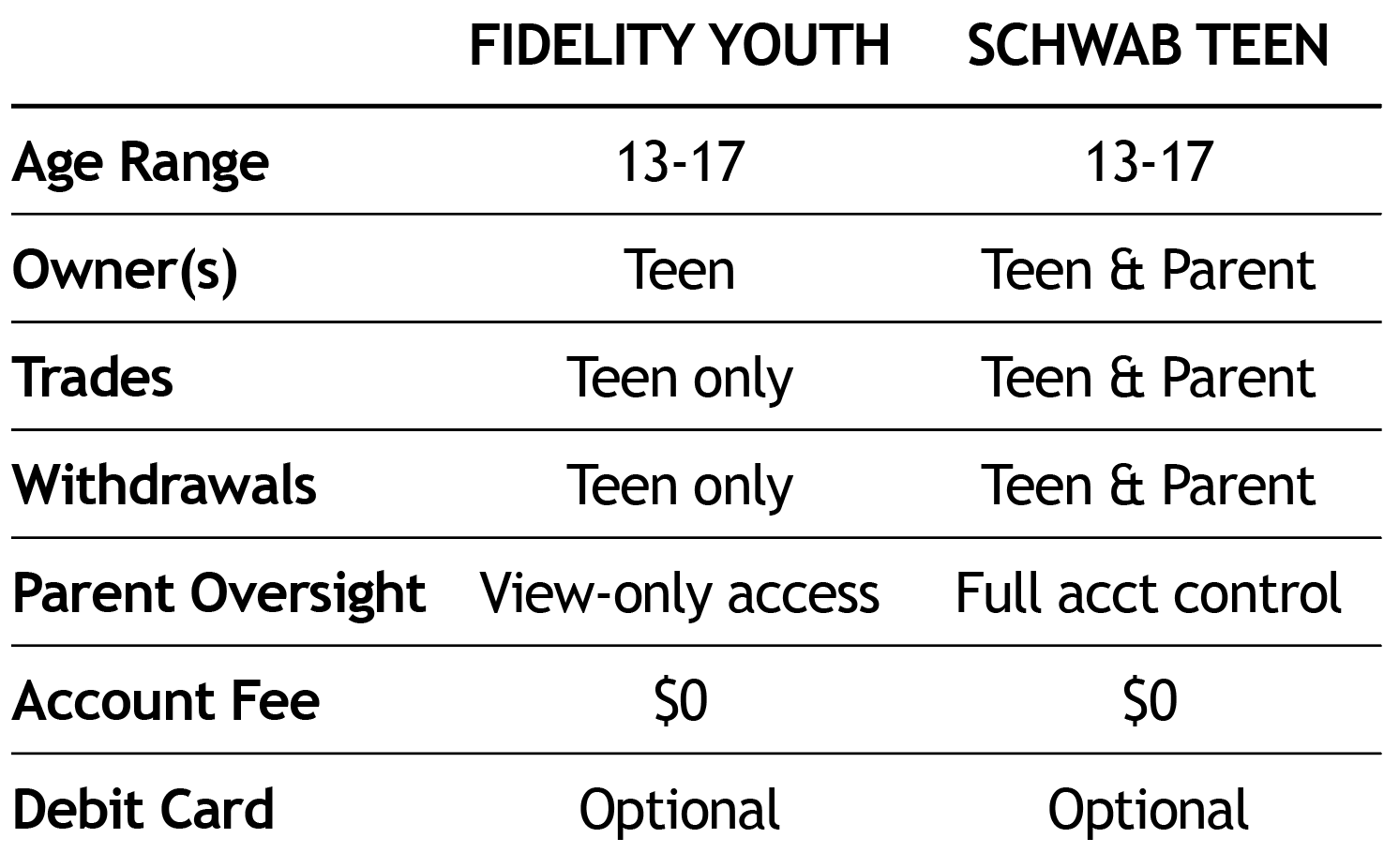

Now, however, brokerage firms Fidelity and Schwab have rolled out taxable investment accounts that allow teens as young as 13 to manage investment trades. The new teen-oriented accounts from Fidelity and Schwab offer similar investment options and restrictions but differ in the level of parental oversight.

(Fidelity and Schwab will continue to offer custodial accounts over which a parent retains full control.)

The Fidelity Youth Account

A teenager isn’t allowed to open a Fidelity Youth Account alone. Instead, a parent with an existing Fidelity account must open it. However, once the young person’s Fidelity account is funded, typically via a transfer from the parent’s account, the teen assumes control and can trade through the Fidelity Youth Account app (or the Fidelity website) without further parental approval.

Optionally, with a parent’s approval, teen users can get a debit card linked to the investment account, enabling easy withdrawals for spending.

It’s important to note that the Fidelity Youth account is not a custodial or joint account. The teen is the account owner and decision-maker. A parent can monitor investment activity and debit card withdrawals (via online alerts and statements) but is not allowed to make or block trades. However, Fidelity stresses that parents “retain the ability to close the account and/or cancel the debit card.”

Investment options in a Fidelity Youth Account include most U.S. stocks, a few international equities, selected ETFs (including fractional-share investing), and Fidelity-branded traditional mutual funds. However, teens may not trade options, buy on margin, or short-sell.

Upon turning 18, a Youth Account holder will have a 60-day window to convert holdings to a regular Fidelity brokerage account.

The Schwab Teen Investor Account

Although similar to the Fidelity Youth Account, Schwab’s taxable investing account has a key difference: it is a joint account held by a parent and a teenager, rather than by a teen alone.

“Once the account is open, the parent or guardian will have full visibility and authority on the account as a joint owner,” Schwab notes on its website. A parent does not need an existing Schwab account to open a teen account.

Investment options with a Schwab Teen Investor Account include most U.S. stocks, traditional mutual funds, ETFs, and U.S. Treasury bills and bonds. Teen investors can also put money into Schwab-curated “theme” portfolios focused on specific sectors. Additionally, a Teen Investor Account offers access to Schwab’s advanced “thinkorswim” trading platform, if desired.

Like Fidelity’s teen account, the Schwab Teen Investor Account offers an optional debit card for easy withdrawals.

Tax considerations

Fidelity Youth and Schwab Teen Investor accounts are taxed the same as custodial accounts, with the minor considered the owner for tax purposes.

Generally, unearned investment income is taxed under the federal “Kiddie Tax” rules, meaning the first $1,350 in earnings is tax-free. The next $1,350 is taxed at the teen’s tax rate, usually 0% for long-term capital gains or 10% for ordinary income. For any earnings that exceed $2,700, different rules — that affect parental taxes — apply. (Dollar amounts in this paragraph are for 2026.)

Pros and cons

As mentioned earlier, there’s no substitute for hands-on experience when learning to invest. Unlike custodial and Trump accounts, these new teen-oriented accounts enable young people to gain experience while still under their parents’ roof.

However, as medical doctor Jim Dahle, founder of the White Coat Investor blog, notes, “Young people do stupid things,” in part because the “frontal cortex [of the brain] is not fully developed until age 25.” So it would not be unusual for a teen who has full control of an investing account to make ill-considered and costly decisions.

Dahle notes that a negative investing experience at a young age could cause lasting harm. “The last thing you want to do is put a fear of investing into your teen that lasts throughout their life.”