Many investors regret not starting early enough. By failing to take greater advantage of the relentless power of compound interest, their portfolios are much less robust than they could have been.

However, there are obstacles to starting early. Most children, obviously, don’t know enough to begin investing, and even if they did, they wouldn’t qualify for tax-advantaged accounts like IRAs that require earned income. As for parents with young families, many are just trying to make ends meet and lack the surplus to set up an investment plan for their kids, except possibly a college-savings fund.

With the passage of the One Big Beautiful Bill Act last year, Congress and the Trump administration eliminated those barriers by establishing a new type of long-term investing account specifically for children and teens: the “Trump Account.” (That’s not a nickname. It’s the official name, designated in Section 530A of the Internal Revenue Code.)

Trump Accounts are similar to traditional IRAs, but they can only be opened and contributed to until age 18. However, the beneficiary need not have earned income, and there is no requirement to use the proceeds for a specific purpose (as with 529 college-savings plans).

During the “growth period” — that is, until age 18 — no withdrawals are permitted. After that, the account functions like a traditional IRA, with the same contribution and withdrawal rules. As with traditional IRAs, withdrawals will incur taxes. Early withdrawals, i.e., before age 59½, will incur penalties if the proceeds aren’t used for qualifying expenses. Alternatively, a Trump account could be converted to a Roth IRA once the growth period has ended, as long as the account holder pays taxes due on investment growth and any pre-tax contributions.

According to Treasury Secretary Scott Bessent, the idea behind Trump Accounts is “creating an ownership economy where all citizens become shareholders in America’s wealth.” Bessent notes that about 38% of American adults currently have no stock ownership. “With Trump Accounts, over time, we can get that number down to zero.”

Who is eligible?

Trump Accounts are only available to U.S. citizens under 18 who have a valid Social Security number. Any authorized adult — typically a parent, legal guardian, or grandparent — can open a Trump account. Only one Trump account can be opened per beneficiary. (If multiple people try to open an account for the same child, the IRS will choose which application has priority.)

When the web portal becomes fully operational later this year, accounts can be opened at www.trumpaccounts.gov. Alternatively, applicants can request an account by submitting Form 4547 with this year’s (2025) tax return. The IRS will send out account activation details starting in May, and accounts are scheduled go live on July 5, 2026.

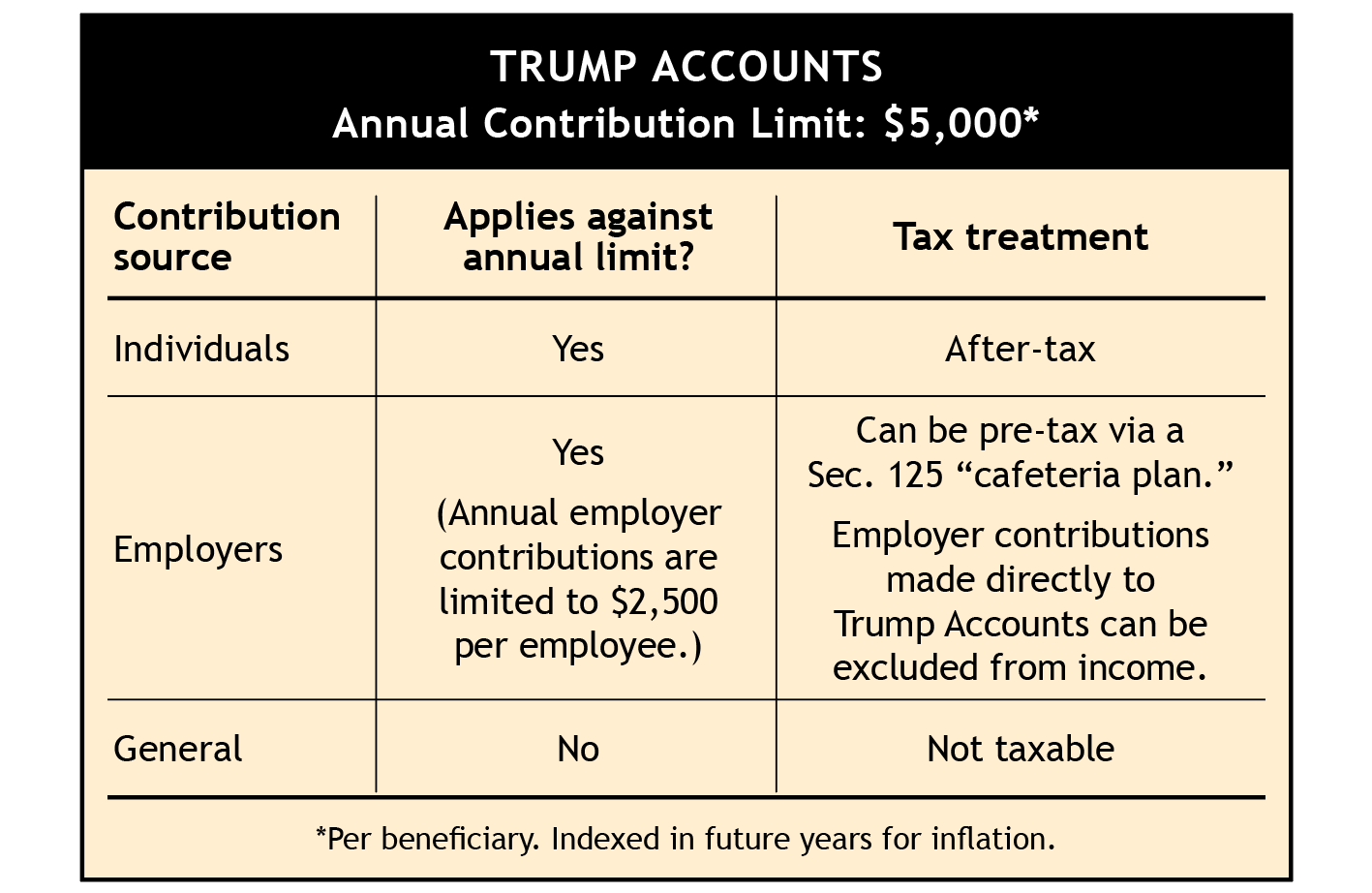

Contribution sources

Trump Accounts will accept funding from individuals and employers, as well as general donations from charitable organizations. Children born between Jan. 1, 2025, and Dec. 31, 2028, will have one additional funding source: Uncle Sam. These children will qualify for a $1,000 seed deposit from the U.S. Treasury.

The table below outlines the contribution rules for each of the three regular funding channels. Contributions from individuals and employers are limited by an annual cap of $5,000. For example, parents, grandparents, and an employer could all contribute to a Trump account for a child or teen, but their total contributions cannot exceed the annual limit.

Furthermore, the $2,500 employer limit applies per employee, not per beneficiary. For instance, even if an employee has multiple children with Trump Accounts, the total employer contribution still cannot exceed $2,500 within a calendar year.

Contributions via the third potential funding source for Trump Accounts — “general contributions” made by charities (and perhaps state or local governments) — do not count toward the annual limit. However, other restrictions will limit the amount of money available through general contributions.

Under the law, such contributions must be broadly directed to “qualified classes” of beneficiaries, such as all Trump account holders within a specific age range or a particular state or geographic region. The billionaire Dell family, for example, is donating $6.25 billion to eligible children ages 10 and under living in ZIP code areas where the median household income is no more than $150,000.

The financial-planning website Kitces.com points out that “each general contribution must by definition fund at minimum thousands (and perhaps millions) of [accounts]—meaning that they require substantial resources to fund, which even then might not amount to materially large contributions for individual recipients.” Even though the Dell contribution is perhaps the largest charitable gift in U.S. history, it will translate to $250 per recipient.

How is the money invested?

During the growth period, up to age 18, Trump Account funds must be invested in a traditional mutual fund or ETF that tracks a major U.S. stock market index. Additionally, the law requires these funds to be free of leverage and to have annual fees no higher than 0.1%.

Details about which funds qualify and how many different funds an account holder can use within a Trump Account have not yet been announced.

A sweet spot for Roth conversions

As noted earlier, once an account holder reaches age 18, his or her Trump Account effectively becomes an IRA. But don’t overlook the attractive option of converting the account (or part of it) to a Roth IRA. Taxes will be due, yes, but most 18-year-olds probably will have little or no earned income and therefore will be in a low marginal tax bracket.

For example, suppose that during the growth period, a Trump Account has grown to $100,000, half of which is taxable (due to investment growth and pre-tax contributions). Although it is impossible to precisely forecast future tax rates and standard deductions, it seems likely that most of the taxable dollars converted to a Roth would be taxed at the lowest or second-lowest prevailing rate. Put another way, one’s late teens is likely to be a tax-friendly time to do a Roth conversion.

Here is something else to consider. To further encourage a young person to do a conversion during that low-tax time of life, a parent or grandparent could offer a cash gift to cover any tax costs.

Having a well-funded Roth IRA by age 18 used to be all but impossible due to earned-income requirements. In the future, what was once impossible may become common, thanks to the introduction of Trump Accounts.

An attractive new choice

Vehicles for saving for a child’s future have expanded significantly in recent decades. They now include 529 plans, Coverdell accounts, Roth IRAs (for children with earned income), and accounts available under the 1960s-era Uniform Gifts to Minors Act and the 1980s-era Uniform Transfer to Minors Act.

Trump Accounts offer one more option, highly attractive not only to parents of children who qualify for the initial $1,000 seed money but also to families looking at the longer term. Parents will now have yet another instrument that can help guide their children toward a lifetime of financial well-being.