One aspect of being a serious steward is to prepare financially for death. For most of us, part of that preparation involves purchasing life insurance.

All life insurance policies include a “death benefit” that helps support the loved ones left behind, but a buyer of life insurance must choose among various options. For example, some policies, in addition to providing a death benefit, are designed to serve as a savings or investment vehicle, creating an asset that a policyholder can borrow against or cash out if the policy is no longer needed.

Temporary or permanent?

The two main types of life insurance are “term” insurance, which expires after a specific period, and “permanent” insurance, which doesn’t expire.

A term insurance buyer, besides choosing a death-benefit amount, must select a coverage period. A buyer of permanent insurance needs to choose among “whole life,” “universal life,” and “variable life.” Whole life is the most common, but the other options may offer more flexible benefits and additional ways to invest a policy’s cash value.

What do you want?

The best type of life insurance policy for you depends on what you want it to do. If you’re only seeking an affordable way to support your loved ones if you pass away, term insurance is the better choice. The cost of term mainly depends on your life expectancy. Because it’s unlikely you’ll die during the policy period, and since term policies have no add-ons or extras, this type of life insurance remains quite affordable.

In contrast, since permanent insurance doesn’t expire, the insurance company knows it will pay a claim eventually. The inevitability of a future claim causes the company to charge a higher premium. Additionally, permanent insurance typically offers features that term insurance doesn’t, which further increases the cost of premiums.

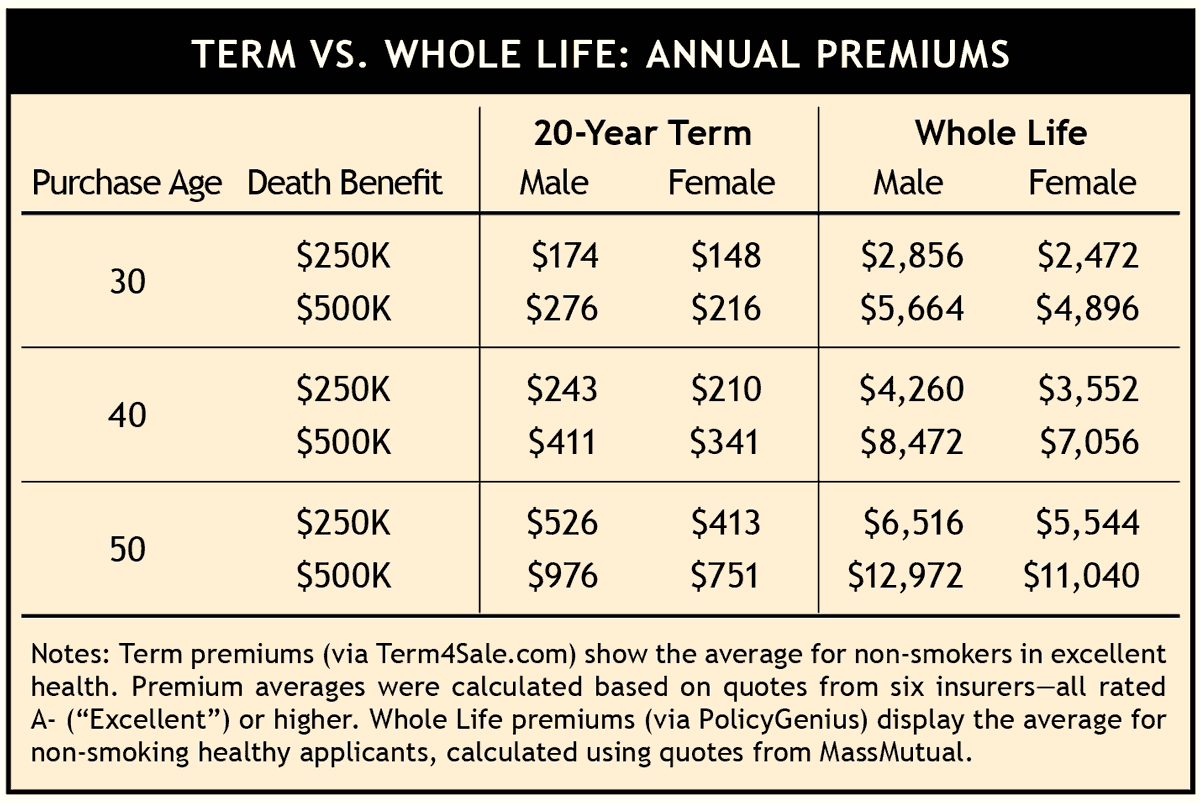

Apples-to-apples comparisons are challenging because there are numerous policy variations. However, generally speaking, a buyer will likely pay 8-15 times more for permanent insurance than for term insurance — even if both types of policies offer the same death benefit (see table below).

Term is straightforward

Term insurance is often referred to as “pure insurance.” The policy pays a benefit if you die during its term, which typically lasts 10, 20, or 30 years.

For a 20-year level-term policy, a 30-year-old buyer might pay an annual premium of $150 to $175 for a $250,000 death benefit. When the 20-year period ends, the policy is terminated. Unlike “permanent” insurance policies, term insurance doesn’t build “cash value” — meaning you can’t borrow against a term policy, nor can you get money back if you cancel coverage.

In some situations, a term policy can be renewed after it expires, though at a higher premium. Additionally, some term policies are convertible to permanent insurance.

Besides the length of coverage, premiums for term policies are affected by several other factors, including age at purchase, overall health, occupation, personal habits (smokers pay more), and gender (women usually pay less because they tend to live longer).

Permanent insurance: Extras at a price

Unlike term insurance, permanent insurance provides a guaranteed death benefit and accumulates a “cash value” while you’re alive. In other words, this type of insurance functions as a growing financial asset.

The most common type of permanent life insurance is “whole life.” As with term insurance, the younger the buyer, the lower the premiums will be. With most whole-life policies, the premium amount remains fixed until age 100, even if the policyholder’s health deteriorates. (Some whole-life policies charge premiums for a shorter specified period, rather than to age 100.)

Meanwhile, the policy’s accumulating fund earns tax-deferred interest, usually with a guaranteed minimum growth rate (the average yearly guaranteed rate for whole-life policies is typically 1% to 3.5%, according to insurance broker Quotacy). If you’re considering permanent insurance, compare a policy’s projected return to what you could earn through other savings or investments.

Besides the gain from the accumulating fund, some whole life policies offer tax-free dividends from the insurance company’s profits. These dividends can increase the policy’s cash value, be paid directly to the policyholder, or help cover premium costs.

At some point, certain types of whole life policies can become “paid up,” meaning that the cash value is sufficient to stop paying premiums and yet have the policy remain in force.

If desired, a policyholder can use the cash value of permanent insurance (if significant enough) to secure a preferential-rate loan from the insurance company. If the policyholder dies before the loan is repaid (including interest), the death benefit will be reduced accordingly.

Some policies allow trading in the cash value for a higher death benefit. This can be a smart choice because any cash value left at death isn’t paid out to beneficiaries as extra money. (Instead, the company uses the cash value to help fund the policy’s stated death benefit.)

Reasons to go the permanent route

One reason people purchase permanent insurance, despite its much higher cost, is to secure future insurability regardless of any health problems that may develop. Permanent insurance can also act as a source of income during retirement, with withdrawals from the policy’s cash value supplementing other retirement income. (However, such withdrawals will reduce the death benefit.)

Increasingly, buyers of permanent life insurance are using their policies to hedge against potential long-term care (LTC) expenses. Some policies offer a low-cost “rider” that allows certain LTC costs to be deducted from the death benefit (not from the cash value). In most cases, to qualify for LTC benefits, the policyholder must be diagnosed with a chronic illness — such as cancer or Alzheimer’s disease — that requires long-term care. Essentially, the policy’s death benefit is “accelerated” to cover long-term care needs. (Accelerated benefits are allowed under some term policies in cases of terminal illness.)

Making the decision

Although buying life insurance isn’t a one-size-fits-all proposition, term insurance is clearly the more affordable choice. Many personal-finance experts recommend a death benefit of 5-10 times a person’s annual gross income, which is much more budget-friendly with low-cost term coverage. (Be sure to consider coverage for a parent who stays at home with children.)

Although permanent insurance has appealing features, its cash-accumulation options are limited and typically yield lower returns. Instead of investing via an insurance product, selecting a low-cost term policy and investing the difference yourself (preferably through an IRA) will likely result in a significantly higher rate of return. That is why SMI has traditionally recommended this approach in most cases.