Building an investment portfolio requires considering many financial and emotional factors. What gets less attention is the need to consider similar factors when determining how to create a stream of retirement income in later life. For this, a framework to help people choose a strategy would be helpful. This article describes an assessment tool to help individuals find a firm starting point from which to make their retirement plans.

Retirement researcher Wade Pfau has addressed that need, and Morningstar columnist Christine Benz interviewed Pfau to learn more about it.

Christine Benz: You think identifying a personal retirement income style is foundational to the retirement planning process. Discuss that idea.

Wade Pfau: There are different approaches to retirement. There are investment-based approaches, there are bucketing approaches. There are income-flooring approaches, where you build protected lifetime income.

There’s much disagreement about which one is best. Ultimately, there is a role for different strategies based on what makes someone most comfortable. But there has never been a framework to help people choose a strategy. The idea behind our work was to develop a tool to help individuals find a firm starting point from which to make their retirement plans.

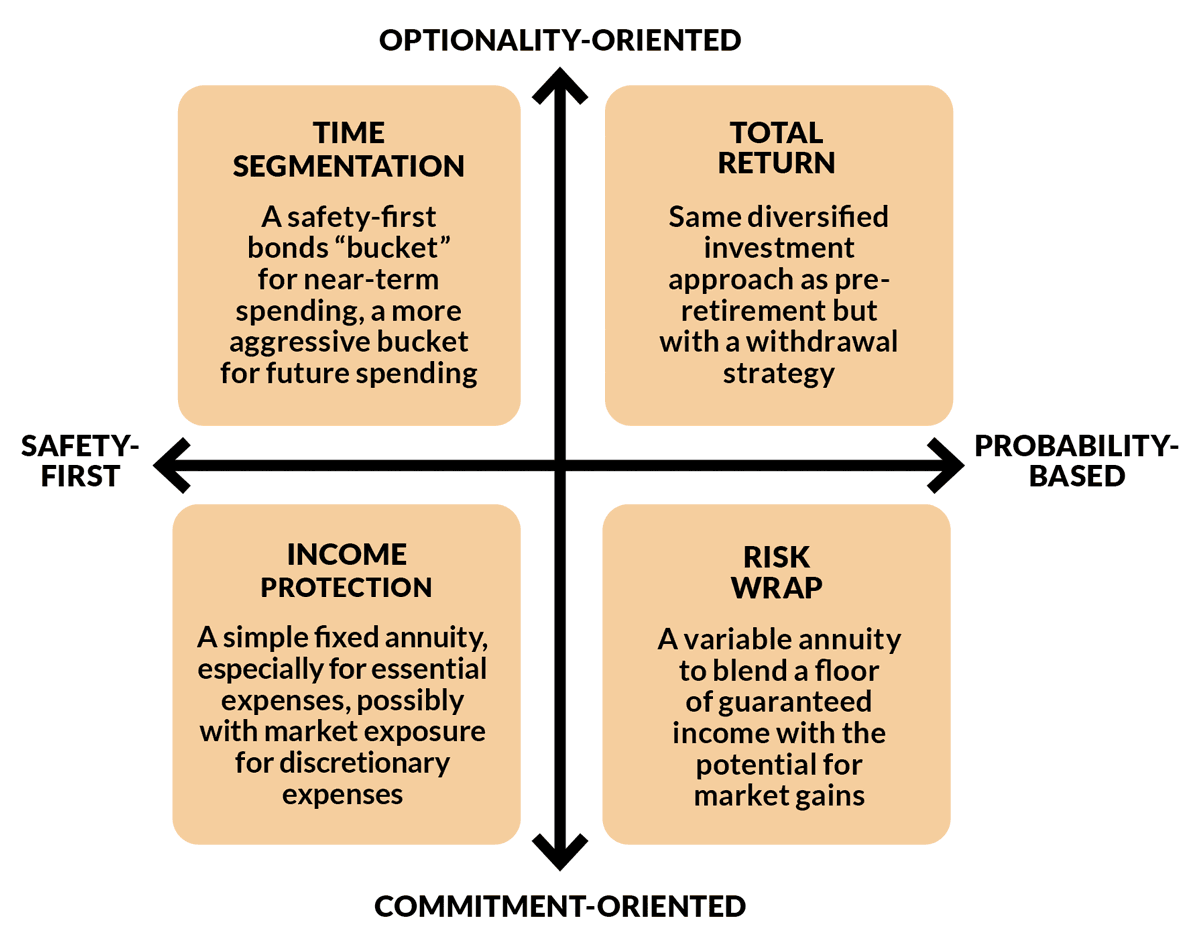

We have identified two key areas where retirees might differ on their retirement income preferences. The first is their attitude toward the safety of their income stream: Are they “probability-oriented” or do they have a “safety-first” mindset? The second key area relates to whether they’re willing to commit to a single retirement income strategy or if they prefer optionality to make more adjustments along the way. We used these four variables to form the RISA (Retirement Income Style Awareness) Matrix. Taking the RISA assessment will show you where you land in each of those two key areas.

If I find that my retirement income style is more investment-based — I’m probability oriented and have an optionality mindset — I can plan with more confidence. I don’t need to consider annuities. But if my style is safety-first, then maybe I do want to start learning about annuities. Whichever approach suits me best, I have a better starting point.

Rely on probabilities or prefer safety first?

Christine: Let’s start with the first key decision, whether [pre-retirees] prefer a “probability-” or a “safety-first” approach.

Wade: Probability-based means that you’re more comfortable relying on the idea that stocks will probably continue to outperform bonds and therefore should support a higher standard of living in retirement than you could get with bonds alone.

Christine: What types of income sources would fall under a safety-first umbrella, and what type of retirees would tend to gravitate toward it?

Wade: With safety-first, you may still feel comfortable with the idea of stocks for the long run, but you’re less comfortable with the idea that you can rely on the stock market to cover your core spending in retirement. You want some sort of contractual protection behind that income. Of course, that starts with Social Security and deciding when to start claiming in order to provide the most longevity protection and an inflation-adjusted income. It also includes traditional pensions.

Your protection could further include holding individual bonds to maturity, more so than using traditional bond mutual funds or ETFs. Then, if there’s still a gap between core expenses and guaranteed income, someone might look to annuities as an additional way to fill that gap.

On top of that, there’s always a role for investments, including stocks. Even if the markets don’t do well, you’ve got your basics covered through other income sources. Someone who’s more interested in the safety-first approach is going to feel more comfortable having their basics covered with contractual protections, and then, if that helps them feel more comfortable investing the rest more aggressively, they have that potential for growth.

Freedom to flex or long-term commitment?

Christine: The second key decision relates to what you call “optionality” versus “commitment.” Can you discuss what the difference is?

Wade: If you have an optionality orientation it means you value flexibility for your assets above all else. You want to be able to make changes and you would be comfortable with income fluctuations. You want to respond to new opportunities.

Whereas if you have a commitment orientation, it’s likely that if you can find something that will solve for your lifetime retirement income need, you would prefer to commit to that. Then you can take income planning off your to-do list and not have to worry about it. There are also some nuances around commitment orientation to help manage potential cognitive decline as you age or to protect other family members.

Christine: You’re saying that someone who prefers optionality would say, “I want to continue to manage my portfolio. I want to have liquid assets in it” and so forth. Whereas if someone’s very commitment-centric, a great example of something they might do is purchase an annuity, a one-and-done decision that creates that income stream for the rest of their life.

Wade: Right, and these are both valid preferences. There are annuities that provide some flexibility. But if you think of a simple income annuity, that’s an irreversible commitment. That would be the purest form of a commitment strategy.

[Editor’s note: Among the approaches discussed below, SMI typically favors a “Total Return” approach, assuming Social Security will fill much of the “Income Protection” role for most investors. But it’s wise to understand the broader picture that includes other options.]

Retirement income style 1: Total Return

Christine: You note that a self-assessment of how they feel about all of these factors can help retirees plot themselves in one of four quadrants, representing four different retirement income styles. Let’s examine each of these styles, starting with the total return investing style. What types of investments and strategies are part and parcel of this approach?

Wade: The total return investing approach is generally the default because it’s the most closely aligned with one’s pre-retirement life. It aligns with the probability-based and optionality preferences. In the pre-retirement world, you build a diversified investment portfolio to grow your wealth, and then at retirement you just flip a switch. You’re no longer adding new savings; you’re now taking distributions. But you otherwise use the same sort of diversified investment portfolio, and you develop some sort of systematic withdrawal strategy.

When financial advisor Bill Bengen first developed the 4% rule, he told retirees never to hold less than 50% stocks in retirement. That idea relies on the notion that stocks will outperform bonds, and you need to use a hefty allocation to stocks to get enough growth to fund a higher level of spending in retirement. This approach is very much probability-based and it’s also optionality-oriented, as we traditionally think of investments as providing more flexibility for the financial plan.

Christine: One central consideration for someone using a total return style is that they have to figure out how much they can safely spend from that total return portfolio per year. You’ve done a lot of research on that topic. What are your main takeaways?

Wade: The years 1966 to 1995 triggered the 4% rule. In that 30-year period, the average market return wasn’t necessarily so bad. But it was only after 1982 that the markets did great. From 1966 until 1982, it was a rough market environment with high inflation for a number of years and double-digit losses in the S&P 500. So the retiree didn’t get to enjoy that full average performance because they decimated their portfolio before the good returns came. That’s sequence-of-returns risk in action, and it’s maximized by having constant spending from a volatile portfolio.

Christine: How can someone mitigate sequence risk?

Wade: There are four ways. The first is to spend conservatively. Another option is to spend flexibly. If I can adjust spending along with market performance, that manages the sequence-of-returns risk because I’m not having to sell as much from a declining portfolio.

A third approach is to mitigate the volatility of the portfolio, not necessarily by just investing in bonds, but with a bucketing approach, or by using an equity allocation that increases over time, once the retiree has made it through the early years of retirement, for example.

The fourth approach I call “buffer assets,” where you have something outside the portfolio that you treat as a temporary spending resource to spend from after market downturns, to help avoid selling from the portfolio at a loss. This could be just a big pile of cash on the sidelines — that was the original buffer asset. Or it could be the cash value of a “whole life” insurance policy. These assets have principal protection and are not correlated with the overall markets.

Retirement income style 2: Time Segmentation

Christine: Another retirement income style is time segmentation, often shorthanded as “bucketing.” What is a time-segmentation style, and for whom might that be appropriate?

Wade: Part of what came out of this research on retirement income styles is that there are connections between the four approaches. If you’re more optionality-oriented, you tend to be more comfortable with a probability-based approach. There’s a natural correlation between those two orientations, and a total return style is a natural strategy for such people. On the other hand, if you’re more safety-first, you tend to be more commitment-oriented. So income protection is a more natural strategy for those people.

But some individuals have preferences that don’t have that natural correlation to one another. Someone might have a safety-first orientation and want contractual protections, but also have an optionality orientation. There is an inherent conflict. How do you have optionality if you have a contract? Financial advisors began developing behavioral strategies such as time segmentation in the 1980s to address these kinds of clients.

Time segmentation involves investing differently based on the time horizon. So we’ll have a short-term bucket. We could have a medium-term bucket. You can have as many buckets as you want, but the basic idea is that the shorter-term buckets are where you get the safety-first contractual protections. You’re going to hold fixed-income assets and when they mature, they’ll provide their face value as well as any coupon payments along the way to fund those upcoming expenses.

You use bonds to cover expenses in the near term, and then you get the optionality because your long-term buckets can be focused on growth.

The behavioral story used with bucketing is that people think, “If the market goes down, I don’t have to panic, because I have these short-term buckets that are going to cover my spending as long as the market recovers before I’m forced to sell from longer-term buckets.”You might still have a 60% stock, 40% bond portfolio, just like with a total return approach. But the person with a time-segmentation approach might say, “I’ve got 40% in my short-term buckets to cover the next eight to 10 years of expenses. The other 60% is in these longer-term buckets, mainly stocks, earmarked for longer-term expenses.” It’s just a different way to frame the asset allocation choice.

For people who have safety-first and optionality preferences it can be an emotionally more satisfying way to approach building their retirement strategy.

The difference between a total return approach and a time-segmentation approach, even if the asset allocations might be basically the same, relates to decisions of rebalancing. With the total return approach, you’re generally rebalancing every year to keep your asset allocation on track. With time segmentation, you don’t necessarily rebalance on cue. It’s based more on what’s going on with the market and the portfolio. If the stock market is down, you’re just going to be spending from the bond side and not rebalancing at all.

If the stock market is doing well, that’s when you start to sell from that long-term bucket to replenish your short-term bucket. But at the end of the day, you’re still using stocks and bonds. So is there any difference to it, relative to a total return strategy? Not necessarily. But behaviorally, it may help people.

Retirement income style 3: Income Protection

Christine: It seems like the purest expression of [this style] would be just to buy a basic income annuity. Can you talk about what else the income protection style would entail?

Wade: With income protection it’s safety-first: You want contractual protections for your core spending, and you’re commitment-oriented. That’s generally the world of fixed annuities, whether it’s the simple, single-premium immediate annuity or a deferred-income annuity.

Once you have your basic expenses covered with this protected, reliable type of income source, the rest of the assets can be invested for upside. You can feel more comfortable investing the rest more aggressively. Even if the market tanks, you’ve got this income protection in place and have your basics covered. You’re not exposed to market risk. That’s the whole idea of income protection: First, build a floor of protected lifetime income and then invest the rest for upside because you have more risk capacity. Since you’ve got your basic spending covered, you can use a variable spending strategy and invest more aggressively in equities for discretionary goals and expenses.

Christine: One big knock against annuities is that inflation can eat away at the purchasing power of the income you receive. And adding an inflation rider can be expensive. Should that lack of inflation protection be a big obstacle for people who would otherwise be inclined toward an income-producing product like an annuity?

Wade: There are no Consumer Price Index-adjusted income annuities in the United States right now. There have been in the past, but the last company to offer a CPI-adjusted income annuity stopped in January 2020.

Now, you could add a cost-of-living adjustment, but that doesn’t provide inflation protection higher than whatever cost-of-living adjustment you included. So you don’t have protection against unexpectedly high inflation. But the annuity can allow you to meet more expenses over time from a given premium or given asset base than traditional, non-Treasury Inflation-Protected Securities [TIPS] bonds are able to do.

If I’m thinking about stocks and bonds versus stocks and income annuities, the income annuity allows me to meet more of my expenses than bonds, which then puts less pressure on the stocks for income needs. When you’re putting less pressure on the stocks for dividends, you have less sequence risk for the stocks, and more potential for growth. Over time we do tend to expect stocks to keep up with inflation, not necessarily over short periods, but over longer periods.

The annuity is not meant to provide inflation protection, but as part of a financial plan it can make it easier for other assets to provide that protection.

Retirement income style 4: Risk Wrap

Christine: Risk wrap is another of the hybrid sorts of styles. Can you talk about what that entails?

Wade: With risk wrap you’re probability based, so you’re comfortable relying on the market. But you also have a commitment orientation and you’re comfortable committing to a strategy. If you have these orientations you also tend to be a little bit more worried about outliving your money. It’s like you want to put some sort of guardrail around the market risk.

There are options here. The simplest way is a variable annuity with a lifetime income benefit. The variable annuity lets you invest for upside, and if markets do well, you get step-up opportunities and so forth that satisfy the probability-based preference. But you have this lifetime-income benefit so that no matter what happens, no matter how the markets fall, causing you to deplete the value of that annuity, that still triggers this lifetime-income benefit. You have a protected lifetime income. Within the same financial product, you’re investing in the market but you’re wrapping the risk through the insurance protections of the annuity contract.

Christine: This is an area that a lot of serious financial practitioners look down upon. There’s a lack of transparency with a lot of these products, and they can be very high cost. Do you think that it’s unreasonable for advisors to automatically say these products are off the table?

Wade: I do think it’s unreasonable to have a fundamental unwillingness to look at the products. I personally am risk-wrap-oriented, so I’ve spent more time looking at these types of financial products. You do have the ability to invest quite aggressively. Even if the stock market goes down, that triggers the benefit; you have this protected lifetime income. And there are low-cost versions. There are even fee-only versions. A low-cost variable annuity with upside growth potential can be a powerful way to build a retirement strategy. But it’s going to appeal more to people who have that probability-based mindset, because generally the variable annuities will have lower downside guarantees, and in the worst-case scenario, you won’t get as much protected lifetime income.

Christine: You mentioned that risk wrap is your own orientation. What do you find appealing about it?

Wade: I’m comfortable relying on the stock market, but I don’t assume a high rate of return. I’ll be very heavily invested in stocks, but I’m going to assume a rate of return closer to the bond side. I like having the protections in place. I can still calculate the worst-case scenario for my financial plan, unlike with a pure investment approach.

The annuity protection at least allows me to put a floor on what the stock market could do. Of course, even with a low-cost variable annuity, a 1% fee over time does have a huge compounding impact on terminal wealth. But if that allows someone to invest more aggressively because they feel more comfortable since they have those protections, that additional market exposure can more than offset the fees.

The other alternative for me was a simple income annuity plus stocks. Since I am more risk-wrap-oriented, I would be more comfortable with a variable annuity with a lot of upside investment freedom versus just a simple income annuity and the rest in stocks.

Christine Benz’s takeaways

There’s no single best style for generating income in retirement. Instead, finding the right retirement income strategy involves some introspection: your attitude toward taking stock market risk vs. locking in a safe stream of income; your preference for flexibility vs. a permanent solution; and whether you’d rather spend more early on to elevate your quality of life in the here and now or defer gratification to improve the odds that you won’t run out.

Like Wade, my result on the RISA questionnaire was risk wrap, but I told him that I would be disinclined to buy a variable annuity in retirement. Instead, my approach is a bit of a mashup of some of the investment styles that Wade discussed. I like the idea of locking in our fixed spending needs with Social Security and possibly a fixed annuity if Social Security doesn’t go far enough. In addition, time segmentation (bucketing) appeals to me from an investment portfolio standpoint. If a lot of our income needs are coming from non-portfolio income sources, and I think they will, our buckets will tilt toward the aggressive (stocks).

There are a couple of benefits of simple annuities that go under-recognized. The first is the fact that an annuity can provide a portion of a retiree’s income needs for life without interruption. The second is that having an annuity has the potential to give retirees “permission to spend,” which is something that wealthier retirees often struggle with. In other words, if the retiree is receiving a stream of income automatically, spending those funds or giving them away might come easier than it would if they had to tap their portfolio.