It’s a classic dilemma and one that investors spend a surprisingly large amount of time dealing with: how to invest when the data seem to suggest the market is "late" in a bull market cycle?

First, let’s establish what that even means. What signifies that we’re "late" in a bull market cycle? It’s more than just looking at the length of other bull markets throughout history (though we’re late by that measure as well). Rather, the lateness of the bull market has more to do with two other variables besides length: valuation and catalyst.

Valuation helps us compare the prices being paid for stocks today versus the past, and has been proven to be a powerful predictor of long-term future returns (over the next 7-12 years). Catalyst is what I’m calling the idea that the likely conditions are in place for the bull market to shift to a bear.

As you might expect, economists and market watchers can (and do) argue ad nauseum about this. But SMI’s contention for years has been that the current bull market wouldn’t end until the Fed had wrung the excess liquidity out of the monetary system. With seven rate hikes under their belt and more to come, plus a scheduled reduction in the Fed balance sheet accelerating in coming quarters, this condition has been met.

That said, the fact that valuation and catalyst are both in place for an eventual bear market is a far cry from saying a bear market is imminent. As we’ll see, pinning down the timing of bear markets is notoriously difficult, even when we’re highly confident one is coming relatively soon.

Current valuations

Second, why do we care whether we’re late in a bull market cycle or not? Because normally this implies that significant losses are looming. Let’s quickly review some of the valuation indicators and what they’re saying. Nine months ago, I wrote a market valuation review in which I detailed a number of indicators and their current readings. Here’s a recent update of many of those discussed at that time: 18 of the 24 are either "moderately" or "extremely" overvalued.

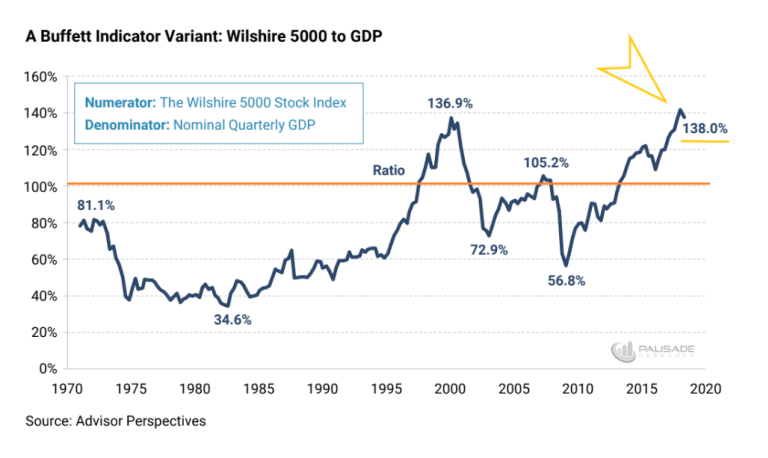

There are almost too many valuation indicators lined up against this market to count. Here’s one reported to be Warren Buffett’s favorite metric, based on him once calling it "the best single measure of where valuations stand at any given moment." It simply compares the total value of U.S. stocks to the nation’s GDP. Anything over 100% has historically been a warning to expect a decline in stock prices. By this measure, stocks are more overvalued than they’ve ever been, even at the peak of the tech bubble in 2000.

Mark Hulbert recently wrote an article in The Wall Street Journal detailing "The Eight Best Predictors of the Long-Term Market" (behind paywall, but also available here via Morningstar). The takeaway is simply that "The stock market’s return over the next decade is likely to be well below historical norms."

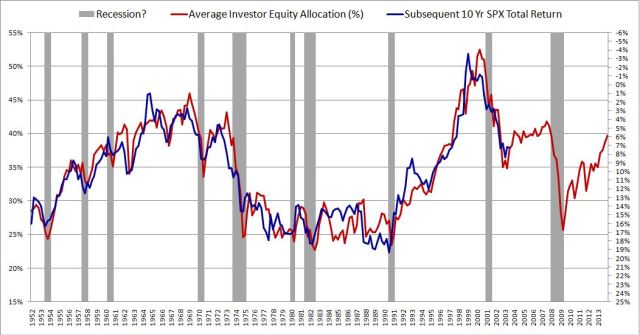

Here’s an old (2013) chart showing the historical correlation between actual stock market performance and the indicator Hulbert found to be the best historical indicator of future stock prices. It tracks the average investor’s equity allocation over time and plots that relative to the S&P 500’s future 10-yr returns. The sole reason for including the chart is simply to show how accurate this indicator has been since 1952. The red and blue lines follow each other up and down nearly perfectly over time.

Here’s what Hulbert says about this indicator today:

The most accurate of the indicators I studied was created by the anonymous author of the blog Philosophical Economics. It is now as bearish as it was right before the 2008 financial crisis, projecting an inflation-adjusted S&P 500 total return of just 0.8 percentage point above inflation. Ten-year Treasurys can promise you that return with far less risk.

Suffice it to say there is a wealth of evidence pointing to the conclusion that stock returns over the next decade or so are likely to be very weak, as they were for the decade following the last time (late-1990s tech bubble) valuations were in today’s territory.

So does that mean we should bail out of the stock market? Not necessarily. We’ll cover what SMI thinks is a better approach in our September newsletter.