The lack of true downside protection has long been a concern for those using SMI’s Fund Upgrading strategy. Fortunately, recent developments in the study of momentum have laid the foundation for a new defensive protocol that provides a “safety net” for Upgrading.

This new 2.0 protocol gives us confidence that Upgrading will be up to the task of defending member portfolios during the next bear market.

[Editor’s Note: SMI’s Stock Upgrading strategy was modified in January 2021 to allow it greater ability to align with the dominant growth/value market trends (see Fund Upgrading Gets Upgraded: Adapting to an Ever-Changing Market Landscape). The article below explains the defensive protocol concepts built into Upgrading. These concepts remain the same within the updated version of the strategy, but their implementation varies somewhat from what is described here as the structure of Upgrading’s holdings was modified with that 2021 update.]

SMI’s Fund Upgrading strategy, which uses a concept known as “performance momentum” to make investment recommendations, has been part of the SMI newsletter in some form or fashion from its earliest days in 1990. By the late 1990s, Upgrading had settled into roughly the form used today. In the years since, the only significant change to Upgrading, at least on the stock-fund side, has been the switch from recommending four funds in each risk category to only three (in April 2015).

In the meantime, academic and industry research on the momentum principles on which Upgrading is based has been anything but idle. In fact, momentum has been one of the most heavily researched investing topics for several decades now. This is largely due to its status as “the premier market anomaly.” Momentum is an easily observable exception to the conventional wisdom that stock market prices are set by such an efficient process that it’s difficult — if not impossible — for investors to outperform the market over time.

That “premier anomaly” label was attached by none other than Eugene Fama, who won a Nobel prize for his work on the Efficient Market Hypothesis. As the name implies, his life’s work has been explaining why factors such as momentum shouldn’t work. Yet just this past year, Fama conceded, “Momentum is a big embarrassment for market efficiency.”

Because momentum has been such a persistent thumb in the eye of the indexing/efficient markets community, researchers have undertaken many studies of momentum. Actually, the earliest such research dates back nearly a century, but up until about a decade ago, most of the research focused on variations of relative momentum — i.e., how an investment has performed relative to others. This relative-momentum analysis is the type SMI has always used in SMI’s Upgrading strategy, and is reflected in our monthly Fund Performance Rankings report.

While the research studies on relative momentum affirmed its robustness and effectiveness, it wasn’t until somewhat recently that a new momentum idea emerged. This was the study of how an investment performed, not against other investments, but against its own past. This second type of momentum is referred to as absolute momentum. Relative momentum asks the question: “In recent months, how has this investment performed compared to others?” But this newer momentum measure asks the question: “In recent months, how has the investment performed in an absolute sense, looking at its own history, ignoring what others have done?”

Multiple studies have confirmed that asking this question can lead to profitable investing choices going forward, but credit for popularizing absolute momentum belongs to Gary Antonacci, who detailed it extensively in his award-winning book, Dual Momentum Investing. In addition to compiling the results of all the research done on absolute momentum, much of it his own, Antonacci also took the crucial step of marrying the two forms of momentum — relative and absolute — into a simple investment strategy that readers of his book could apply easily. The backtested results of this approach were surprisingly good, despite the approach being extremely simple.

In a nutshell, while Antonacci demonstrated what SMI Upgraders have long known, that relative momentum can be a powerful return enhancer, he added a critical new dimension as well: showing how applying absolute momentum criteria could limit downside loss significantly.

Improving on SMI’s “Bear Alert”

Since Antonacci’s book came out in 2014, SMI has been working on how we might apply this new information to our Stock Upgrading strategy. This research has been through many iterations in our quest to strike the best balance of simplicity and effectiveness. The result of this research is our new “Upgrading 2.0” being introduced this month.

To set the stage for this new Upgrading approach, it’s helpful first to back up and look at how SMI has addressed the issue of downside risk within Upgrading in the past. The Upgrading strategy has some risk mitigation built into it through the normal process of rotating from aggressive funds into more conservative ones as conditions change. While helpful, this alone is unable to provide sufficient protection to an investor during deep bear markets.

In an attempt to bolster our ability to handle downside risk and bear markets, SMI created a “Bear Alert” indicator following the 2000-2002 bear market. In the years since, the guidelines regarding how to best implement the Bear Alert within Stock Upgrading have been modified a few times. While the Bear Alert has been helpful (certainly during the 2008 financial crisis), it has raised questions among many SMI members as to how best to use it. Additionally, the Alert yielded some false signals along the way (2010 and 2011).

Upgrading 2.0 improves on the quality and accuracy of the Bear Alert signals, while also bringing that risk management function into the Upgrading strategy itself. This is a key point in terms of ease of use: Upgraders will no longer need to monitor a second signal, external to Upgrading, and decide how (or if) to apply it to their holdings. With Upgrading 2.0, SMI members will be able to simply follow the monthly fund replacement signals as they always have; however, they’ll now have a robust risk-management system running in the background (as part of the Upgrading strategy) looking for signs of trouble.

Applying absolute momentum to Stock Upgrading

This means that when the defensive aspects of absolute momentum kick in for Stock Upgrading, the actions we’ll take will function completely within the context of normal Upgrading. As before, you’ll check to see which funds, if any, are to be sold, but instead of switching immediately into another stock fund, the proceeds from any sold funds will be held in cash.

Behind the scenes, SMI will be running all the normal relative momentum calculations we always have, identifying funds to buy and sell based on their recent performance compared to others in their risk category. But now we’ll also be running some new processes that tell us when to start looking at the absolute momentum of each fund in our universe. At a certain point in a weakening market, these absolute momentum screens will tell us we’re better off not owning certain stock funds. As that happens, the recommended-fund “slots” increasingly will suggest holding money in cash instead.

This however, is the rare exception, not the rule. In fact, we’ve purposely designed Upgrading 2.0 to kick in only when the risk of significant declines has measurably increased. As long-term readers would expect, there’s no predictive element to this — it requires certain signals that show market deterioration is already under way in order for these new defensive protocols to trigger. You’ll never see cash recommendations within Upgrading when the market is near all-time highs, as it is today. Only when the market has begun to fall and passes certain “tripwires” will the protocol kick in and open the door to absolute momentum to start gradually shifting some of our Upgrading holdings to cash.

Break glass only in emergency

This is an important point to understand: Upgrading 2.0 is designed to turn on infrequently, during only the most significant bear markets. We have built it using criteria and settings that shouldn’t prompt defensive actions during “run of the mill” market corrections.

The pair of market corrections in late 2015 and early 2016 provide a helpful example. To review that period, the market fell roughly -12% on two separate occasions within a seven-month period. The popular stock-market indexes, such as the S&P 500, first lost -12% in August of 2015. While those large-company-dominated indexes gained back all of those losses by October, small-company stocks rebounded only mildly before plummeting again in January 2016. For the large-company dominated indexes, the events looked like a pair of -12% corrections. But those invested in small-company stocks experienced a mild bear market with losses exceeding -20%.

Our testing of Upgrading 2.0 showed it would have ignored the August 2015 episode entirely, and started taking only mild defensive steps when the second leg of the downturn was reaching its climax in early 2016. In that 2016 instance, each of Stock Upgrading’s risk categories had one fund turn to cash in February, and a second turn in March. By April, all of Upgrading’s slots were back-invested in normal stock funds.

In hindsight, it would have been ideal for our defensive measures to have not turned on at all in this case. The correction ended in mid-February, so our defensive measures ultimately caused Upgrading 2.0’s backtested 2016 performance to decline slightly. But given the depth of the losses in small-company stocks at that time, it was appropriate to start taking measured defensive steps.

Perhaps most importantly, outside of 2000-2002 and 2008-2009, the two major bear market periods when we surely would have wanted defensive measures to activate, this two month period in 2016 was the only “false signal” or whipsaw in the 20 years of testing we did. While this is obviously no guarantee against whipsaws in the future, it’s an encouraging sign.

The idea of not trying to protect against 10%-15% declines may seem strange to newer readers. Wouldn’t we want to protect against any downturns? It’s important to understand there is always a tradeoff involved in any attempt to reduce market risk. Is the potential benefit greater than the potential cost? Protecting against market risk requires taking some sort of defensive measures. If the market moves higher rather than lower once those defensive measures have been put in place, performance will suffer (as it would have in early 2016 had Upgrading 2.0 been active).

Stock-market declines of 10%-15% have been common historically, occurring every one to two years on average. We want our system to avoid being triggered during shallow corrections. Yet we want those defensive measures to still kick in early enough to protect us from the bulk of the losses suffered during deep bear markets.

Add all of this up and we’re talking about a defensive system designed to turn on only during the “big” bear markets while ignoring everything else. Said differently, Upgrading 2.0 is designed to look exactly like Upgrading has always looked — except during those roughly once-a-decade bear markets that take the markets down for the count.

Upgrading 2.0 backtesting results

How does the new Upgrading 2.0 meet these goals? Quite effectively, if our backtesting of the past 20 years is representative of what we can expect in the future.

Obviously, we’d love to have more history to test on, but we have good Upgrading fund data to work with only going back to around 1998 — prior to that, our fund selection process was different enough that the older data isn’t useful. However, the lack of fund data is somewhat irrelevant because there weren’t any market events between SMI’s inception in 1990 and the start of our “good data” in 1998 that would have triggered the new 2.0 protocol.

As it is, our testing period includes the two big bear markets: the 2000-2002 dot-com crash and the 2007-2009 financial crisis, as well as the numerous milder “panics” we’ve had along the way, which include 1998, 2010, 2011, and the aforementioned 2015-2016 twin corrections.

Overall, the results have been fantastic. Here’s why: As we’ve explained before, there’s a “cruel math” attached to investment losses. If a portfolio loses 25%, it doesn’t require merely a 25% gain to get back even — it requires a 33.3% gain. A 50% loss, such as the indexes have experienced during the past two big bear markets, doesn’t require a gain of 50% to get back to breakeven — it requires a 100% gain from that low to recover.

Understanding that, one can see how important minimizing losses can be for long-term performance. The addition of absolute momentum in creating Upgrading 2.0 works wonders along those lines, despite not being “turned on” very often over the 20-year test period.

Table 1 above shows the theoretical results of the full 20-year test period. It shows how “actual Upgrading” — what SMI readers experienced, on average, using normal Upgrading — handily beat the market with a performance difference of +9.0% vs. +7.4% annually over those two decades. But adding the absolute momentum process of Upgrading 2.0 sent that annual return soaring to +14.1% in our backtesting!

(Full disclosure: Our ability to reproduce what the exact results would have been in this backtest isn’t as precise as with other “purely mechanical” testing we’ve done, such as with DAA. That’s due to the small degree of subjective evaluation we apply when choosing from among two or three “finalists” when selecting new Upgrading recommendations. There is no doubt that the 2.0 protocols add a significant degree of capital protection to Upgrading. The exact degree of protection can’t be known, but it should be close to that illustrated in the table above, perhaps plus or minus a percent or two.)

The percentage differences in Table 1 may be better appreciated in terms of their dollar impact on a portfolio. A portfolio of $100,000 invested 20 years ago at the market’s rate of return would have grown to $418,000. A “regular” Stock Upgrading portfolio would have done considerably better, growing to $564,000. But an Upgrading 2.0 portfolio? A shocking $1.4 million — more than double the market’s total gain.

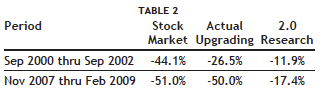

Table 2 shows how it happened. Upgrading 2.0’s defensive protocol, built on the principle of absolute momentum, put a safety net under Upgrading’s performance during the two big bear markets of the past 20 years. In 2000-2002, regular Upgrading did a pretty good job of limiting losses. While the market was down -44.1% between September 2000-September 2002, regular Upgrading lost -26.5%. But Upgrading 2.0 would have done substantially better, limiting that bear market’s loss to only -11.9%.

The more recent financial-crisis bear market was even more stark, given that its reach extended to every corner of the market, leaving no risk categories where regular Upgrading could find a safe haven. The market lost -51.0% between November 2007-February 2009, and regular Upgrading was only slightly better at -50.0%. But Upgrading 2.0 limited that loss dramatically, falling just -17.4%. Remembering our “cruel math” of investing losses, it’s easy to see how such a dramatic limiting of bear-market losses can lead to incredible improvement in the long-term strategy performance record.

Effortless implementation

Earlier, we referenced Gary Antonacci’s book, which contained a simple system for combining relative and absolute momentum into a workable long-term strategy. That approach was appropriate for the wide audience that would read his book and try to implement his system on their own.

Our initial research focused on similarly simple approaches, but what we discovered was that in our effort to keep the system simple, we were leaving a lot of potential profit on the table. In addition, the approaches we looked at initially had the significant issue of either creating too many “false” signals, which caused whipsaws (exits followed by rapid re-entry signals), or being too “dull” and losing too much during big bear markets.

As a result, we ended up studying refinements that would help us fine-tune the absolute momentum outcomes a bit. The result is a combination of technical indicators that alert us when market risk has risen to a degree sufficient that we should begin watching for the absolute momentum signals at the individual fund level.

(If reading that last paragraph felt a little confusing, you’ll understand why we won’t be making all the details of the new Upgrading 2.0 system public. Not only would it be confusing to less-advanced readers, it simply isn’t necessary to bog readers down with the indicators behind what has become a more complicated system. The strategy is a simple one on the surface, and can be implemented by just following the same steps Upgraders are accustomed to in running their portfolios.)

Here is all you really need to know: When the defensive protocol kicks in and absolute momentum becomes a factor in our Upgrading process, you’ll see individual fund “slots” on the Fund Upgrading Recommendations page turn to “Cash.” If that happens to a fund you own, simply sell it as usual. But rather than immediately replace it with another stock fund, let the proceeds of that sale temporarily sit in cash in your account until, eventually, a new stock fund is recommended.

Phased-in exit signals

Note that this “move to cash” won’t happen to all funds at once. In fact, one of the aspects we tested and eventually built into the system was the concept of a “phased-in” application of these signals. All this means is you won’t ever see more than one recommended fund per risk category go to cash in a single month.

This phased-in approach may cost us slightly during the occasional true bear market, as it can take us as long as three months to completely exit a particular risk category. But overall performance using this system during the big bear markets was so outstanding (see Table 2) that we felt it was well worth the tradeoff to limit our exposure to cash early on in market declines. The research suggests that doing so likely will protect us from moving too quickly to cash during the ultimately short-lived corrections (such as 2016) which occur more frequently.

While this means most Upgraders won’t have to sell all their funds and go to cash all at once, it’s worth noting that the signals can be interpreted in different ways depending on your risk-tolerance. A more conservative member may opt to move his or her holdings in a particular risk category to cash as soon as any of the recommended funds in that category switch over to cash. In contrast, another member may wait until all three holdings for a given category go to cash. By waiting longer, the chances of being whipsawed are decreased.

A natural downside of not spelling out all the working parts of the new system is that those in 401(k) and other plans won’t know precisely when these various triggers are firing behind the scenes. But it will be easy to tell when it’s time to take action by simply watching what’s happening on the Upgrading Recommendations page. Again, the conservative-aggressive spectrum may alter your implementation by a month or two, but overall, any investor tuning in to the official Upgrading fund recommendations will know when the system is indicating it’s time to take defensive cover.

Phased-in re-entry signals

Our criteria for re-engaging with the market is phased as well. Historically, we know that when the market has lost between -10% and -15%, it will have quite a bit further to fall if we’re entering a major bear market. So if our system moves us to cash at those relatively modest loss levels, it’s designed to require a strong contrary signal to get us to reverse our defensive positions and move back into stocks.

The criteria we’ve established, however, will make the decision to re-enter easier as bear-market losses intensify. As long as a selloff remains mild, the hurdle for once again buying stocks is set relatively high, but as the market falls below various loss thresholds, the hurdle is lowered. That means we’re more likely to go back into stocks when the market is down -35% than we are when it’s down -20%. As overall market losses deepen, our focus shifts to making sure we get back in for what is typically a sharp bounce off the ultimate bear-market low.

Given that bear markets tend to be multi-year events, we’ll have plenty of time to write more about the re-entry side of this system when we finally do go through another bear market.

Conclusion

The new Upgrading process we’re unveiling this month has two huge potential impacts:

The performance of Upgrading should be drastically improved by avoiding most of the worst losses (see Table 1 above).

It should have a huge impact on how willing you are to stay invested during late-stage bull markets. Those late stages tend to provide some of the strongest returns to investors. Being able to harvest late-cycle gains, while still avoiding the bulk of any subsequent bear markets, is a game-changer for Upgraders.

Importantly, there are no extra signals for you to watch for, or even anything complicated to do on the rare occasions when our defensive protocol kicks in. When it does, you’ll simply sell as normal, then sit in cash until regular Upgrading resumes with new stock-fund recommendations. Just follow the monthly Upgrading instructions as you always have and you’ll be all set. It is as easy as that.