Many investors have watched in astonishment as the market has roared back from its late March, Iran War lows. While gains have been impressive across the board, they’ve been particularly stunning in the tech-heavy Nasdaq index (up +28% since the March 30 low). And a primary driver of tech returns has been a wild ascent in semiconductor stocks. XSD, the semiconductor ETF recently bought within Sector Rotation, has gained +106% since March 30 (all figures through May 26).

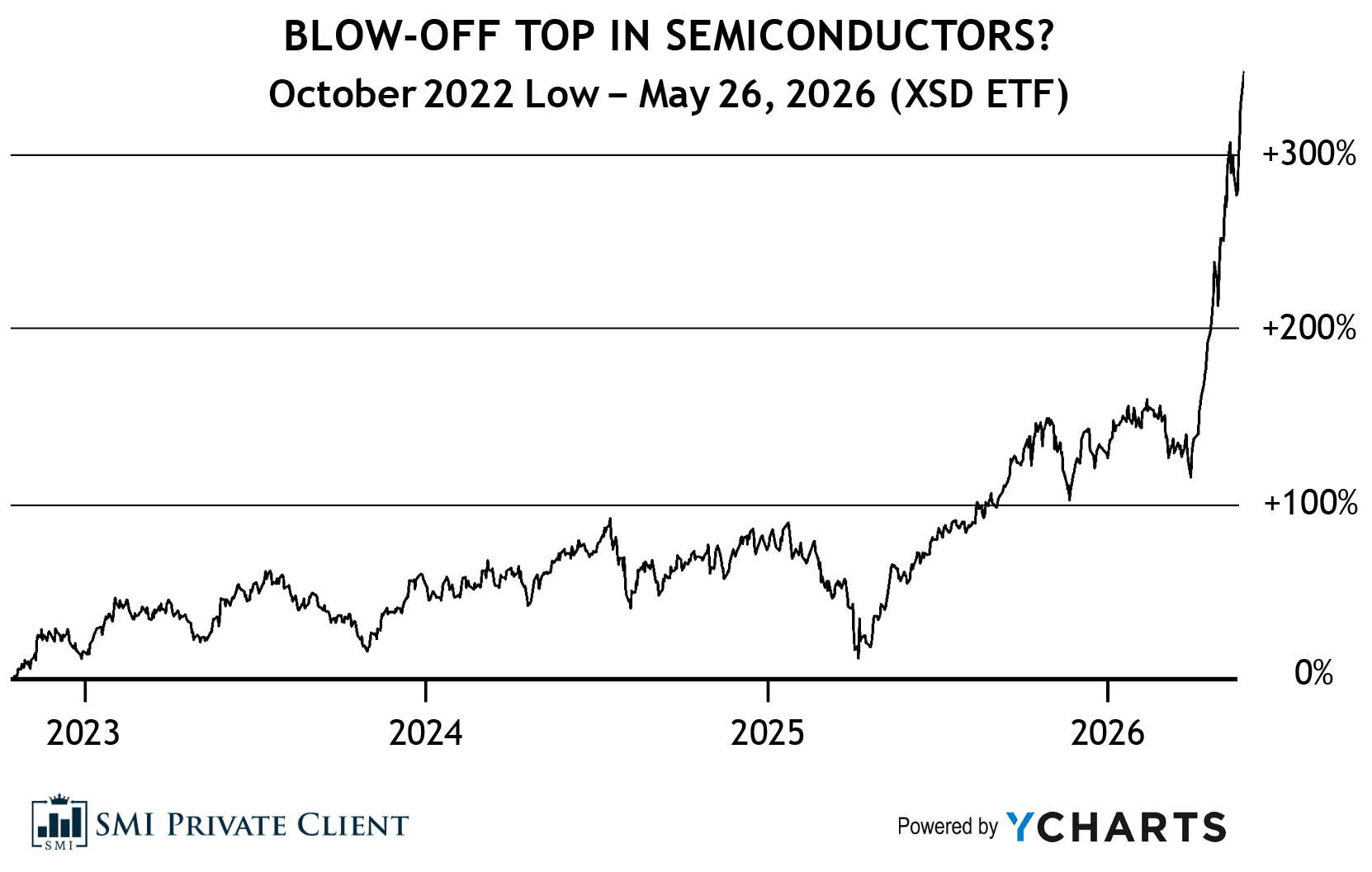

A quick look at the chart below shows the incredible gains of semiconductors (XSD) since the October 2022 lows. Since that bear market bottomed ~3½ years ago, semiconductors are up +346% (+51% annualized) while tech stocks (Nasdaq index) have gained +165% (+31% annualized).

Perhaps even more concerning is the shape of the semiconductor stock chart. That line turning straight up recently looks, at least to some eyes, ominously like a “blow off top.”

Is it a bubble?

While semis and tech stocks have been on quite a run, it’s worth stepping back to evaluate this move in a broader context. When we do that, the bubble picture isn’t so clear. The May Private Client video update made the point that the stock market is a forward-looking discounting mechanism. That simply means investors care a lot more about what a business is going to earn in the future than what it is earning today. In theory, a stock price is just the present value of a company’s future business expectations. So if those expectations improve notably, the current stock price should increase in turn.

That’s exactly what we’ve seen during the recent quarterly earnings season. Kevin Muir, who writes The MacroTourist Substack, points out that this quarter’s S&P 500 earnings were the 8th-best quarterly earnings in the past 22 years. But they jump off the page for a different reason: this quarter was the only quarter among the Top 10 that didn’t follow a significant downturn first. As Muir puts it, “The current earnings period is unique because it is the only non-post-recessionary acceleration of this magnitude.”

Connecting these dots, it appears that one of the main reasons large U.S. companies have seen their earnings inflect higher is they are starting to see the impact of AI flow through to their bottom-lines. Getting the same (or in many cases, more/better) work out of the same number (or fewer) employees is a recipe for higher corporate profits. That’s what companies delivered this quarter. And, crucially, AI’s expanding impact guided estimates substantially higher for the next few quarters as well.

In other words, this isn’t a one-time fluke. It appears to be the start of a new higher earnings trend, and stocks have broadly repriced higher as a result.

Working backward from there, the tech companies facilitating this step-change higher in corporate profitability have seen their stock prices increase faster, and the semiconductor companies at the heart of the AI story have gone up the most. This makes sense as questions about whether corporate America would actually be able to monetize the promise of AI are being answered “yes” in real time.

Said differently, the odds that the AI story is “smoke and mirrors” that will never fulfill the hype are declining. Investors are rapidly changing their assessments as they realize the AI companies are still short of the needed computing power to satisfy the voracious appetite of corporate America for more AI, as company profits begin to be seriously boosted by these AI tools.

SMI’s approach to bubbles (or aging bull markets)

The point of this article isn’t to try to convince you one way or the other regarding whether AI/semiconductor/tech stocks are in a bubble. Rather, it’s to assess what an investor should do even if this turns out to be one.

One lesson from history is that trying to predict when a bubble (or simply an aging bull market) will end doesn’t work. So what can investors do instead? Here’s SMI’s approach to dealing with a bubble (or extended bull market):

Stay invested.

This assumes you’re using an appropriate blend of SMI’s strategies, some of which have defensive properties that we believe will help reduce (not eliminate) the impact of future bear markets. Note also that a simple way to reduce risk during rapidly rising markets is to rebalance your portfolio more frequently, which redeploys money from rapidly rising holdings into less bubbly assets.Have reasonable expectations.

This applies both to your overall portfolio and to each individual component. We know that by continuing to invest, specifically in the tech and semiconductor themes, we’re likely to give back a portion of our late gains when the market either moves on from the tech/AI theme, or worse, finally shifts from bull market to bear. Hopefully, you’ve made peace with that idea so it won’t be upsetting when it eventually occurs.If the bull market continues and it’s just a theme change we have to eventually deal with, the normal processes within strategies like Sector Rotation and Stock Upgrading will gradually pivot our portfolios from the old themes to the new ones. If it’s a more dramatic ending that results in a full-blown bear market, remember that the defensive properties of the SMI strategies are intentionally designed to kick in slowly, ideally triggering only occasionally, during particularly damaging conditions.

There’s always a trade-off with defensive efforts: Either the protocols trigger quickly, causing us to endure numerous false alarms that cost money and frustrate everyone along the way, or they trigger slowly and infrequently, which requires us to absorb some degree of pain at the end of a bull market cycle. This happens as our fully invested portfolios work their way down from the prior highs to the levels where the defensive protocols kick in and start getting us out of stocks.

Regarding the individual strategies, understand what each is expected to do. Upgrading, and especially Sector Rotation, are supposed to perform great in the current environment (and they have been!). Dynamic Asset Allocation isn’t (although gold has helped it be a strong performer over the past couple of years). DAA is supposed to do okay during bull markets, then be great in the opposite environment — bear markets. Over full market cycles, DAA’s performance will hopefully exceed the overall market. But it typically gets there by outperforming during bear markets, while lagging toward the end of bulls.

Play good defense.

While Sector Rotation and Stock Upgrading are exposed to the initial stage of market declines, DAA plays a vital role in incrementally playing defense within a portfolio. Psychologically, it’s tough to make significant changes to one’s stock allocation all at once. That’s one reason why traditional market-timing approaches don’t work for most people: apart from it being extremely difficult to figure out accurate signals, those trades are emotionally brutal to execute.Contrast that with DAA, which always has some defensive positioning in place via its SMI 3Fourteen REAL Asset Allocation ETF (RAA) holding, and never has more than two-thirds of its remaining holdings in stocks at any given time.

Who has the easier emotional path from here, should the market begin to decline substantially? The DAA investor who will see their defensive holdings increase each month within RAA, and eventually will take the incremental step of eliminating a one-sixth position in U.S. stocks at a pre-established interval? Or an investor who has been heavily invested in stocks for years and has to figure out when and how much to trim that heavy stock allocation?

The existence of defensive protocols within Stock Upgrading since 2018 is another reason we can confidently keep Upgrading money invested right through the end of a bull market, while still expecting some reduction to the losses inflicted by an ensuing bear market. That’s important, because large gains often come in right before bull markets end (thus the concerns about the semiconductor chart).

SMI members using the type of multi-strategy approach we frequently discuss likely have a good portion of their portfolios covered by some type of defensive protocol. For example, a 50/40/10 portfolio would have 90% of the portfolio covered by either DAA’s or Upgrading’s defensive measures. Those actions are built right into the strategies themselves, so members don’t have to do anything special. They just keep following the monthly instructions as they normally would. This should help tremendously with actually executing any defensive steps, because those steps won’t feel particularly unusual or like they’re coming from outside the normal system.

Summary

It’s rare for markets to correct as significantly as they did in April 2025 and March 2026, then rebound as strongly as they have recently, only to then fall into a deep bear market. Never say never, but this dynamic, coupled with the resilient economy and recent inflection higher in realized and anticipated corporate earnings, suggests that this bull could run quite a bit further before it tires. That said, it’s still useful to ask the tough “what if” questions should that turn out not to be the case.

The bottom line is that SMI’s strategies allow us to stay invested through what can be surprisingly long “late” bull market periods — harvesting the big gains that often come in toward the end — while still reducing our downside risk when bear markets eventually hit. Long-term, we think this approach will lead to better results than trying to anticipate bear markets and reduce stock exposure preemptively. Mentally and emotionally, it’s much easier to follow the same strategies long-term — through bull markets, bear markets, and especially those confusing periods when it’s unclear which animal is in charge!