Before 2020, I'd never been a gold bug.

Most investors are, to some degree, a product of the market environment they "come of age" in. I'm no exception. I got my finance degree in the first half of the 1990s, started investing personally in the second half of that decade, and started full-time in the investing business with SMI in January 2000.

In other words, my early personal and professional investing experiences were heavily colored by the tech bubble and crash, followed by the Global Financial Crisis (GFC) a handful of years later.

Applying that timeline to gold...yuck. Gold had peaked in 1980, long before I was tuned in, and had spent 20 years in an ugly bear market. The first decade I was really tuned into investing (the 1990s), gold was a black hole. Nobody cared about gold by the end of the 90s. Legends like Warren Buffett were saying disparaging things like this about gold around that time (1998):

"(It) gets dug out of the ground in Africa or someplace. Then we melt it down, dig another hole, bury it again and pay people to stand around guarding it. It has no utility. Anyone watching from Mars would be scratching their head."

I figured he should know, being a legend and all.

The final confirmation of my total disinterest in gold came in 2002 when Austin and I worked on the research that turned into SMI's Sector Rotation strategy. We ultimately had to throw the Precious Metals mining funds out of the SR fund universe because even within that group of wild swingers, the PM funds were so volatile they messed everything up! So, to my 2002 eyes, not only had gold been a terrible performer for the prior two decades, but it was also a volatile pain in the neck.

My radicalization began in 2012...

Fast-forward a decade to 2012, when Austin and I once again engaged in research on a new strategy (which would ultimately become Dynamic Asset Allocation, or DAA). Driving this research was the realization that bonds were unlikely to provide investors with the type of returns in the decades ahead that they had in the three decades prior.

The reason was simple math: Bonds had used up most of the huge tail-wind that falling interest rates had provided since 1982. It had been a monster bond bull market, but by 2012, the Fed Funds rate had spent 7.5 of the prior 11 years below 2%. The GFC in 2008 had seen rates smashed to near-zero, plus Quantitative Easing added as an extra kicker.

You can read more about the origin story of DAA in the sidebar links. But a foundational building block of the strategy was Harry Browne's Permanent Portfolio idea, which allocates 25% of a portfolio permanently to each of Stocks, Bonds, Gold, and Cash.

25% to Gold? Permanently? Maybe that had made sense when Browne came up with the idea in the 1970s, but we were enlightened 21st-century investors!

As most SMI readers know, DAA avoided large permanent allocations by utilizing momentum to guide our investing between these asset classes. But it was the first time I had wrestled with the idea of an investor putting a significant slug of a portfolio in gold.

Crucially, one of the biggest positives DAA provided was it significantly reduced SMI's static bond allocations. While DAA didn't perform as well as we hoped during its first decade, it looks a lot better when one realizes that much of the money it absorbed came from what had previously been investor bond allocations.

For example, an investor who allocated 90% to Upgrading and 10% to Sector Rotation before DAA, while splitting their Upgrading 60/40 between stocks and bonds, would have had 36% of the money in a static bond allocation. If that person transitioned to a 50/40/10 portfolio — 50% DAA, 40% Upgrading with the same stock/bond split, and 10% SR — the static bond allocation would have dropped from 36% to 16%. Of course, DAA owns bonds sometimes, which temporarily boosts the overall portfolio bond exposure. But when bonds are breaking bad, as they have the past few years, SMI's exposure to bonds is much lower than it used to be.

...and took another leap forward in 2020

The massive stimulus response to the COVID crisis in 2020 was an eye-opener for many people, myself included. I penned a cover article on gold in the summer of 2020, explaining the potentially inflationary path forward and how gold might serve as an anchor against a world of fiat-currency debasement.

Given my concern about future bond returns in 2012, when the 10-year Treasury yield began and finished the year around 2.0%, imagine how I felt seeing the 10-year Treasury yield at 0.52% in August 2020! From there, it was hard to imagine bonds had much upside. And they haven't, as they've been stuck in a bear market over the four years since.

The question isn't gold vs. stocks. It's gold vs. bonds.

It's hard to overstate how out-of-consensus the idea of significant gold allocations is with professionals (institutions and investment advisors). This chart does a good job of framing it.

1/ What's the ideal gold allocation?

— Ronnie Stoeferle (@RonStoeferle) August 13, 2024

A recent ARC survey (https://t.co/VLHi005ri5) highlights that 75% of managers surveyed have minimal to no gold exposure, with none exceeding 10%.

These results echo a Bank of America study, showing that 71% of US advisors allocate less… pic.twitter.com/mPRqJkc5JA

Advisors have no problem putting 40%, 50%, 60% or more of their client money in bonds. But gold? It may as well still be 2000, with bonds two decades into a raging bull market and gold two decades into its bear market slumber.

This is an excellent time to remind us all of the crucial first lesson mentioned in the September SMI article, Right – and Wrong – Lessons to Draw From Gold vs. Stocks:

Starting (and ending) points matter...a lot.

The same is true when comparing gold and bonds. If we're not careful, we can cherry-pick starting points that look good for one class and bad for the other.

The natural starting point for comparing gold and bonds — at least to my mind — is when the Fed started its "low interest rates forever" campaign. An argument can be made that began in December 2001, when the Fed dropped the Fed Funds rate below 2%. The Fed Funds rate would stay below 2% for all but about 4.5 of the next 20 years before the recent hiking cycle began in 2022.

For our purposes, what we really want to see is how gold and bonds each perform as a complement to stocks within a blended portfolio. Because as much as gold enthusiasts might want to make this about raw performance, a considerable part of the appeal of bonds is that they have done a good job of dampening portfolio volatility over the past 25-30 years, mainly by being inversely correlated to stocks (i.e., bonds have tended to go up when stocks have gone down).

Here's a chart comparing a 60% Stock / 40% Gold portfolio with a 60%/ 40% Bond portfolio, starting in December 2001 when rates first fell below 2%:

Surprising, isn't it?

However, skeptics will rightfully point out that the December 2001 starting date happens to correspond pretty closely to the end of the gold bear market.

I'm not willing to dismiss the above comparison, as it's worth considering whether ultra-low interest rates were at least partially responsible for ending the 1980-2000 gold bear market and sending gold higher over the decades since. After all, gold competes with interest-paying alternatives and lower interest rates are a widely accepted factor in producing higher gold prices.

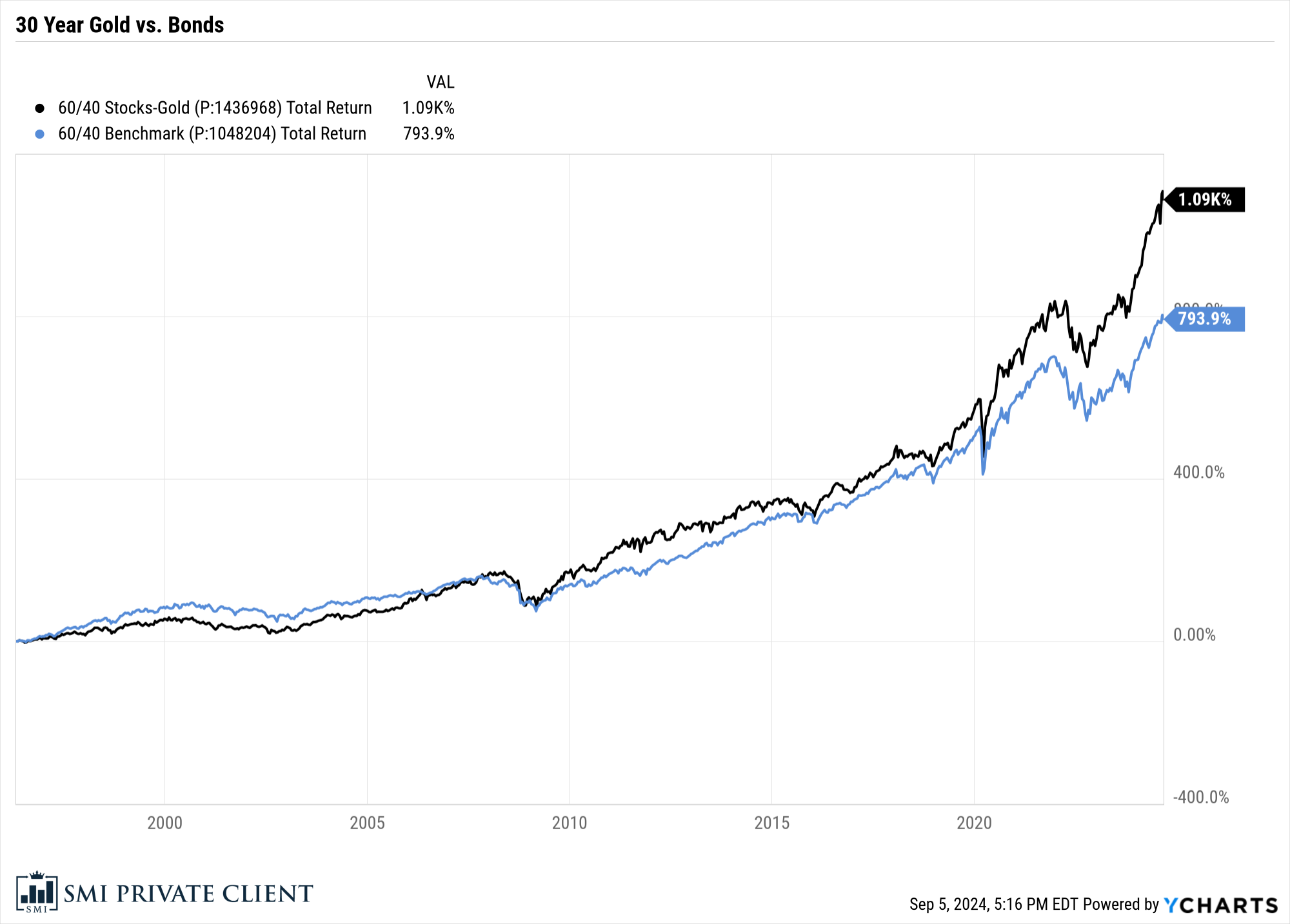

But to avoid any appearance of stacking the deck in gold's favor, let's go back 30 years, to September 1994. The bond bull market was in full swing, and the gold bear market would hold on for another six years. Here's that comparison:

Gold still has the better of it overall, though the comparison is much closer. The chart clearly shows bonds outperforming through the end of the 1990s, then gold gaining the upper hand and pulling away post-GFC in 2008.

Important takeaways

Both lines (in both charts) include 60% allocations to stocks, so the effect of stock market variation is nullified. The difference between the two lines in each chart is the impact of gold vs. bonds as the 40% portfolio diversifier.

Returns aren't everything. Both charts show that gold (the black line) is more volatile than bonds. We see gold pull away during good times and then fall back toward the 60/40 bond (blue) line again and again.

This portfolio smoothing is a substantial reason pros have been slow to switch from bonds to gold — it's great to always have something in the portfolio that is doing well. Having stocks and gold both falling at the same time is an advisor's nightmare, yet that's what typically happens at the start of each significant market sell-off.

Nobody is suggesting investors replace all their bonds with gold. The point of this article is simply to introduce the idea that perhaps a little more gold and little less bonds might be worth considering.

SMI investors already do this if they allocate significant assets to our DAA strategy.

To close, it's worth pointing out that gold is up about +30% so far in 2024, while bonds have had a rough run the past few years. So even if an investor was considering shifting some bond money to gold, it might be worth waiting for a more opportune time to make that shift. Market panics have a way of coming around every so often, and when they do, gold often drops sharply along with stocks (as investors sell what they can, with gold always being liquid). Meanwhile, bonds often reflexively spike higher in price during panics. That would be an ideal time to sell a little bond exposure at a temporary high point while adding gold exposure near a temporary low point.