As detailed in our October issue, money-market mutual funds have fallen on hard times. That’s a shame.

Here’s a quick primer on money funds from The Sound Mind Investing Handbook:

[You can lend your money to] "big time" players who...typically will pay you more interest than your bank will. These organizations include the federal government, big corporations, and even other banks. However, to do business with them readily, you need a go-between. That’s where a special type of mutual fund comes in, one that specializes strictly in the short-term lending of money in the financial markets. Hence, its name: money-market fund.

The word "typically" above is important. During times of extremely low interest rates, MMFs may pay less than bank savings accounts. We saw that during the 2008 financial crisis and for years following. Money funds finally began to recover a bit of luster in 2018, and for most of last year were yielding better than 2%.

Unfortunately, the return to almost-normal was short-lived. MMF rates began falling in the latter part of 2019 and then fell drastically when COVID hit. In January, MMFs were paying an average of 1.30%. By May, the average had fallen to 0.10%. MMF rates have fallen even more since then and now average just 0.04%.

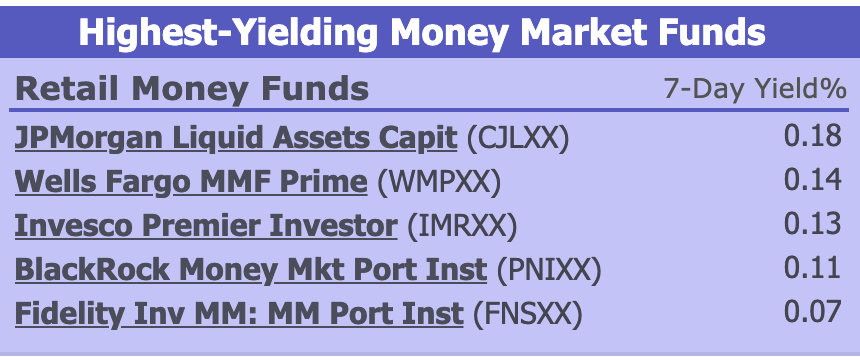

Here are the best current MMF yields, courtesy of Crane Data. It’s not a pretty picture.

Note: A 7-day yield reflects what an investor would earn over one year at the current rate.

Better options

So where do you turn for a better return on your savings? Matt related his story last week about moving his savings from an MMF to Capital One, an online bank currently paying 0.50% on its savings accounts (down from 0.65% last month). As Matt noted, Capital One makes it easy to set up and track multiple savings accounts (which is a helpful feature), but other online banks are paying better rates.

Here are seven other bank-savings options (all FDIC-insured):

Bank | Min. to open account | Current rate | URL |

SmartyPig | $0 | 1.10%* | www.smartypig.com |

First Foundation Bank | $1,000 | 1.00% | www.firstfoundationinc.com/personal-banking/bank/online-savings |

Salem Five Direct | $100 | 0.80% | www.salemfivedirect.com |

Vio Bank | $100 | 0.76% | www.viobank.com |

Live Oak Bank | $0 | 0.70% | www.liveoakbank.com/personal-banking/personal-savings/ |

Discover Bank | $0 | 0.60% | www.discover.com/online-banking/ |

Ally Bank** | $0 | 0.60% | www.ally.com/bank/online-savings-account/ |

*SmartyPig (yes, that’s an actual bank name) is paying 1.10% on amounts up to $2,500 and then 1.00% on amounts up to $10,000. Amounts from $10,000 to $50,000 earn 0.80%. SmartyPig is part of the well-known education lender Sallie Mae.

**Like Capital One, Ally Bank allows users to set up multiple savings accounts (Ally calls them "buckets").

Is it worth it?

Be aware that moving your savings from one account to another to earn a higher rate may not make that much of a difference. For example, a $10,000 account earning 0.50% will pay $50 a year. That same amount of money at 0.70% will pay $70 a year.

But if you’re currently earning 0.05% in a money-market fund (i.e., $5 a year on $10,000) or perhaps 0.01% at your bank (only $1 year on $10,000), moving your money to a savings account that’s earning, say, 0.70% would seem to be worth it. Of course, there is no guarantee that a bank paying 0.70% today will still be paying that rate a few weeks from now.

How about you? Have you moved your savings from one account to another in search of better yields?