Matt has written several times (most recently here) about the Retirement Confidence Survey, issued annually by the Employee Benefit Research Institute (EBRI). The RCS consistently polls two categories of respondents: current workers (1,255 this year) and current retirees (1,266).

While preparing an article for SMI's upcoming September issue, I reviewed this year's survey findings and discovered a few encouraging data points we haven't previously reported.

Better than expected

For example, despite the run-up inflation, most retirees are not feeling financially squeezed. Further, about a third say their retirement lifestyle is better than expected.

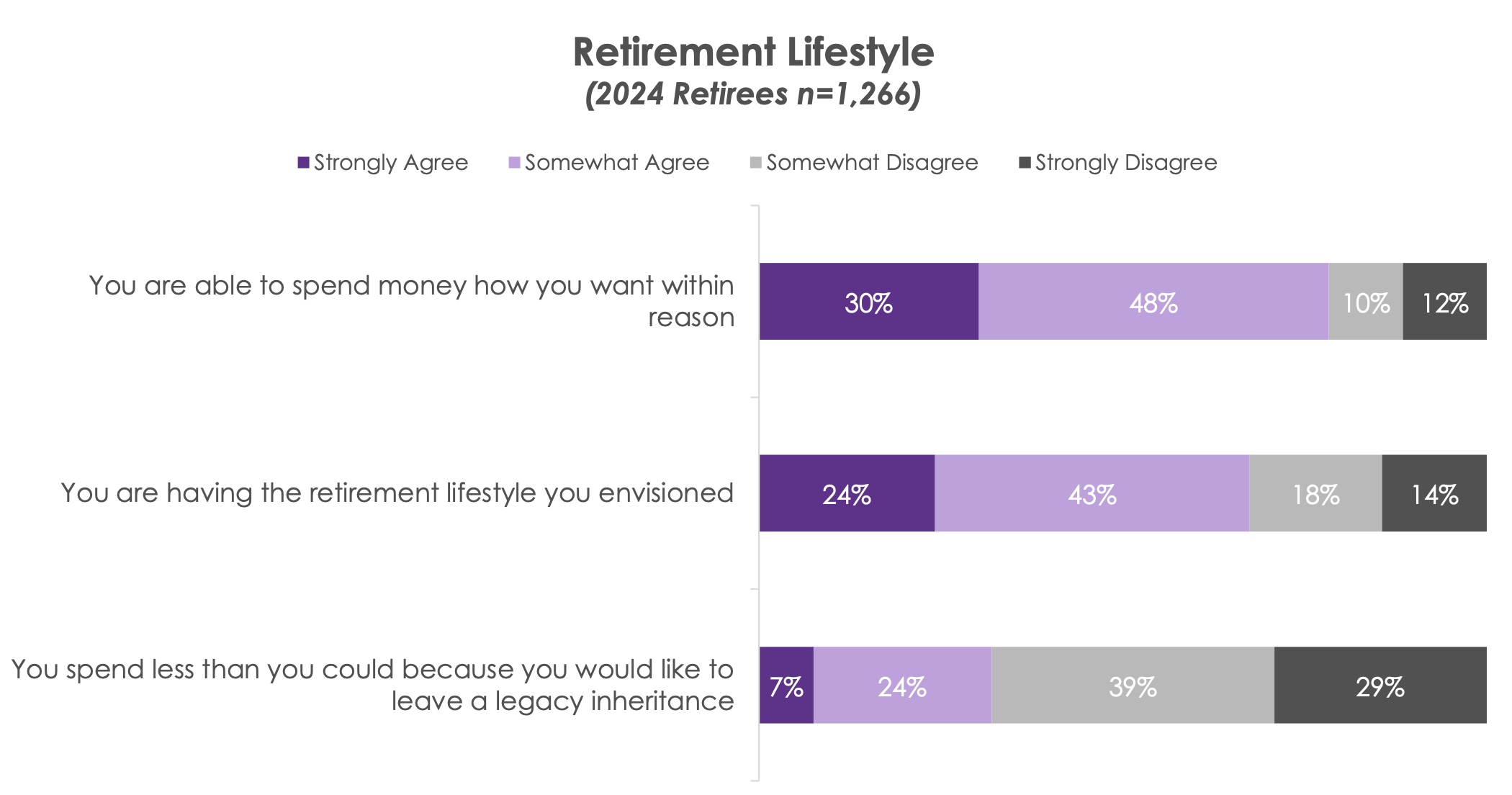

While over half of retirees say their overall expenses in retirement are higher than they originally expected, nearly four in five say they are able to spend money how they want, within reason.

Despite higher-than-expected costs...three in 10...believe their overall lifestyle in retirement is better than expected.

Additionally, over two-thirds of retirees agree they are having the retirement lifestyle they envisioned. A quarter of retirees strongly agree with this statement.

Not only are retirees managing their current expenses, but 58% say they are still saving for the future. In addition, they are planning for the next generation, as nearly two-thirds of retirees are confident they will have enough money to leave an inheritance.

Many workers are thinking ahead

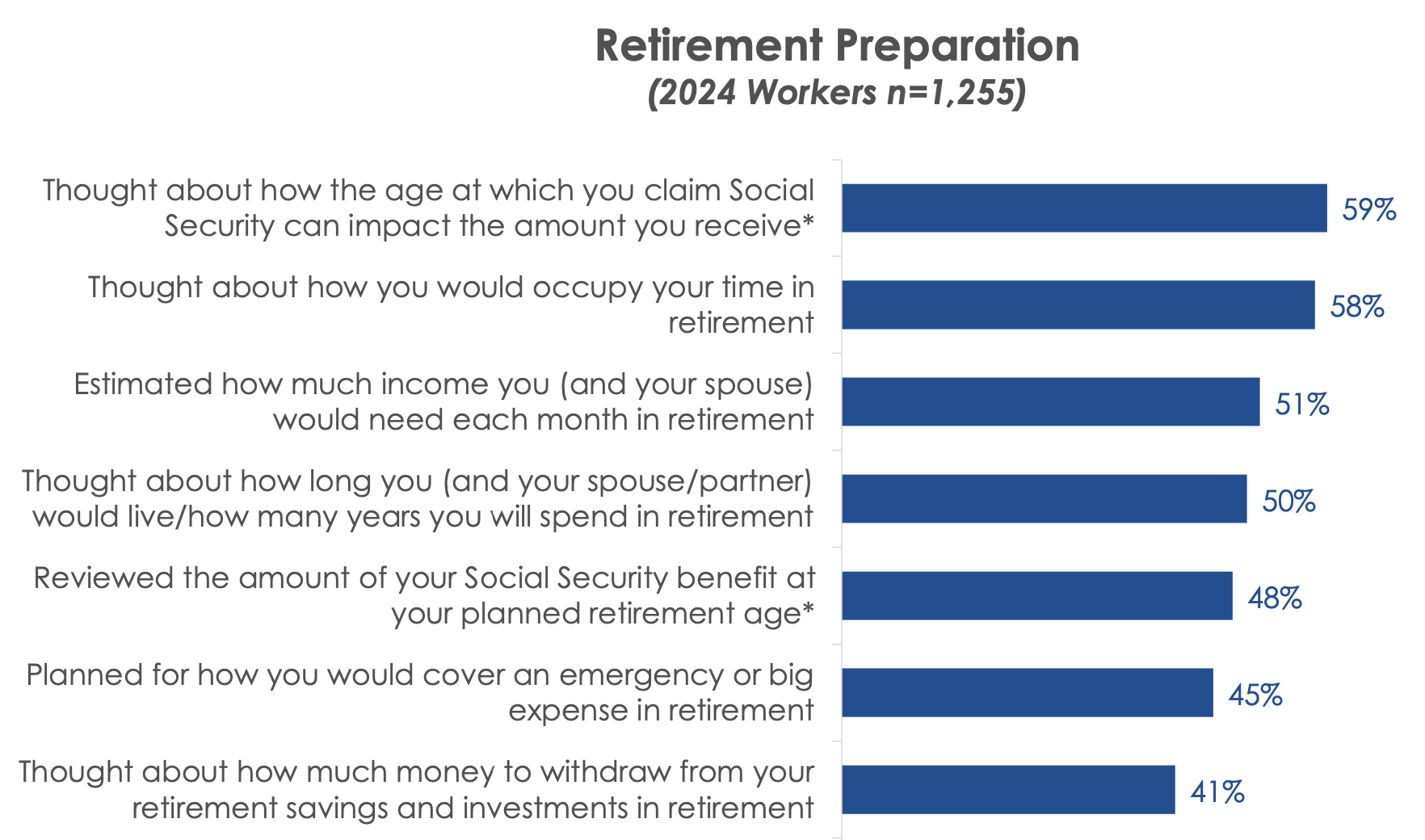

Among the non-retirees surveyed, nearly 6 in 10 have considered a Social Security claiming strategy (a crucial decision), and more than half have attempted to project their future living expenses in retirement.

The most engaged group

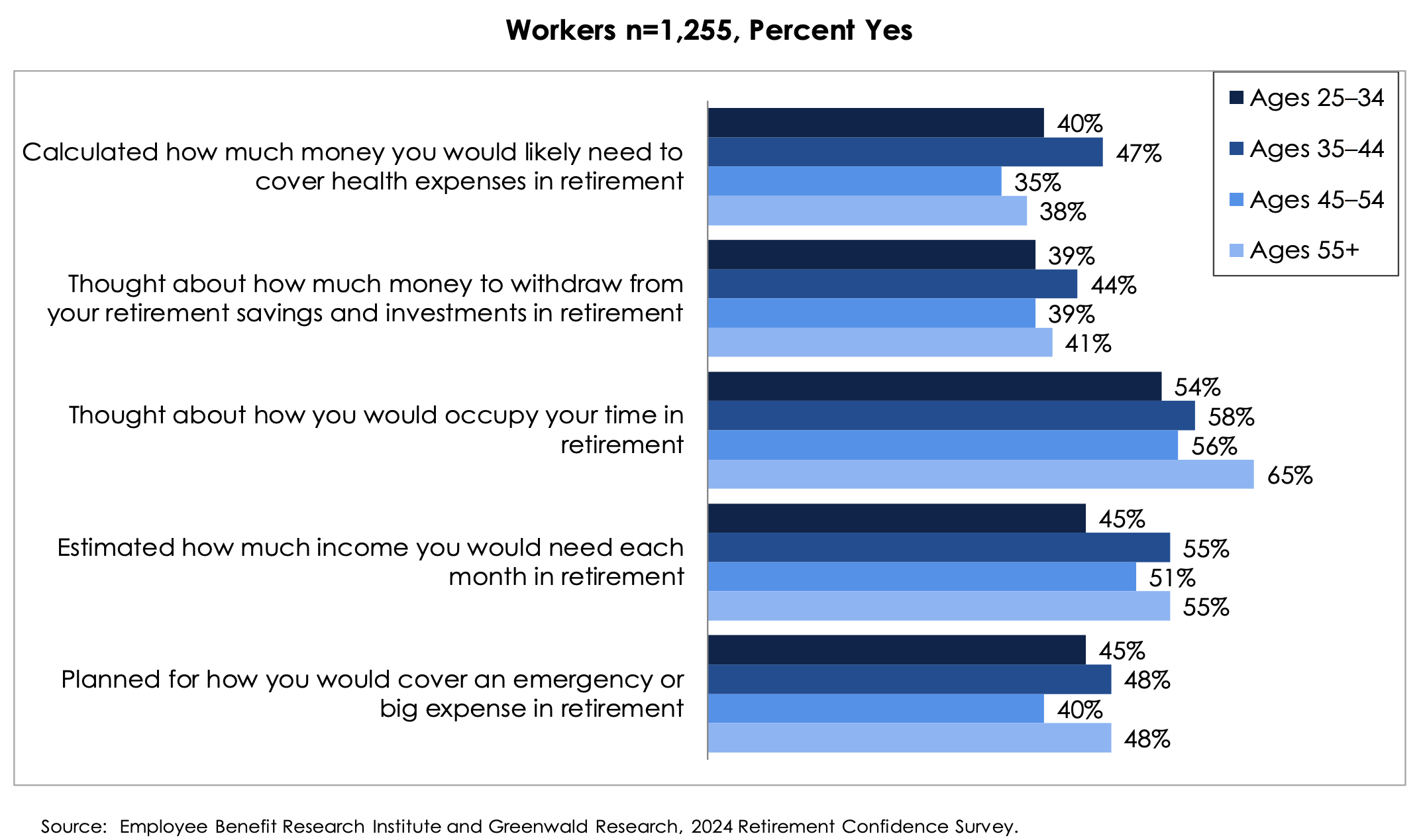

Some aspects of this year's Retirement Confidence Survey are somewhat curious. As Matt and I were discussing the RCS findings, he pointed out this chart, showing that workers aged 35-44 appear to be more engaged on retirement-related issues than workers 45 and up.

Perhaps workers in the 35-44 group are more concerned (than older cohorts) about what might happen with future Social Security and Medicare benefits. Or maybe they are more plugged into financial matters because of the many "fintech" apps that have made money management cool — or at least less tedious.

At any rate, the financial engagement of 35-44-year-olds seems to be a good sign. However, the somewhat lesser engagement by people a bit older is puzzling.

A bit of optimism

Survey findings sometimes raise as many questions as they answer! But it's encouraging that many of today's retirees seem to have prepared adequately for their retirement years. And, despite the unevenness of the data, many current workers appear to be making at least some preparation steps for their later years.

Obviously, more workers need to engage on these issues while they still have time to prepare sufficiently. But, to the optimistic eye, the RCS data suggest the glass may be half-full.