A few quick thoughts on the day of the first Fed rate hike since 2018...

I wrote an article yesterday that I intended to post today, but the market reaction to today’s Fed meeting is so...wow...that I’m holding that for tomorrow and writing up my thoughts on today’s action instead.

First of all, there’s always the potential that I’m flat wrong in how I’m interpreting all this. But I’m surprised investors interpreted what they just heard from Fed Chairman Powell as being positive for stocks.

A quick recap: The Fed raised the shortest term rate by 0.25% today, as expected. Powell communicated that every Fed meeting this year is fair game for additional hikes and that they will consider hiking more than 0.25% if warranted.

Translation: they’re serious about fighting inflation.

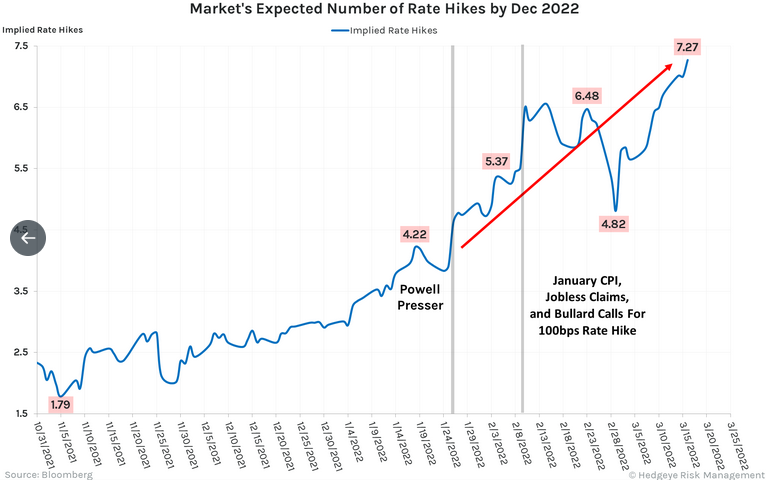

Background: the market is anticipating seven rate hikes from the Fed this year. Seven!

The Fed basically aligned itself with the market’s expectation today. This is not — in any way, shape, or form — good news for the stock market.

In SMI’s January cover article, Winds of Change Are Blowing: Casting a Wary Eye on 2022, we detailed four specific reasons we were concerned a bear market was looming this year. The first specific concern was that by the second quarter it was going to be clear that growth was slowing. Here we are in March, two weeks from the second quarter beginning, and it’s showing up in all the data already. The last specific concern, which I stated was the one that concerned me the most, was that the Fed was going to tighten policy into the face of this slowing growth.

That’s exactly what the Fed confirmed today.

Importantly, we wrote all of that in December of last year, before there was any inkling that Russia was going to invade Ukraine. If a peace deal was signed tomorrow, it wouldn’t change the underlying problems pointing to slower growth and tightening monetary conditions.

A circumspect bond market

Ironically, while stock investors appear oblivious to all this (pushing the indices substantially higher today), the bond market seems to get it. While the Fed was hiking short-term rates today, long-term rates were subdued. In fact, TLT (the iShares 20+year Treasury Bond ETF) was up nearly 1% today — the opposite reaction one would expect on a day "interest rates" were rising.

I put that in quotes to illustrate the idea that "interest rates" don’t move monolithically any more than "the market" does on the stock side. There are often differences between various parts of both the stock and bond markets and how they respond to various news. In this case, short-term rates (which the Fed largely controls) were rising but long-term rates (which are set by investors in the market) weren’t.

The simple reason LT rates weren’t rising is bond investors see the slowing economy. If anything, the Fed’s hawkishness (meaning their communicating that they plan to be aggressive in attacking the inflation problem with rate hikes) made bond investors even more nervous about future economic growth prospects.

Bottom line

The unfortunate reality that seems to not have sunk in for stock investors yet is that if the Fed really does hike seven times this year, we’re going to have a recession. The yield curve (which Joseph wrote about a couple of weeks ago), is already inverting at various points (the 5-yr yield briefly moved higher than the 10-yr yield today, with both closing at 2.18% today). An inverted yield curve is one of the most reliable indicators of future recession and the Fed has never started an interest rate hiking cycle with the curve so close to inverting. It seems unlikely they will be able to hike multiple times without fully inverting the curve by driving short-term rates higher than long-term rates.

Anything can happen in markets, which is why I continually remind SMI members that we deal in probabilities, not certainties.

But what I took away from today’s meeting is that the Fed was communicating as clearly as they could that fighting inflation is now priority #1, not fostering growth. It’s been so long since investors have had to deal with a legitimate inflation problem that many seem to think they can have both. They can’t. The actions required from the Fed to fight inflation will hurt economic growth — in fact, they’re explicitly designed to do so.

Think back to the last significant inflation crisis the Fed had to deal with. After a decade of inflation in the 1970s, the Fed finally cranked rates up to the point that the economy had the dreaded "double-dip" recessions of 1980 and 1982. As crazy as it sounds to modern investors’ ears, the whole point of raising interest rates is to slow down the economy. That is what brings inflation down! With no inflation to worry about the past dozen years, the Fed has been able to focus exclusively on promoting growth. Today’s Fed meeting was the clarion call that this has changed and bringing inflation down is now the priority.

The data says the economy is already slowing, and now we have a Fed intent on aggressively raising rates to slow it down even more. Somehow, stock market investors interpreted this as positive news today.

The good news is our SMI process has been navigating this treacherous market really well over the past several weeks. There’s more on that in tomorrow’s post. Sorry to be the bearer of bad news today, but I want you to be able to frame today’s events in a proper context. There’s no reason to despair, but unfortunately, I don’t see any reason to take today’s events as anything likely to change the longer-term bearish trajectory the market has been on so far this year.