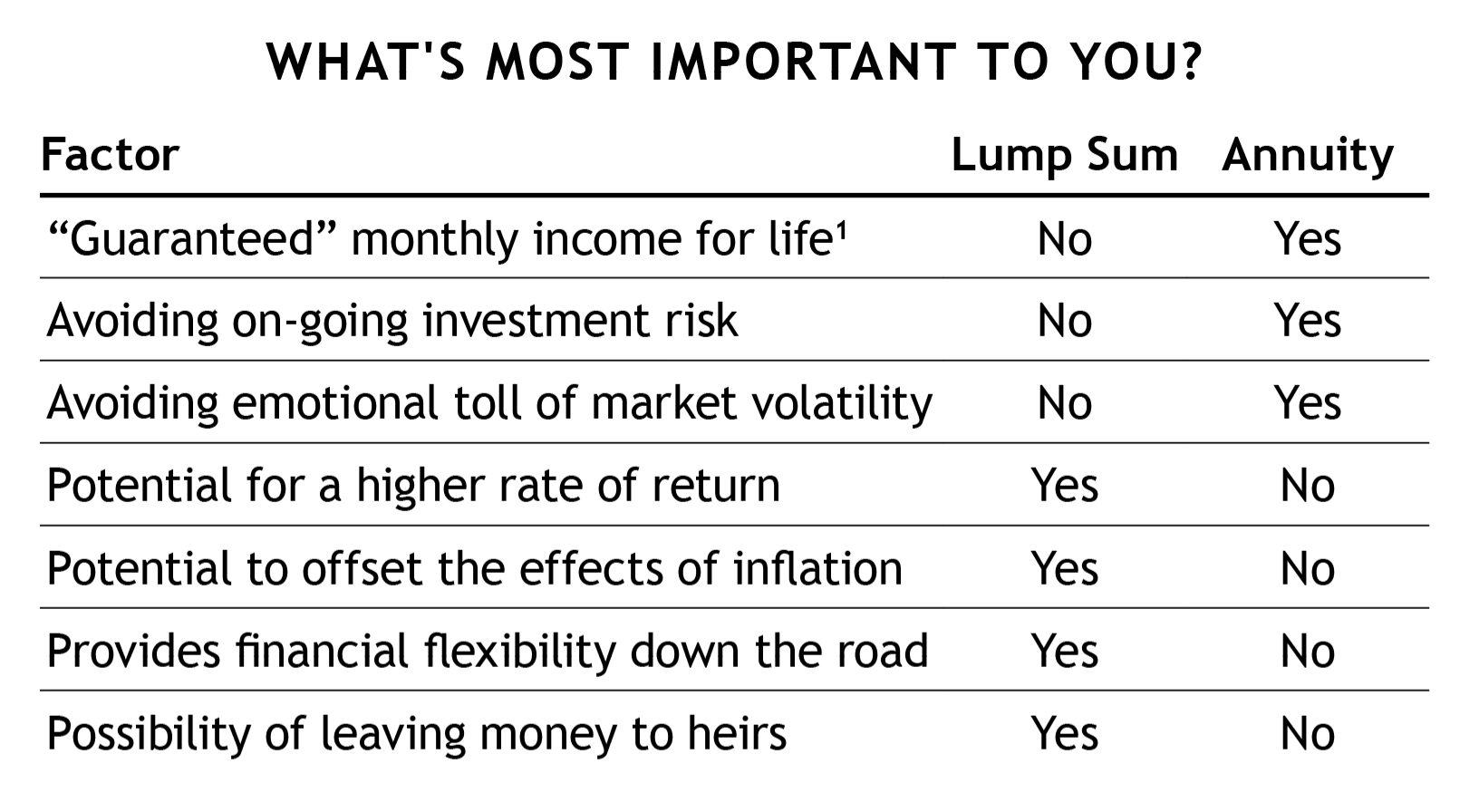

One of the most important, irrevocable financial decisions many people ever face concerns how they will receive the money out of their retirement account when they retire. For certain types of retirement plans, employers offer a choice: either take a single one-time payment (“lump sum”) and invest it yourself, or take a series of guaranteed monthly payments over a specific period (“annuity”). Which is the better choice?

That’s a bit like asking, “Which is the better tool, a hammer or a screwdriver?” It depends on what you’re trying to accomplish. Let’s look at how each of these financial tools works so you can determine which might be better for your situation.

With a lump sum, you control the investment options and timing decisions related to your retirement funds. By choosing to manage the money yourself (or hiring someone to do it), you assume the investment risk. If you pick a well-diversified allocation and the markets are favorable, you have a reasonably good chance of outperforming the return on an annuity. Of course, the opposite is also true: the annuity may outperform depending on what the markets do over your holding period. Also, to the extent you have some of the lump sum remaining at your death, you can pass it on to your heirs. Normal estate and income tax rules still apply.

In contrast, an annuity removes the investment risk from you and transfers it to an insurance company. When you select the annuity option, your employer typically takes the lump sum you would have received and uses it to purchase an annuity for your benefit. You will receive monthly payments that are guaranteed either for an agreed-upon number of years (“period certain”), or over your (and, if you choose, your spouse’s) lifetime.

In this arrangement, the ongoing investment decisions and performance are no longer your concern. However, you still bear the risk that the insurance company or annuity provider could become insolvent and fail to make your payment. Therefore, it’s critical that you check the strength of the annuity underwriter and whether your employer will pay as a last resort should the insurance company fail to do so.

To hedge against default, you might consider spreading your annuity over several companies if your company offers that. In addition to the risk of default, depending on your annuity’s earnings, there is the possibility of losing ground to inflation — the silent enemy of the retiree.

1 Bear in mind that the guarantee is only as solid as the health of the insurance company from which you purchase the annuity.

So, how do you decide which option is better for you? A simple three-step process should help you decide.

Step 1: Know the annuity’s imputed return.

Determine the annuity’s implied rate of return, meaning the return you earn by giving your lump sum to an insurance company. Take the monthly payment you would get from the annuity, multiply it by 12 to make it an annual figure, then divide that number by your lump sum amount. This gives you a reasonable estimate of what your annuity option is earning after taking out fees and expenses (although it will tend to be a bit high as it ignores the partial return of principal in each monthly payment).An example will help. Assume a lump sum of $120,000, and the monthly annuity payment is $500. Multiply the monthly payment by 12 months to total $6,000. Dividing the annual annuity income ($6,000) by your lump sum ($120,000) gives you an average return of 5%.

Investing in a diversified growth-oriented portfolio would likely earn more than 5% over the long term. But you would have to endure market volatility, make asset allocation decisions, incur investing expenses and hope that you (or your investment advisor) make good decisions. So even if the potential return could be higher from the lump sum, you need to decide how you feel about these other factors.

Step 2: Know your risk tolerance.

Asset allocation is key in determining what the annual return on your lump sum is likely to be. There’s no sense in thinking about higher potential returns if your risk tolerance will limit your allocation to very safe or conservative investments. A risk tolerance questionnaire is a good start but may only tell part of the story. Sometimes a person’s risk tolerance unexpectedly drops significantly when stocks are in free fall. Consider your reaction to the 2008/2009 bear market. Did you sell stocks? Did you learn your true risk tolerance is not what you thought?Don’t forget, declining markets are not the only risk. You might outlive your principal (longevity risk). You might lose purchasing power (inflation risk). You might not be able to get to your money in an emergency without a large loss or penalty (liquidity risk). Successful investing is not about avoiding risk. An investor cannot avoid all risks. Your goal is to tailor risk to meet your specific objectives.

As you can see, many factors should be considered besides your risk tolerance. If you want to safeguard the return and aren’t concerned about retaining flexibility and control (or leaving a balance for your heirs), the annuity might be a good choice. On the other hand, if you are willing to endure volatility on your monthly statement for the chance of doing better than the annuity return (plus the possibility of having more left for your heirs), the lump sum has merit.

Step 3: Know your income needs.

Determine how much income you’ll need in retirement. If the annuity income is sufficient and leaving some of this money as an inheritance isn’t a priority, the annuity can be compelling. On the other hand, the lump sum option is attractive if you need more income than the annuity provides and are willing to assume investment risk to get the return, or if you want to try to leave some of your retirement benefits to your heirs.

To sum up, if flexibility is a major objective, the lump sum is usually the way to go. That’s because the annuity option, once chosen, is irrevocable and generally offers little flexibility. If you do select the annuity, you’ll need to decide over what period you (the annuitant) want the monthly benefits paid. The most common options are:

Single life means you receive benefits for your lifetime. When you die, so do the benefits. Your spouse gets nothing. Joint and survivor means at your death, your surviving spouse still receives a monthly benefit until his or her death, though the dollar amount is generally reduced by 25% or 50%. Realize that under this option, the dollar payout while you are alive is generally less than a single life payout.

Period certain means the monthly benefit is paid for a certain period even if the annuitant dies early. The surviving spouse or named heirs would receive the unpaid accrued benefit.

Still can’t decide? Proverbs 15:22 says, “With many counselors there is victory.” Talk to people who have already made this decision. While a financial advisor may be helpful, just remember advisors make nothing if you go with the employer-provided annuity, which may influence an advisor to encourage the lump sum option. And of course, pray about it, as God promises to grant wisdom to those who genuinely ask.