With most asset classes delivering strong gains through the first nine months of 2024, it’s easy to forget that investors had to hold on tight during some early third-quarter volatility.

Between July 16-Aug. 5, stocks fell sharply and unexpectedly. In something of a “chicken or the egg” conundrum, explanations differ as to whether it was a pullback in U.S. tech stocks that caused the Japanese Yen “carry trade” to unwind, or vice versa. But either way, market volatility briefly spiked and stock market prices fell sharply. The S&P 500 Index dropped -8.5% over that three-week period, while the tech-heavy Nasdaq Index fell -12.5%. Dwarfing those declines, Japanese stocks dropped -12% on August 5 alone and were down more than -20% overall.

Two positives emerged from this painful reminder that stocks don’t always go up. First, it was mercifully brief. As quickly as it started, it reversed. While stocks would drop sharply again during the first week in September, they posted surprisingly strong returns for the quarter as a whole, especially in light of the significant losses of those three weeks.

Second, for the first time since rates started climbing in 2022, bonds cushioned the blow of declining stocks. The Bloomberg U.S. Aggregate Bond Index gained +2.2% during the July 16-August 5 stock market selloff. It was the first significant decline in stocks since 2022 that wasn’t accompanied by falling bond prices driven by rising interest rates.

Just-the-Basics (JtB) & Stock Upgrading

Despite the brief wobble in late July, the overall trend for stocks during the third quarter was higher, as it has been throughout the past year. The Wilshire 5000 Index gained +6.2% during the third quarter and ended September up +20.6% year-to-date.

SMI’s Just-the-Basics indexing strategy was a bit stronger during the third quarter, gaining +7.1%, but has been a bit weaker overall for the year, up +16.2% year-to-date (thru 9/30). As we’ve noted many times, the rally was largely driven by the “Magnificent Seven” tech stocks during the first half of this year. The more diversified JtB portfolio lagged the large-company stock indexes through that period.

But the market rally broadened considerably during the third quarter (and has continued to do so in October), while the big tech stocks have taken a breather. This is evident in JtB’s stronger third-quarter results. From the beginning of July through mid-October, the small-company Russell 2000 index gained +12.1%, while the large-company S&P 500 Index was up just +7.4%. That’s a very significant difference from earlier in the year when the leadership roles were reversed.

Stock Upgrading was a bit slower than the indexes during the third quarter, gaining +3.8%. But for the first nine months of 2024, it has done an excellent job, gaining +19.2%.

Of particular interest to SMI members, the new Full-Cycle Trend model had a great third quarter, gaining +11.3%. Its year-to-date gain of +27.6% through September 30 is equally impressive. Drilling down more specifically, from July 26, when the new FCTE holding was first included in Stock Upgrading, through the end of the quarter on Sept. 30, FCTE gained +6.35% while the S&P 500 was up +5.8%. So we’re off to a good start with that large company stock holding!

Bond Upgrading

As noted earlier, it was a great quarter for bonds, a rarity since rates started climbing sharply three years ago. The broad bond market was up +5.2% during the third quarter, turning a small first-half of 2024 loss into a year-to-date (thru 9/30) gain of +4.45%.

Unfortunately, those good times were short-lived, as longer-term yields reversed course immediately following the Fed’s Sept. 18 rate cut. Rather than follow shorter-term yields lower, the benchmark 10-year Treasury yield rose from 3.65% to 4.09% in the three weeks following the cut (and has continued to rise throughout October, recently hitting 4.30%). As SMI investors know, higher yields mean falling bond prices, and the bond market gave back a fourth (-1.1%) of its year-to-date gain by mid-October.

Bond Upgrading avoided much of that volatility by virtue of its 50% allocation to Bulletshares, whose price doesn’t vary as much based on interest rate changes. Bond Upgrading “only” gained +3.3% during the third quarter when bonds were racing higher, but also only gave back -0.4% during the first half of October.

Altogether, after losing less than the broader bond market in 2022/2023 by being more conservative with its bond positioning, Bond Upgrading has trailed a bit so far in 2024. But the year isn’t over yet, and with bond yields climbing again, it may yet have the last laugh by the end of the year. Either way, we still think Bond Upgrading’s conservative positioning has been appropriate given the longer-term secular bond bear market that we believe started in 2020.

Dynamic Asset Allocation (DAA)

DAA was surprisingly strong during the third quarter, gaining +9.9%. Its year-to-date gain of +19.8% is also surprisingly robust, given this strategy’s defensive reputation and tendency to lag during strong bull markets.

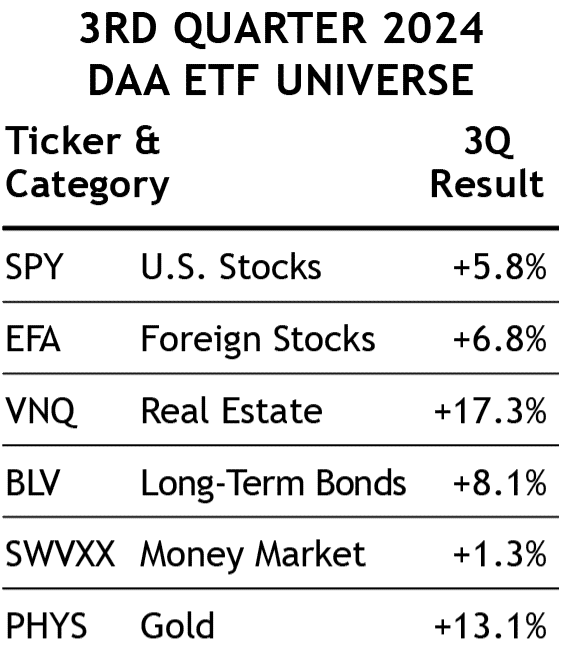

Driving the recent strength has been DAA’s large allocations to gold and real estate. As the inset table shows, both were up double digits during the third quarter (although it should be noted that Real Estate wasn’t added to DAA until the end of July). U.S. Stocks were the laggard during the third quarter, which is a bit ridiculous given SPY’s third quarter gain of +5.8% annualizes to a rate in excess of +20%! But it just goes to show how strong the overall market environment was during the third quarter.

Sector Rotation (SR)

It’s been a year of dramatic swings for SR in 2024, and that pattern continued during the third quarter. SR was up over +18% year-to-date by early July, but its exposure to tech stocks cost it dearly during the July/August market swoon. By Aug. 7, SR year-to-date gain had flipped to a -6.6% loss. Since then, SR has gained +15.7%, pushing it back to a year-to-date gain of +8.2% as of mid-October. But the volatility is hard to deal with and we continue to look closely at SR for ways to improve both its overall performance and volatility profile.

50/40/10 (with 60/40 stock-bond Upgrading)

This portfolio refers to the specific blend of SMI strategies — 50% DAA, 40% Upgrading, 10% Sector Rotation — discussed in our April 2018 article, Higher Returns With Less Risk, Re-Examined. For 2024, we’ve started reporting this portfolio using a 60/40 split between Stock & Bond Upgrading within the 40% Upgrading allocation. This is a reasonable reflection of how most SMI investors utilize such a “whole portfolio” blend and is a great example of the type of diversified portfolio we encourage most SMI readers to consider.

This version of a 50/40/10 portfolio gained +5.6% during the third quarter. Its year-to-date (through 9/30) gain of +15.0% compares favorably with the +11.5% a well-diversified 60/40 JtB portfolio would have earned, or the +12.3% of a 60/40 Upgrading portfolio.

Conclusion

It’s been a strong performance year for markets and the SMI strategies. Most SMI members likely are experiencing all-time highs in their accounts as a result. Of course, long-term investors know that bull markets don’t last forever. Having the confidence to stay invested, which allows us to capture gains such as we’ve experienced this year, is an underrated aspect of using strategies such as those provided by SMI.

A year ago, there was no shortage of worry as the expectation of an early 2024 recession was nearly universal. Many investors either sold investments or changed their allocations due to those expectations. We avoided that trap and have earned strong returns as a result.

That broader dynamic now sets up the potential for many institutional investors having to “chase” markets higher into year-end due to lagging their benchmarks earlier in the year. This is one aspect of what drives the “Santa Claus” effect and other positive year-end investing patterns. It’s not that people feel warm and fuzzy around the holidays so they bid up stock prices. Rather, there are structural and market flow factors that combine to typically make the weeks between now and the middle of January one of the strongest performance periods of the year. Here’s to a strong fourth-quarter finish for SMI investors!