Today was the second-largest spike in single-day stock market volatility since 1990 (as measured by the VIX). This followed two days of nasty selling to end last week, which followed the Fed's decision to hold interest rates steady last Wednesday. Lots of noise there, but where's the signal?

It's easy for U.S. investors to view everything that happens in markets as being about us, because, well it often is. But it isn't always and this is one of those times. Yes, slowing growth data here in the U.S. contributed to this move, with Friday's soft employment report getting a lot of attention. And the timing of the Fed decision is easy to look at as a potential smoking gun. I'm seeing a lot of fingers pointing in a lot of different directions today as investors try to sort out what's going on.

Unwinding the Japanese Yen "carry trade"

While it's always tricky unraveling these threads in real time, the primary cause of the recent market rout is a massive unwinding of leverage in the financial system. Specifically, this stems from changes going on in Japanese monetary policy and Japan's emergence from decades of low and negative interest rates. For many years, sophisticated investors would borrow in Japanese Yen, taking advantage of these low rates, then investing the proceeds in other markets/countries, etc.

Currencies get complicated and confusing quickly, so I'm not going to do a deep dive here. But suffice it to say, a month ago one U.S. dollar would purchase nearly 162 yen, whereas today that same dollar would purchase just 143 yen. That means the yen has strengthened substantially relative to the dollar (or the dollar has weakened relative to the yen, those are flip sides of the same coin).

This is the result of a combination of factors that include Japan's central bank raising interest rates, the Fed not cutting rates as quickly as some might have expected, slowing U.S. economic growth making the case for a weaker dollar more likely, and so on. It's very difficult to ever fit all the narratives together tightly, and it's not especially important in this case anyway.

What is important, is that currency trades (like the yen carry trade, more detail here) are typically taking advantage of tiny variances in valuations. Which means to make them worthwhile to pursue, many investors pursuing them do so with significant leverage. And as SMI readers know, leverage cuts both ways. When the Mag 7 is going up 5% per month, leverage feels great. When the air is coming out of the balloon at the same time the currency you've borrowed in to invest in those stocks is rapidly re-pricing, accounts suddenly blow up.

Japanese Nikkei index is the tell

Japan's (Nikkei) stock market was down -12% today, the worst day of any major stock index since Black Monday in 1987. Since peaking on July 11, the Nikkei is down more than -20%. These are huge moves that dwarf the declines of the U.S. indices.

Why do we care about that? Well, for starters, it indicates that this event is primarily a leverage unwind, as opposed to a dramatic shift in, say, expectations regarding a U.S. recession, or U.S. companies bombing their earnings this quarter. That's important, because both of those narratives are flying around right now and I think they're a bit misplaced.

Admittedly, a leverage unwind being the catalyst is a good news/bad news type of situation. It's good news in that, absent a deep recession, it's hard to imagine U.S. stocks slipping into a 2008-type bear market. But it's bad news from the standpoint that the buildup of leverage in the system has been massive and this unwind has been relatively tiny in comparison. So there's no assurance this will be short-lived or quickly put behind us.

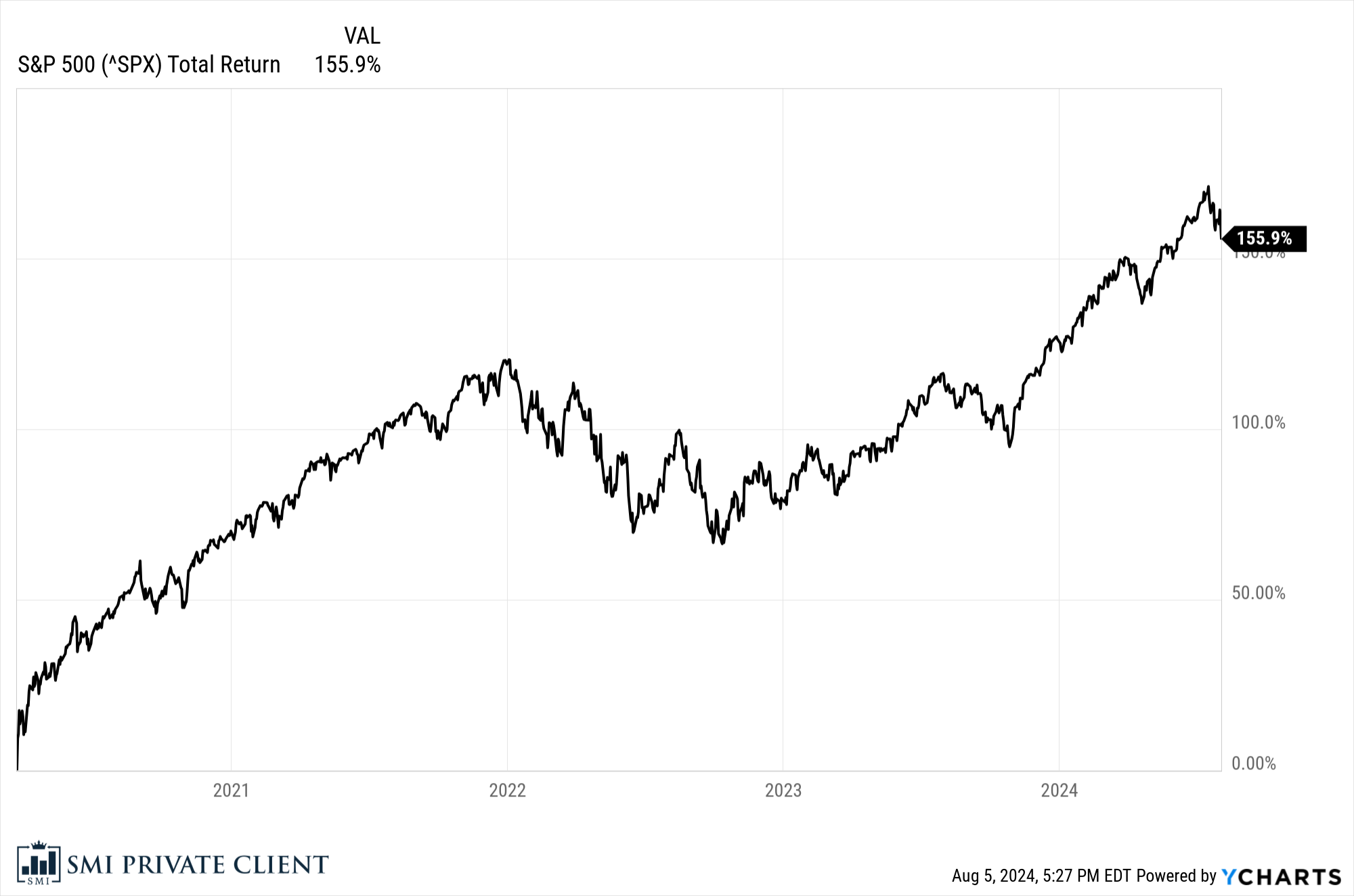

The chart below offers another way of making that same point. Since the COVID low in March 2020, the S&P 500 Index is up nearly +156%. The recent correction has knocked about -8.5% off the index. That's not nothing, but it's a very unexceptional drawdown.

What to do with this information

Add all this up and it leads to a situation where I'm not enthusiastically running out to buy this dip immediately, but nor am I really sweating that this is the beginning of the end of this bull market. Granted, it could be. We've been noting the signs of slowing growth and Friday's employment report was the weakest yet. So maybe we will slide headlong into recession, as so many are suddenly claiming.

The thing is, Friday's employment report really wasn't all that bad. Neither are the U.S. growth numbers. The Fed is already primed to cut interest rates — they told everyone that explicitly last week — and the bond market has already front-run the Fed by pricing in a slew of cuts between now and year-end (continuing into next year).

One scenario is we get more selling now, cascading to some sort of true panic that forces the Fed's hand into a more immediate cutting posture. The Fed doesn't want to cut before their next meeting six weeks from now, because the market very well may interpret such an emergency cut as a reason to really panic. But they'll be jawboning like crazy trying to reassure markets. I'm sure they would love to get to their much-watched Jackson Hole symposium on Aug. 22 without having to take any emergency action.

That said, I'm not convinced that's the most likely scenario. As leverage unwinds, it forces each borrower hit with margin calls (or simply rules governing their accounts) to pare back risk. But at a certain point, that selling cascade can run out of forced sellers, leaving everyone to wonder what the panic was all about. Consider this track record of past volatility spikes similar to what the market has experienced over the past few weeks:

The $VIX has increased by 88% over the past 3 weeks, the 15th biggest 3-week spike ever. Here's a look at how the S&P 500 has fared following big $VIX spikes in the past... pic.twitter.com/KABAwRldQR

— Charlie Bilello (@charliebilello) August 5, 2024

I'm not usually a huge fan of these "average of past examples" stats, but it's impossible not to notice that the average of the 20 worst prior volatility spikes just like this one resulted in significantly better returns over the next year than periods when there was no volatility spike to kick it off. This chart doesn't say anything about what the next weeks or months may look like, but it's almost all green in terms of looking out a year or more.

When I combine that historical record of past volatility spikes with a Fed that is itching to cut rates and ease monetary conditions, an economy that is slowing but seemingly still not particularly close to rolling over into recession, a government running a deficit of 5% of GDP (bad long term, but that spending is a fire hose of economic support in the short term), and an election calendar that normally turns south in August-October before rallying like crazy into year-end (and has been getting front-run by investors all year)...the balance of evidence seems to weigh in on this not being the beginning of the end. I have plenty of concerns about how 2025 may play out, but this seems too early.

SMI has a process for this!

Most importantly, SMI has a process to navigate all this. We don't have to guess — and you don't have to rely on my finger-in-the-air-trying-to-make-sense-of-it-all analysis!

What has the SMI process been doing lately?

Ten days ago (July 26), we cut our largest holding (IWF) in Stock Upgrading by two-thirds, replacing it with a new Full-Cycle Trend model that dramatically reduced our reliance on the "Magnificent 7" giant tech stocks. Over the past 10 days, that new model has dropped -2.8% while IWF is down -10.1%.

Last Wednesday, we sold Foreign Stocks (EFA) within our Dynamic Asset Allocation strategy just before the wheels fell off in Japan, replacing it with a more rate-sensitive Real Estate holding. Since Wednesday's close, EFA has lost -6.3% while our new real estate holding is down a third as much at -2.1%.

Both of these steps reduced our risk and have paid off quickly. But there are plenty of other steps we've taken this year that have helped as well, not the least of which is the hefty Gold allocation we've sported throughout 2024.

The point isn't to pat ourselves on the back, and it certainly isn't to try to predict what's going to happen over the next days or weeks or months. It's to point back to the system — the process that allows us to not feel like we have to react to days like today by "doing something." If there's something that needs to be adjusted, our process will register that and we'll make those adjustments in the measured, consistent way we always do. For now, the steps we've taken recently have us weathering this correction pretty well.

Follow along on X/Twitter

I've only recently started getting more active on X/Twitter, but the events of the past week are a good illustration of why I'm I'm trying to do so. Last week I was traveling all week for a funeral. Unfortunately as soon as I got home, I got drilled with COVID and have been fighting that ever since!

Events like these sometimes make it hard to get much long-form writing done. But I'm always reading and reacting to market events — X makes it possible to at least "re-tweet" things I find to be interesting or insightful about markets, often with a comment or two attached.

If you're on X/Twitter and want to follow along, you can follow me at @mark_biller.