A lot can happen over the course of a calendar quarter. Investors started 2025 largely euphoric, but ended the quarter nervous. It quickly got even worse — President Trump’s April 2 tariff announcement sent stocks sharply lower as the second quarter began.

So much has transpired since the end of the first quarter that it feels like old news to focus much attention there. We’ll quickly review the first quarter as well as how each strategy has responded to April’s wild market action.

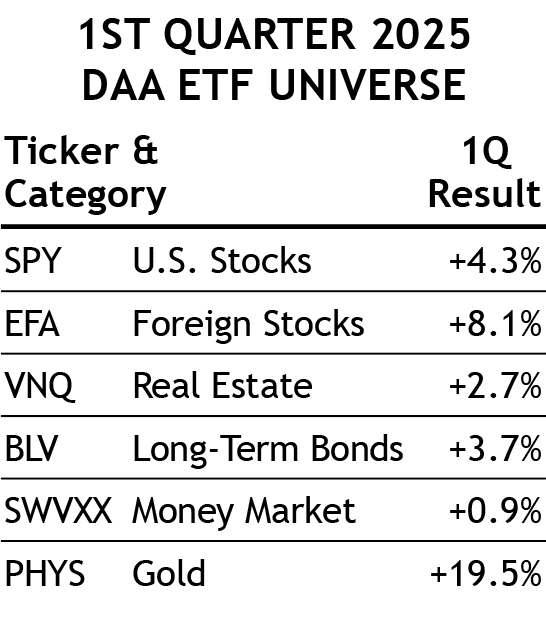

Stocks rallied through mid-February, with the S&P 500 Index setting a new all-time high on Feb. 19. But storm clouds were already forming on the horizon. China’s January “Deepseek” news of a competitive Artificial Intelligence model that could operate at a fraction of the cost of the U.S. big tech models had already rattled the U.S. tech sector. Tariff talk intensity would soon increase as well.

Bonds helped cushion stock market declines initially, with the Bloomberg U.S. Aggregate Bond Index gaining +2.8% during the first quarter. That partially offset the U.S. stock market’s -4.8% first quarter loss. However, as April’s stock market decline accelerated, the abrupt change of behavior in longer-term U.S. Treasury bonds became a primary storyline. After falling initially (causing bond prices to rise), the 10-year and (especially) 30-year Treasury yields spiked higher, a marked departure from their normal behavior as a flight-to-safety asset during times of market distress.

(The likelihood of this stocks-down/bonds-down scenario, in contrast to the way bonds have cushioned stock market losses for investors in recent decades, was the focus of SMI’s March cover article: Real Asset Allocation: The World Has Changed.)

Just-the-Basics (JtB) & Stock Upgrading

SMI’s JtB allocation tweaks for 2025 have produced mixed results so far. Shifting 10% of JtB’s allocation from small stocks to large has worked out well, as year-to-date losses for small stocks were nearly twice that of large stocks (-11.5% vs. -5.7% through April 28). On the other hand, reducing JtB’s foreign stock allocation (+8.5% YTD) has offset that advantage.

Stock Upgrading’s (SU) incremental risk management efforts during the first quarter paid off during April’s steeper market decline. Through April 28, SU led the S&P 500 by a -3.7% to -5.6% margin, while the small-company focused Russell 2000 was down -11.5%.

At the end of January, SU shifted 10% of its allocation out of small-company growth stocks (IWO) and into commodities (SDCI). Through the end of the first quarter, SDCI would gain +4.2% while IWO would lose -13.6%.

Two months later, just before the end of the first quarter (March 26), SU sold three holdings that had been part of the portfolio since mid-2023. One was a swap of small company value funds: the fund sold (HFMDX) has lost -6.3% since then, while its replacement (AVALX) has gained +1.6% over the following weeks (through April 28).

Another of the March 26 changes shifted 10% of the portfolio out of large U.S. growth stocks and into international stocks. This change also turned what would have been a loss (-3.3% in the fund sold) into a gain (+2.6% in the fund purchased).

Stock Upgrading’s primary large U.S. company position, FCTE, outperformed the S&P 500 Index during the first quarter (-3.1% vs. -4.3%) and continues to lead by 1.8% through April 28. FCTE’s limited scope of buying only high-quality companies is an embedded “baseline” of risk management, while its own internal process of “upgrading” its holdings based on recent trend and mean reversion factors (prices retreating to their long-term trend) helps keep it in the most attractive stocks.

Bond Upgrading (BU)

SMI investors may recall that last year we stepped away from the up-and-down roller coaster bonds have experienced recently as interest rates have repeatedly reversed course. Instead, we locked in a more stable path via BU’s current Bulletshares recommendation.

When bond yields were declining on economic slowdown concerns during the first quarter, traditional bond funds outperformed. But ironically, as markets unraveled in April, rather than seeing the traditional flight-to-safety response into longer maturity Treasury bonds, longer-term yields spiked higher. Our steady Bulletshares position gained ground quickly as that surprising dynamic unfolded. Through April 28, BU’s +2.3% gain year-to-date trails the bond index (+3.0%) slightly, though our return has come with considerably less volatility.

While bond returns haven’t been exciting, April’s climbing Treasury yields in spite of a falling stock market is an important signal. These yield increases appear to have forced some accommodation from the Trump administration (the first significant tariff “pivot” came the day after the 30-year Treasury yield had punched above 5.0% overnight). This positive stock-bond correlation, with both falling in price together, is the exact scenario discussed in SMI’s March cover article and the rationale behind the new Real Asset Allocation ETF recently added to DAA.

Dynamic Asset Allocation (DAA)

Driven largely by gold’s remarkable +56% gain since being recommended at the end of February 2024, DAA has generated some of its strongest ever relative performance lately. This continued during the first quarter, as it gained +3.8% while most markets fell. Foreign stocks, added at the end of January, also contributed significantly to DAA’s success while providing another excellent example of incremental risk management ahead of the decline in U.S. stocks.

Speaking of U.S. stocks, DAA adeptly exited its U.S. Stock position on March 31, days ahead of President Trump’s tariff announcement that sent U.S. stocks plunging. That move to cash paid off immediately as markets dropped in early April.

DAA underwent a significant change during the first quarter with the addition of the new RAA ETF. This addition hasn’t boosted performance yet, as DAA’s “legacy” holdings have been performing so strongly. This isn’t unexpected, as legacy DAA has normally done a great job at the start of past bear markets. But DAA hasn’t always done as well pivoting quickly back into higher risk assets once these market downturns end. We expect RAA to help with that and add considerable value to our process over time.

That’s not to say RAA won’t be a good performer if the current market correction continues. RAA’s internal trend-following process will cause it to de-risk further if the market’s negative trend is prolonged. This would trigger the specific risk-management features discussed in SMI’s March 2025 cover article. So far, relatively little of that adjustment process has occurred, given the swiftness and relatively short duration of the market’s decline.

Sector Rotation (SR)

It’s getting old reporting that SR lagged again, but not surprisingly, the market’s swift decline has been especially tough on this strategy. A poor first quarter got even worse when SR pivoted into energy stocks at the end of March. On April 2, not only did Trump’s tariff announcement deal a harsh blow to economic growth projections (negatively impacting projected future energy demand), but Saudi Arabia simultaneously announced it will boost supply much faster than had been previously communicated. Lower energy prices are great for U.S. consumers, but have pushed energy stock prices much lower.

50/40/10 (with 60/40 stock-bond Upgrading)

This portfolio refers to the specific blend of SMI strategies — 50% DAA, 40% Upgrading, 10% Sector Rotation — discussed in our 2018 article, Higher Returns With Less Risk, Re-Examined. In 2024, we began reporting this portfolio using a 60/40 split between Stock and Bond Upgrading within the 40% Upgrading allocation. This is a reasonable reflection of how most SMI investors utilize such a “whole portfolio” blend and is a great example of the type of diversified portfolio we encourage most SMI readers to consider.

This version of a 50/40/10 portfolio declined just -0.9% during the first quarter, which compares favorably with just about any blended portfolio metric. This strong performance was driven by DAA’s solid returns and is a good illustration that with solid diversification and appropriate position sizing, an overall portfolio can still excel even if one portfolio component performs poorly (as SR did this quarter).

(Note: For do-it-yourself investors, blending strategies adds complexity. Some members may prefer to use an automated approach instead.)

Conclusion

The aggressiveness of President Trump’s tariff plans has sent shockwaves through financial markets. The administration has clearly articulated that reshaping America’s trade policy is vital to the interests of regular workers, and they are willing to endure pain in financial markets to achieve their broader societal goals. This is quite a reversal from the past 15 years, when most bouts of market distress have been quickly resolved by strong policy responses from the Federal Reserve, the federal government, or both.

SMI has strong incremental risk-management processes built into its active strategies. These processes are rules-based and designed to keep us on the right side of the broad market trends. This means that if the market trend deteriorates sufficiently, our holdings will grow incrementally more conservative, including the potential of shifting assets to cash (as DAA did with a portion of its portfolio at the end of March).

While there’s always the risk that falling markets will snap back quickly — and investors have grown to expect that over the past 15 years — SMI’s approach will significantly reduce our risk should a deeper, prolonged bear market unfold. Given the ambitious nature of this administration’s goals to reorder the global economic system, we can’t rule anything out.