The financial markets packed a lot into the first quarter of 2023. Stocks enjoyed the strongest January since 2001, gave it almost all back during February and the early March banking crisis, then (part of the market) rallied strongly into the end of the quarter.

That last sentence alludes to the common problem in referring to “the market” as if all stocks behaved similarly. In fact, there were significant disparities between different groups of stocks during the quarter. Small company stocks (Russell 2000 index) managed a meager +2.3% gain for the quarter, whereas tech stocks (Nasdaq index) gained a shocking +16.8%!

The S&P 500 index’s quarterly gain of +7.5% looks great, but it’s worth noting it was up less than +1% at the bank crisis low of March 10. From that point through early April, Goldman Sachs noted that the six giant tech stocks which comprise nearly 20% of the index gained ~$620 billion in value, while the other 494 index constituents lost ~$950 billion. In other words, virtually the entire gain of the S&P 500 index during the first quarter was attributable to only six stocks. Those same six stocks make up 41.5% of the Nasdaq index, explaining its explosive first-quarter gain, while the Russell 2000 languished without any exposure to that group.

The bond market experienced an even wilder ride. Bond yields fell sharply in January (boosting stock returns), rose sharply in February (sending stocks lower), then fell sharply again in March after the bank crisis (sending stocks rallying into quarter-end). Bond volatility was exceptionally high all quarter, but especially once the bank situation began to unfold.

Relative to the narrowly focused stock-market-index gains, SMI strategy returns were pedestrian, as our portfolios contained virtually no exposure to the giant tech stocks. Of course, that was also the case through most of 2022, when those stocks fell sharply and SMI portfolios didn’t. It’s important to maintain a full-cycle perspective regarding our positioning and performance, as last year’s “good” far outweighed this quarter’s “bad.”

Just-the-Basics (JtB) & Stock Upgrading

Just-the-Basics gained a very reasonable +6.7% during the first quarter, given its significant exposure to smaller-company stocks which lagged. Its S&P 500 exposure helped and foreign stocks also performed well.

Stock Upgrading, which was allocated 70% to cash and the rest to value stocks (as opposed to the tech growth giants), gained just +1.3%. That’s not ideal but also isn’t unexpected during bear market rallies. If the bear market resumes in the quarters ahead, as we think is likely, this conservative positioning will prove beneficial again, as it has throughout this bear market.

Bond Upgrading

Bond performance has been easy to overlook in recent years, given how dramatic stock returns have been relative to bonds. But with dramatic moves in yields leading to significant bond volatility over the past year, Bond Upgrading has played a key role in protecting SMI member portfolios.

Bond Upgrading beat the Bloomberg Aggregate U.S. Bond Index by a whopping seven percentage points in 2022 during the worst bond bear market in decades (-6.0% vs -13.0%). It got off to a good start this year as well, as its first-quarter gain of +3.6% handily beat the index’s +3.0%. It’s impressive to see Bond Upgrading outperform in both falling and rising markets without missing a beat.

We’ve written recently that bonds were likely to start performing better as investor focus finally turns from inflation to the upcoming recession. That was certainly the case during March, as the bank crisis combined with softer economic data to shift the investing narrative. As we suspected, in that environment, our bond holdings excelled, rising over +3% in March alone. We suspect that is likely to continue as this bear market plays out. Bonds are traditionally great recession performers.

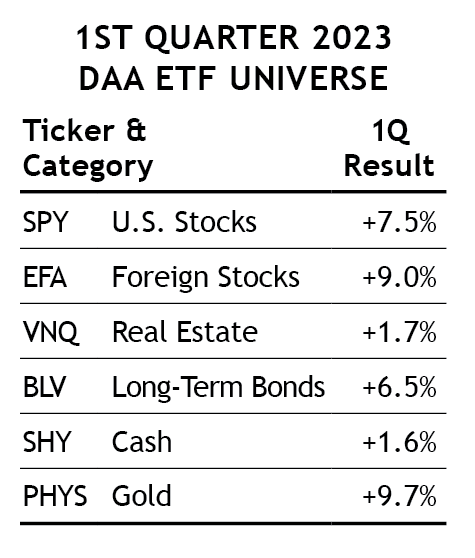

Dynamic Asset Allocation (DAA)

DAA was surprisingly strong during the first quarter, gaining +6.7%. Both last year’s surprisingly poor performance and this year’s better-than-expected result can be partially traced to gold. Last year, despite high inflation and a shooting war in Europe, gold didn’t do much — at least in dollar terms. But since the dollar peaked in October after a strong 2022 rally, it’s been a different story for gold. DAA’s gold allocation gained +9.7% during the first quarter of 2023, bringing its gain since last October to +20.8%.

DAA’s move back into Foreign Stocks last December provides a good reminder of why we follow these strategy signals even when we don’t like what they’re suggesting. Buying foreign stocks just a month after the market’s October lows last year was uncomfortable, but the +9.0% first-quarter gain of DAA’s foreign stock holding played an important role in the strategy’s strong performance.

One final note on DAA: cash is no longer trash! Cash still isn’t going to keep pace when both stocks and bonds rally strongly, but the +1.6% first-quarter return on our cash holdings represented a solid annualized rate.

Sector Rotation (SR)

SR stumbled during the first quarter, following last year’s +18.5% gain. Energy stocks had decent gains going into the March banking crisis, but recession fears pushed energy prices dramatically lower. While the oil price recovered most of its lost ground by the end of March (and would subsequently get a further boost in April from a surprise OPEC+ supply quota cut), the energy stocks in SR didn’t bounce back as quickly. SR was down -10.3% during the first quarter, giving back some of last year’s gains.

50/40/10

This portfolio refers to the specific blend of SMI strategies — 50% DAA, 40% Upgrading, 10% Sector Rotation — discussed in our April 2018 cover article, Higher Returns With Less Risk, Re-Examined. It’s a helpful example of the type of diversified portfolio we encourage most SMI readers to consider.

Given how conservatively positioned this blended portfolio was positioned coming into the quarter (70% cash in Stock Upgrading, with 33% cash and another 33% gold in DAA), its gain of +2.9% was reasonable. That’s an annualized rate of over +11%. Naturally, it didn’t compare favorably with the strong market bounce last quarter, but it still looks quite good when we look back over longer periods that include last year.

Conclusion

The market’s first quarter surge was the fourth significant rally of this bear market. Those who haven’t invested through extended bear markets before (or perhaps have forgotten what it’s like) may be surprised by how powerful these rallies can be — and how much doubt and “fear of missing out” they can create!

Rest assured this is part of the normal bear market process. The 2007-2009 bear market had at least six significant rallies, while the 2000-2002 bear also had at least that many. Much like we’ve experienced over the past 11 months, the 2000-2002 bear market featured a long period in the middle where it seemed perhaps the bear was over — the S&P 500 index was higher in March 2002 than it had been a full year earlier, only to roll over again and drop another -32.7% before the market would bottom seven months later.

From the beginning of this bear market, SMI has provided a pretty good outline of what was ahead (see here and here). Unfortunately, the broader path is always easier to see than the smaller wiggles, which means it takes patience to endure the inevitable bear market rallies that always accompany extended bear markets.

Fortunately, we have good tools to help guide us along the way — our momentum-driven strategy signals. They aren’t designed to catch every bear market rally, but we’re confident they’re going to keep us on the right side of the major trends. That’s what will ultimately determine our success or failure over this entire period. As we’ve discussed numerous times since the start of last year, if we can limit the damage inflicted during bear markets, we’re in a great position to compound our long-term wealth during the longer bull market that inevitably follows. So far, so good!