Soaring energy prices. Relentlessly rising inflation. Slowing economic growth. A stock market coming off a long period of impressive gains, led by a group of seemingly invincible growth giants. To veteran investors, it’s starting to feel like the 1970s again.

With so many emerging similarities, it’s become popular to speculate that the current market could be headed for a repeat of the 1966-1982 period. It’s not as much of a stretch as you might think.

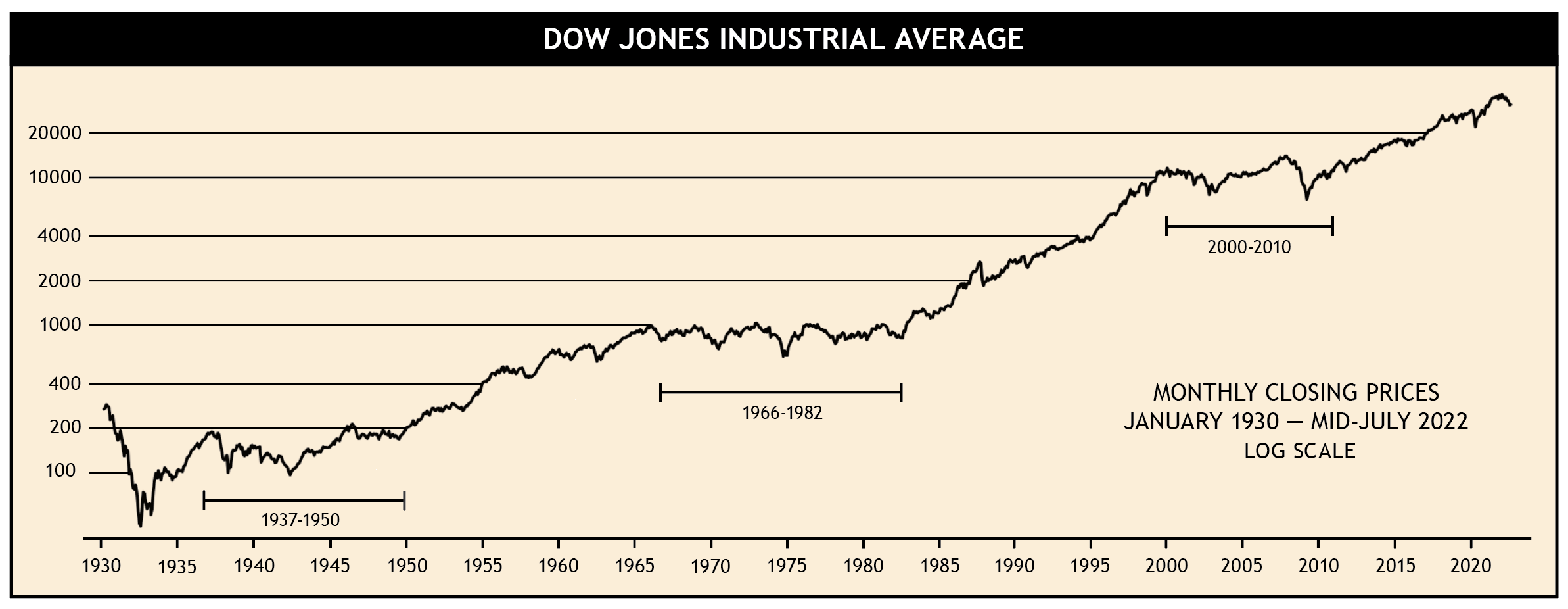

Consider the graph below. It’s a bit different than most stock market charts because it’s a “logarithmic” chart. That means the vertical proportions of the chart stay the same each time the market doubles. In other words, the vertical distance between Dow 100 and 200 is the same as the distance between Dow 10,000 and 20,000. This gives us a clearer view of the true path of the market over the past 92 years. As an investor, the effect on your wealth is the same any time the market doubles, regardless of how many Dow points are involved. But that fact is easily lost in most charts where the huge number of points gained since 1982 tends to obscure all of the market’s movements prior to that point.

Click Graph to Enlarge

The chart shows that over the last 90-plus years, the market moved through several distinct bull, bear, and sideways periods, and that each was quite prolonged at times. The most dramatic bull markets are easily spotted (1950-66, 1982-2000, and 2009-2021) as are the major bear markets which began in 1929, 1973, 2000, and 2007.

But between the prolonged market advances are uncomfortably long periods where the stock market just flattened out. That’s not to say there weren’t significant gains and losses within those “flat” periods. The 1966-1982 period, for example, contained four separate bull markets with each gaining 32%-75%, as well as five bear markets with losses of 24%-45% each. But at the end of all this activity, 16 years went by with the Dow ending at the same level it started. The same is true of the 2000-2010 period, with two major bear markets of -50%, yet a total return that was roughly flat.

These “secular bear markets,” as these lengthy flat periods are sometimes called, are a scary proposition for investors to consider. They call into question the validity of buy-and-hold investing, and really do a number on the idea of passively investing in index funds. But consider them you must. With the appearance of the 2000-2010 version, these long, flat periods aren’t ancient history. Many SMI members invested through that period. They’re as vivid a part of the historical record as the bull markets connecting them.

Thankfully, accepting the existence of these secular bear markets isn’t the same thing as worrying about them. Two key questions should dictate your attitude towards these market plateaus.

How long is your investing time frame?

A 40-year-old investor should react differently than a 60-year-old investor to the prospect of a decade (or more) of flat market returns. The retiree or near-retiree would view this as a more threatening event due to their shorter investing time horizons. The younger worker, on the other hand, should ideally view a flat market as a tremendous opportunity to load up on shares at reasonable prices.

Upon closer examination, a flat market of several years may not be as dire a threat as it first appears even for investors about to retire. These days a realistic retirement time frame usually extends at least 20 years into the future, maybe more. That’s long enough to work through an extended flat market and still derive some benefit at the other end. Those already in retirement when such periods arrive are more at risk, though they’ve likely had the benefit of a long bull market during their peak earning years. Most importantly, as we’ll see next, there are still ways to prosper even if the market indexes flatline for a decade or more.Are you indexing or following SMI’s active strategies?

This is the key to the whole discussion. It’s clear that a strategy tied to the movement of the broad market will be unsuccessful if the broad market is stagnant for an extended period of time. The legion of investors who have piled into index funds over the past dozen years, and who are dutifully staying put at the advice of the financial services industry, could be sorely disappointed. Cruelly, the market offers just enough rallies to sustain one’s optimism. But an index fund can only mirror the performance of its underlying index, meaning all indexers — including, to a slightly lesser extent, those following SMI’s Just-the-Basics strategy — can only hope to tread water until such sideways periods end.

The scenario is brighter for those using SMI’s active strategies. While the market as a whole may be zigging, there are always parts of the market that are zagging. We’ve seen that during this year’s decline, as the mid-year review discusses. (SMI Premium-level members can also watch a video discussion of the year’s first half and how the SMI strategies fared.)

The market is fickle and changes its affections for companies of different sizes and styles regularly. The 1970s, which many are worried we’re about to repeat, present a good illustration. The decade began with all attention focused on the “Nifty 50” — a strong advance by the market’s largest, mostly growth-oriented, stocks (similar to the FAANG leaders of the past decade: Facebook, Apple, Amazon, Netflix, Google). By the latter part of the decade, the situation had reversed, with these same darlings completely out of favor and a strong rally in small-company stocks underway. Yet the Dow started and ended the decade in basically the same place, completely masking these powerful undercurrents.

SMI’s Upgrading and Sector Rotation strategies exploit these shifts within the markets (in somewhat different ways), capitalizing on each new trend as it emerges. The Dynamic Asset Allocation strategy also rides the market’s ebbs and flows between varying asset classes, some of which (such as gold and real estate) outperformed stocks during the inflationary 1970s.

Although SMI wasn’t around during the 1970s, we saw many of these dynamics come into play during the last sideways period from 2000-2010. While the broad stock market was largely flat (the Wilshire 5000 index had a total return of -1.7% for the decade ended 12/31/2009), SMI’s Stock Upgrading strategy gained +85.0% during that decade. That happened without the defensive protocols that have since been added to the Upgrading process, and which have been so valuable so far this year. Clearly, Upgraders (and users of the other SMI actively managed strategies) have much less to fear from “secular bear markets” or market plateaus than those whose investment returns are tied to the market indexes. In fact, it’s pretty easy to argue Upgraders don’t have much to fear from these sustained plateaus at all.

Circling back to the original question of whether the current market will repeat the 1966-1982 experience, nobody knows. But even if it does, maintain perspective. Look again at the graph above. Imagine you’re an investor in 1967 (or 2001), but you have the ability to see the rest of the chart. So you know that after several years of relatively flat action the market will begin a long bull market advance. Would you be frightened, or elated? Retirees would have mixed feelings, but younger investors would be excited! In fact, they likely would want to accumulate as many shares as possible during those “flat” years — when prices would remain relatively steady — in anticipation of the huge bull market to come.

That doesn’t necessarily translate into going out and buying shares today. We still think that by remaining patient today we’re likely to have an opportunity to buy at even better prices later. But extending our gaze to these longer market cycles helps us realize that our efforts to preserve capital during bear markets (such as we’re in today) and carefully grow it during the long plateau seasons (should we be starting one), put us in position to profit greatly when the next secular bull market begins.