An SMI tenet is that investing decisions should flow from — and be consistent with — a specific investment strategy (or strategies) you have chosen.

For some people, selecting a strategy can be daunting. This overview should help.

SMI offers three “core” strategies designed with the average person in mind. These strategies (two available to Basic-level members, another to Premium members) are easy to understand and relatively simple to implement. But they require different levels of involvement and self-control.

Let’s compare what each strategy demands — and what you can expect in return.

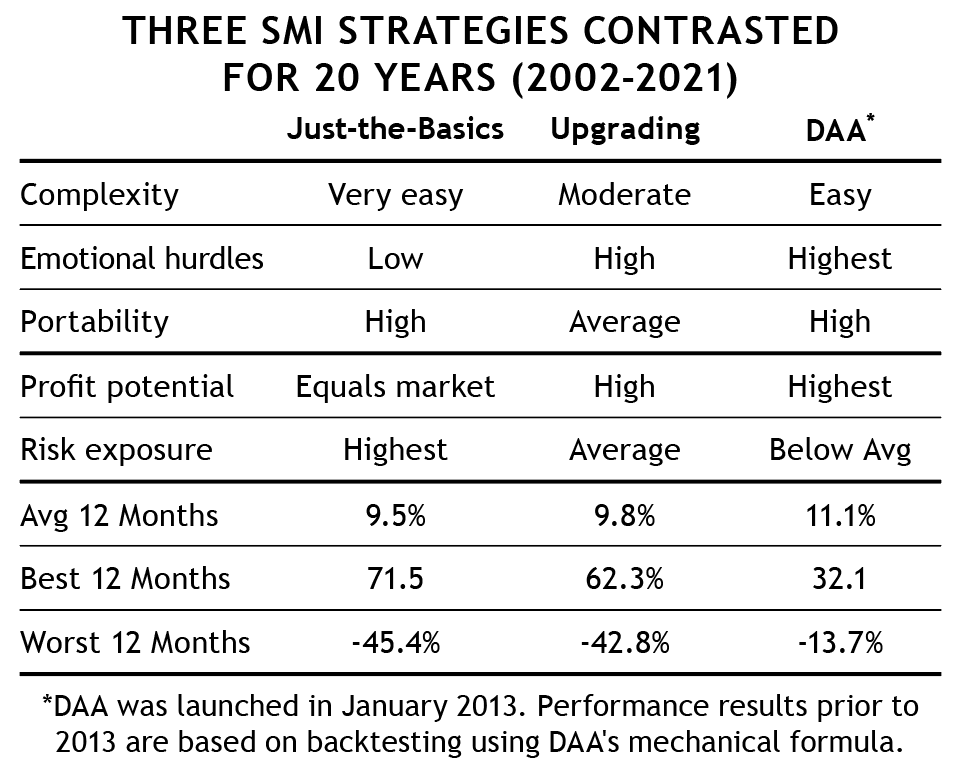

Complexity.

Just-the-Basics: If you believe the simpler, the better, select JtB. It’s easy to set up, and your only housekeeping chore is the annual rebalancing task every January.

Fund Upgrading: You get specific buy/sell instructions each month. Following those instructions won’t take more than 15-20 minutes (once you have done it a time or two).

Dynamic Asset Allocation: DAA requires monthly attention, but there are only three holdings (out of a possible six) at any one time. Occasionally, you’ll be told to sell one and invest the proceeds in another.

Emotional hurdles.

Just-the-Basics: It doesn’t help to have a great strategy if you don’t have the self-discipline to follow the rules. With JtB, since there is never a need to replace any of your funds, you can’t go wrong.

Upgrading: You’ll have to be ready to replace one or more of your holdings regularly. In practice, it doesn’t happen monthly, but it could. When told to sell a fund, people often hesitate to follow through. Maybe it’s because they have a loss in that fund, or they discover there’s going to be a redemption fee. With Upgrading, procrastination can be tempting — and costly.

DAA: The instructions are easy to understand, but there’s room for operator error if you decide to do your own thing. Most often, this will be because you are required to sell something at a loss to move on from a trade that didn’t work out. Overcoming this tendency to wait for a turnaround is key to minimizing your losses.

Portability (i.e., the ability to implement a particular SMI strategy where you already have your accounts).

Just-the-Basics: Even if you don’t have a Vanguard account, this approach is flexible because most brokers, fund organizations, and 401(k) plans offer similar index funds.

Upgrading is also quite portable. It can be implemented anywhere you have access to a large number of actively managed funds, such as in an IRA. On the other hand, not all 401(k)plans will offer such a variety (but even then, SMI’s Personal Portfolio Tracker can help you maximize your options).

DAA: This strategy can be implemented easily in most accounts, but it’s not a great option for 401(k) plans unless your plan offers a brokerage window that allows you to buy the ETFs of your choice.

Profit potential and risk.

Just-the-Basics: This approach will perform much the same as the overall market. If stocks rocket up so will your returns. In a bear market, the only downside protection is your portfolio’s bond allocation (as dictated by your optimal asset allocation).

Upgrading: Because it rotates among the top-performing active managers, Upgrading offers a high profit potential and average risk exposure.

DAA: From the nearby table, you can see this strategy has the best profit potential over time, as well as the lowest risk exposure. It accomplishes those excellent long-term results primarily by limiting losses in bad markets rather than turning in huge gains during good ones.

There’s no single strategy that’s best for everyone. In fact, we generally believe a combined strategy approach is best for most investors. But whichever your preference, you are more likely to progress financially if you invest according to a specific, proven plan.