Recently, SMI's Upgrading and DAA strategies recommended moving to "cash" for some positions.

"Cash" is a catch-all term for options such as money-market funds (MMFs) and cash-oriented ETFs. There are less liquid forms of cash too, including Treasury obligations and brokered CDs. (Outside of a brokerage account, options range from bank savings accounts and corporate "demand notes" offered by large companies such as Ford, GM, and Caterpillar.)

Typically, the best options to use within SMI strategies are money-market funds. MMFs, which are a type of mutual fund, are posting attractive yields at present, plus they can purchased easily and sold at any time without penalty.

Here is an overview of what's available at SMI's recommended brokers.

Fidelity

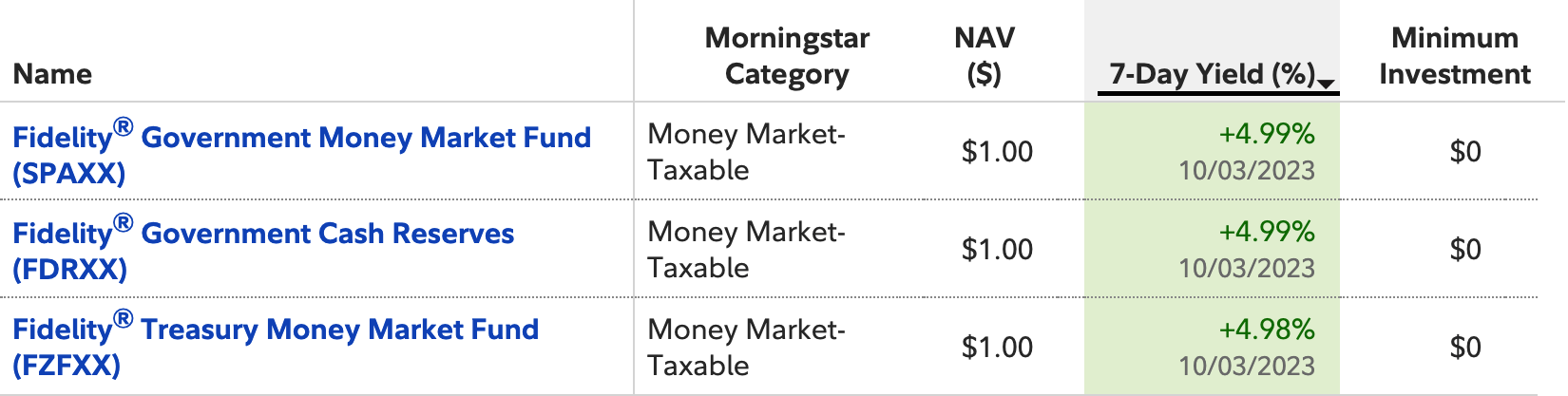

Fidelity offers 11 in-house MMFs, both taxable and non-taxable (see a full list here). Even better, investors can designate a money-market fund as the default option for "uninvested cash" or — as Fidelity calls it — the "core position."

SPAXX (Fidelity Government Money Market Fund) is available as a core position fund for any Fidelity investor. Some accounts also have access to FDRXX (Fidelity Government Cash Reserves). Non-retirement account holders have one other option: FZFXX (Fidelity Treasury Money Market Fund).

As of yesterday (10/03), all three funds had similar "7-day yields" (i.e., a projection of what an MMF would yield over one year based on its income distributions over the past 7 days):

Choosing an MMF as one's core position fund makes "going to cash" as simple as selling a holding and then leaving the proceeds in the default account. (It also simplifies redeploying your cash back into an equity fund when the time comes.) However, if you would prefer to keep your core position separate from any cash you're holding for DAA or Upgrading, you can invest the proceeds in a different Fidelity MMF.

If you're not sure which fund you're currently using for your core position, log in to Fidelity, select "Accounts & Trade," and then "Account Positions." Click your core position and you should see the fund name. You'll also see an option to "Change Core Position." (If you prefer, a Fidelity rep can make the change for you — call 800-544-6666.)

In addition to the MMF options described above, Fidelity offers other core position options. For retirement accounts, there's an FDIC-insured bank sweep that currently pays 2.72% APR. For non-retirement accounts, there's the Taxable Interest Bearing Cash Option (FCASH), currently paying 2.69%. But there is no reason to choose either of those when Fidelity's MMFs are offering better yields.

Schwab

Unlike Fidelity, Schwab doesn’t allow an MMF to be selected as a default option for sweep money. At Schwab, the default options for cash (for most customers) are" 1) An FDIC-insured "Bank Sweep" that deposits money in interest-bearing deposit accounts with Schwab-affiliated banks or 2) an SIPC-insured "Schwab One Interest" account. Both presently pay a scant 0.45%.

Contrast that with SWVXX (Schwab Value Advantage Money Fund), which has a 7-day yield of 5.24% (through 10/03).

To use SWVXX or any other Schwab money market fund, you have to make a fund purchase, as with any other mutual fund. From Schwab's Trade screen, choose "Mutual Funds" (or use an "All-in-One Trade Ticket") and enter SWVXX (or the fund you prefer) in the symbol field. Choose "Buy" and enter the dollar amount you wish to purchase.

Schwab's money market funds are listed here. Select an "investor shares" fund (unless you're investing $1 million or more!).

E-Trade

In contrast to Fidelity and Schwab, which offer only in-house MMFs, E-Trade offers taxable and non-taxable money-market funds from many companies, including Federated Hermes, American Century, and (E-Trade owner) Morgan Stanley. Vanguard MMFs are available, too (minimum investment: $3,000).

Currently, about 20 of the taxable funds available via E-Trade have 7-day yields above 5.00%. You can research all of E-Trade’s MMF offerings here (use the "Fund Category" option in the left column and choose "Money Market" from the dropdown menu.)

Note: If you're an E-Trade investor, you may want to get in the habit of regularly transferring any uninvested cash to an MMF because E-Trade is among the worst-paying brokers for cash-sweep money. Despite interest rates being at their highest level in years, E-Trade still pays a paltry 0.10% on cash holdings of less than $500,000.

Firstrade

Think of Firstrade as the brokerage equivalent of a "no-frills airline." It may be cheaper than the other guys, but the trade-off is limited service and irritating inconveniences. Here's a great example: Firstrade offers no money-market funds. None. Nada. Zilch.

Therefore, Firstrade customers who wish to "go to cash" will need to select an ETF option. An appropriate one is TBIL (US Treasury 3 Month Bill ETF). That fund is yielding 3.73% YTD (total price return through 10/02). TBIL is available via Firstrade commission-free.

Vanguard

Vanguard investors have a sweet arrangement when it comes to "going to cash." VMFXX (Vanguard Federal Money Market Fund) — with a current 7-day yield of 5.30% — is the default "settlement fund" for Vanguard account holders.

Of course, if you prefer to keep your "SMI strategy cash" separate from "uninvested cash," you can employ a different Vanguard money market fund. The company's MMF offerings and current rates are shown here.

Note: For non-retirement accounts, Vanguard recently rolled out the FDIC-insured Vanguard Cash Plus Account, currently yielding 4.70%. At this point, the Cash Plus Account is not available to all customers.