Asset classes once thought of as “alternative” have been moving steadily into the mainstream — a quiet but significant investing trend of recent decades. The influence of that trend is apparent in the SMI model portfolios, which today include once-alternative asset classes such as real estate and commodities.

In this excerpt from The Allocator’s Edge, investment manager Phil Huber argues that many of today’s alternatives will become mainstream too — an evolution he believes is both necessary and beneficial.

Editor’s Note: This month’s cover article is more technical than SMI’s typical content, but Phil Huber makes such important points we wanted you to read these ideas straight from him. The big picture idea is that the conventional “60-40” stock/bond portfolio isn’t going to be sufficient in the years ahead. Today’s starting points all but guarantee that: Equities are historically expensive and bond yields are already low. That’s the polar opposite starting point from 40 years ago when stocks were historically undervalued and bond yields were sky-high. Further, trends that powered the success of 60-40 portfolios over recent decades (disinflation, falling interest rates, rising globalization, “peace dividend,” etc.) are reversing before our eyes.

|

For as long as I can remember, I have been fascinated — nay, obsessed with — asset allocation. I know what you’re thinking — this guy needs more hobbies. And you’d be right, but that’s neither here nor there...

My infatuation with asset allocation stems from my strong conviction that diversification — true diversification — is indistinguishable from magic. I mean, think about it. To put different investment ingredients together in a blender and have the resulting smoothie taste great and be less filling than the sum of the parts?

The direct parallels between asset allocation and our everyday lives captivate me. Whether in markets or in life, we continually walk a tightrope of trade-offs in the decisions that we make. Want to be physically fit? You need to balance the trade-offs between a healthy diet and exercise against your desire to watch TV and eat the things you enjoy. Want to have a successful career? You need to balance the trade-offs of a higher salary and recognition from your peers against your willingness to work long hours and spend time away from your loved ones.

This brings us to the myriad trade-offs we must make as investors: return objectives, risk tolerance, income needs, liquidity preferences, tax considerations, and so on and so forth. The deeper you go, the more you realize that it’s trade-offs all the way down.

For the last several decades, traditional asset allocation techniques have proved sufficient in helping investors achieve their most important financial goals. It is my belief that while the conventional core building blocks of portfolios — stocks and bonds — will still be necessary going forward, they are no longer sufficient.

To that end, I have spent an inordinate amount of time over the last decade-plus of my career researching modern approaches to asset allocation and leading-edge portfolio construction techniques. I believe that most investors have historically been limited in terms of the types of diversification they can access, but that is changing.

The road to success in this new era will not be paved with the familiar and comfortable. It is no secret that old habits die hard. But excellence in asset allocation

requires a continuous evolution of ideas. We now live in an era where alternatives can stand on equal footing with stocks and bonds as a third pillar of diversified portfolios. The evidence and rationale are too compelling to ignore.

A two-asset world

Most investors live in a two-asset world. You want the prospect of high returns with commensurate risk? Buy stocks. You want safety and income with the accompanying lower expected returns? Buy bonds. Find yourself stuck somewhere in the middle? Buy some combination of the two. It is impossible to pinpoint exactly when and how it happened, but somewhere along the way, the specific combination of 60% stocks and 40% bonds became the de facto standard in asset allocation.

The last 30-plus years have been defined by a secular decline in interest rates, providing a once-in-a-generation tailwind for fixed-income investors coming off the heels of the inflationary environment of the 1970s. Or, as writer Morgan Housel puts it, “The most underrated investing traits are patience and having your career coincide with a 30-year record decline in interest rates.”

There’s good news and there is bad news. Let’s just rip off the Band-Aid and get the bad news out of the way first. There is a high probability that the 60/40 portfolio that worked tremendously in the past will ultimately fall short in meeting the return targets and objectives of investors in the decades ahead. There are two main culprits to blame here: high valuations of the “60” and paltry interest rates on the “40.”

Let’s start with equities. There is a wealth of evidence supporting the notion that starting valuations matter a great deal to long-term returns. The mean-reverting nature of valuations links high starting multiples with lower-than-average returns. And vice versa. For U.S.-domiciled investors with an embedded home bias, this challenge is particularly acute as our domestic stock market ranges from slightly rich to obscenely expensive, depending on your preferred valuation metric.

This tells you nothing about what might happen in the next year or two, as valuations alone are a blunt timing tool. But it certainly doesn’t paint a pretty picture for the next seven to 10 years. The story in international markets is not nearly as bad, but market multiples of earnings abroad are by no means a screaming buy.

Let’s move on to fixed income now. As of March 2021, the 10-year Treasury rate sits at around 1.5%. That is materially higher than the low of 0.52% reached in 2020, but still historically low. Assuming realized inflation of roughly 2%, investors are set up for negative expected “real” (after inflation) returns from an asset that has historically acted as ballast against equity volatility and generated mid-single-digit returns in the process.

One doesn’t have to make an interest rate forecast to confidently declare that the halcyon days of fixed income are all but over.

The result of these two forces colliding is dramatically lower expected real returns for traditional 60/40 portfolios. According to investment management firm AQR, the expected medium-term real returns for a U.S. 60/40 portfolio is a measly 1.4% — less than one-third of its long-term average since 1900.

Don’t get me wrong. I think almost all investors should own stocks. I also think most investors should own some bonds. These core portfolio pillars are not going away anytime soon and both serve valuable roles in a portfolio. But we can do better. The goal is not to replace stocks and bonds, but to augment them.

Three choices

With conventional portfolios stuck between a rock and a hard place, allocators can choose one of three paths to confront today’s challenges:

Do Nothing

This is the path of least resistance. And it is likely the road that most will take, as inertia is a force to be reckoned with. Maintaining the status quo will feel comfortable, but the price of admission for that comfort will come in the form of falling short of investors’ objectives. Return targets are unreasonably high, yet capital market expectations are stubbornly low. When you have that combination, something’s got to give.Take More Equity Risk

This choice might solve the return side of the equation but requires a very long horizon and will incur some bumps along the way. Investors will likely have to incur cringe-worthy levels of volatility and drawdowns that will keep them from sleeping well at night. And we must remember the equity risk premium is promised to no one — that’s why it’s a risk premium. History has demonstrated several lengthy dry spells. In theory, this approach might work. In practice, the odds are slim.Think and Act Differently

Investing differently than others is easier said than done. Choosing this path takes courage, but it is where the opportunity lies ahead.

The opportunity

What do I mean when I say we need to think and act differently? I promised there was good news as well. A net positive for investors is that the investable universe has grown by leaps and bounds, providing a more diverse toolkit with which to build portfolios.

The solution to the dilemma facing traditional asset allocation is to embrace additional sources of return that lie outside the conventional stock-bond orthodoxy. A wide range of exposures once considered un-investable are now increasingly democratized thanks to the confluence of technological advancements and financial innovation. From niche asset classes to strategies designed to intelligently exploit structural market inefficiencies and behavioral biases, investors today can enhance their portfolios by including valuable, diversifying return streams sourced from non-traditional risk categories.

The effective implementation of alternative investments in the context of a diversified portfolio is the biggest opportunity — and the biggest challenge — facing financial advisors, asset allocators and other sophisticated investors today.

The only constant is change

Our ability to give alternatives a role in all portfolios today exists because of our evolved understanding of the drivers of risk and return, and our increased knowledge of what types of asset classes and strategies work over time.

This ability also exists because innovation and technology have allowed for: lower barriers to entry for historically hard-to-access alternatives; more liquid and systematic approaches that aim to deliver the beta of once alpha-driven categories at a lower cost; and more investor-friendly vehicles. [“Beta” is how volatile an investment is compared to the overall stock market. “Alpha” measures an investment manager’s ability to outperform a market index. – MB]

We’re getting smarter

Investors a century ago lacked the data, analysis, technology, and insights we have at our fingertips today. In many respects, investors of yesteryear were feeling around in the dark.

Fast forward to today’s world and a lot of the heavy lifting has been done for us. Researchers and practitioners are continually “articulating, extracting, and assembling investment risk” for use in portfolios. This is akin to the centuries-long (and still ongoing) process undertaken by scientists to identify the chemical elements that make up our physical universe.

It’s easy to get lulled into thinking that all 118 chemical elements were created or discovered at the same time, but the periodic table of elements has undergone expansion over time, supporting innovation and embracing change. In the early 18th century, the rich and colorful table we know today would be barely recognizable with only 13 discovered elements in 1718. The late 18th and early 19th centuries saw a flurry of new elements added to the mix, with a total count of 53 by 1825. An early version of the periodic table we’re all familiar with today surfaced in the 1860s and counted 63 listed elements at the time. As the science of chemistry became more formalized and our knowledge of atoms, protons, neutrons, and electrons deepened, the periodic table rounded itself out. As recently as 2016, four new elements were added.

The periodic table of investment assets

The investable universe is far vaster than most investors realize. If we took the average investor’s perception of the investable universe and translated that into a periodic table, it would likely resemble one of the early iterations from centuries ago rather than the reality of today.

Markets are continually evolving, which means our methods and techniques for harnessing them and capturing their rewards need to adapt as well. As the investable universe continues to expand, failing to take advantage of the opportunities offered is likely to result in portfolios that are inefficient, overly concentrated, or both.

Imagine how limited our understanding of the world would be if chemists had stopped at 63 elements in the 1860s. Is it likely we’ll discover another 100 elements or another 100 asset classes? Probably not. But we should always keep pushing the frontier further west in search of a better tomorrow.

The codification of investment returns

The building blocks that comprise risk and return have been largely codified thanks to our enhanced ability to process enormous amounts of data, and then examine, analyze, and interpret historical results. Long ago, before the influence of academia and the proliferation of reams of historical data for us to dissect, investing was an art. Competition was scarce and few investors possessed the skills to understand companies and their pricing to make good investments.

Harry Markowitz advanced our understanding of the concepts of risk and diversification in the context of maximizing returns. In the 1952 paper “Portfolio Selection,” Markowitz wrote: “Investors diversify because they are concerned with risk as well as return. Variance came to mind as a measure of risk.”

Enter Professors Eugene Fama and Kenneth French. These two gentlemen — one at the University of Chicago and the other at Dartmouth — compared the expected returns of stocks to the expected return of the market, as well as company size and value (as measured by book-to-price). According to their analysis of these factors, the premiums associated with smaller companies and those with higher book-to-price multiples went a long way in explaining the cross-section of expected stock returns.

Following Fama and French’s seminal work, it was off to the races in the asset management industry to develop and market products that fit neatly into this framework. In 1992 the now ubiquitous nine-square grid known as the Morningstar Style Box™ was unveiled, allowing investors and advisors to analyze the investment style of stock funds.

While the asset management industry continued to slice and dice fund mandates to meet allocators’ ever-growing need for precision, academics continued their quest to identify and translate the drivers of expected returns across and within assets. Subsequent attempts to improve on the Fama-French Three-Factor model (i.e., size, value, and expected return) include the addition of momentum (1993) and profitability (2013). Thus, there were then five factors to take into account. Soon, we would have a veritable Factor Zoo with researchers finding over 400 patterns in historical data. The clear majority of these would prove to be nothing more than noise.

The continued decomposition of risk and return led to a transformation in how we look at portfolios, moving away from an asset-class mindset toward a factor-based approach. While asset classes provided convenient labels, factors brought us closer to the essence of what was driving returns. As Andrew Ang of BlackRock notes, factors are to asset classes what nutrients are to food.

As allocators increasingly spoke the language of factors, the industry adapted. The Morningstar Style Box™ benefited from being recognizable to even the most novice of investors.

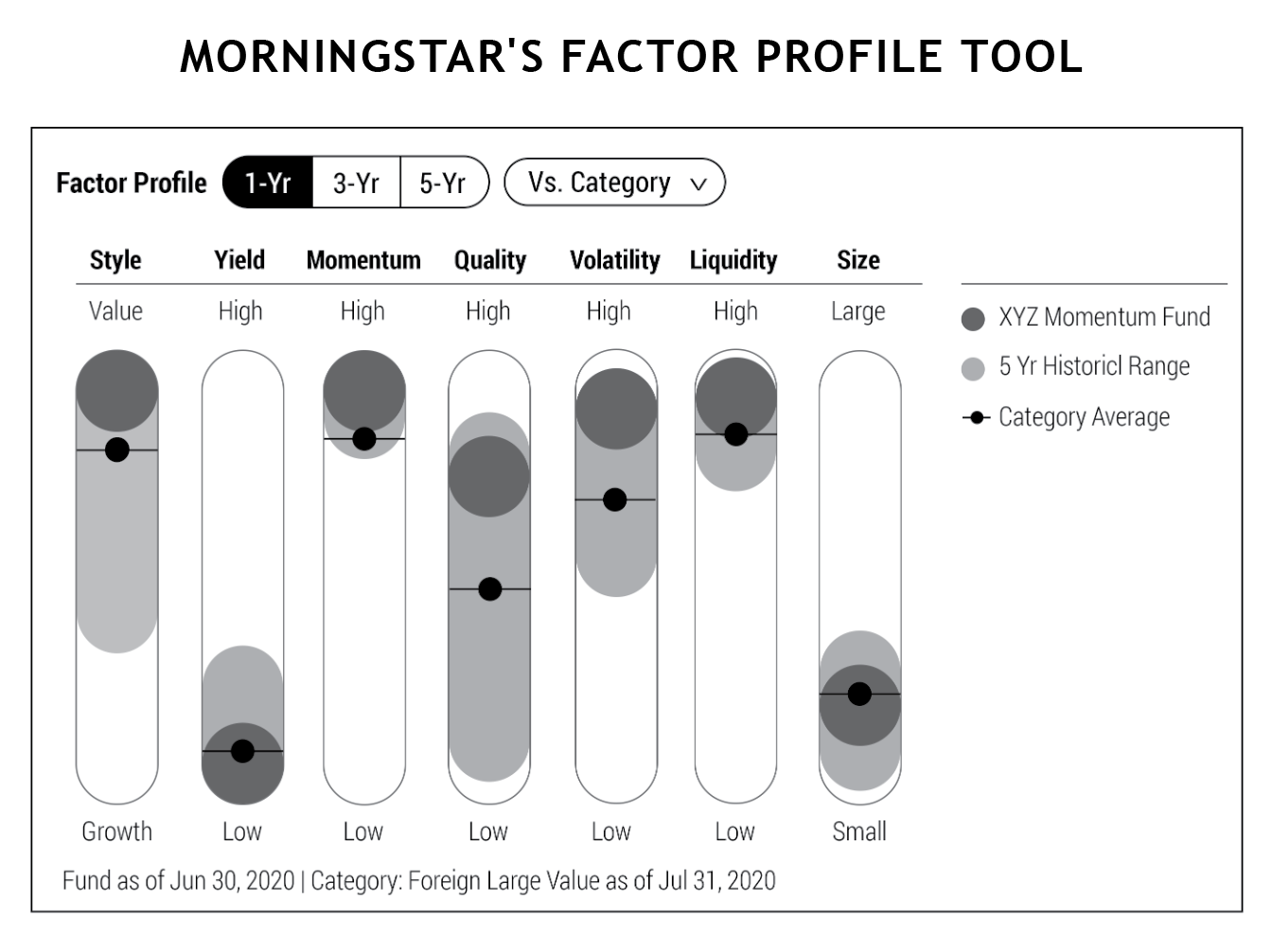

But Morningstar realized that its two dimensions did not tell the full story and in late 2019 introduced a Factor Profile tool — adding volatility and liquidity to raise the number of factors to seven — as a complement to further explain an equity fund’s exposure to sources of return (see image at right).

Perhaps signaling the mainstream arrival of liquid alternative betas is the fact that they now have their own style box, much like that of stocks and bonds. Admittedly simplistic, measuring correlation and volatility relative to global stocks, it at least serves as a foundation to be built upon-much like the original Style Box at its inception in the early 90s.

Markets and portfolios adapt to changing conditions

Our perception of what is considered “alternative” evolves over time as investment strategies become more widely adopted and institutionalized and subsequently less... alternative.

What do REITs, high-yield bonds, and emerging markets have in common? They were all once considered alternative.

REITs [real estate investment trusts] were established in 1960 by U.S. government regulation aimed at facilitating real estate investment for the average investor. By the end of 2019, there were 179 REITs with over $1 trillion in combined market value. Nobody on Main Street knew what a junk bond was until they were made infamous by Michael Milken and Drexel Burnham Lambert in the 1980s. Despite the bad press at the time, few investors today would bat an eye at high-yield credit as a strategic component of a fixed-income portfolio.

The first emerging markets fund appeared in 1987 from Franklin Templeton. Fast forward to today, and other allocators might look at you sideways if you don’t have a dedicated EM allocation. And finally, we have Bitcoin. Barely 12 years old and this asset class created out of thin air went from “phony internet money’’ used for illicit activity to a bona fide institutional-grade asset class.

The regulatory landscape also plays a critical role in shaping asset management trends. The environment following the Great Financial Crisis made it increasingly uneconomical and onerous for financial institutions to hold certain types of risk on their balance sheets. This meant less supply per unit of demand, leaving a gap to be filled by asset managers. This dynamic has brought forth a handful of rewarded risks, once concentrated on the balance sheets of large financial institutions, toward being distributed more evenly across the balance sheets of millions of individual investors. These risk premiums, previously held captive by financial incumbents via bank lending, trading activities, and insurance underwriting, are now increasingly accessible to investors through innovative fund structures.

[As for] the growth of private markets... even Vanguard — the public face of index investing — has announced plans to offer private equity strategies.

As financial innovation flourishes, we continually push new boundaries both in the discovery of novel asset classes and strategies, and the unlocking and democratizing of investments to benefit more people. Technological advancements, academic insights and the tireless efforts of industry practitioners all contribute to a future for investors that allows more opportunities to diversify, removes frictions, lowers costs, and improves access and fairness.