In celebration of SMI’s 30th anniversary, we’re highlighting some of the core beliefs and principles that guide our work. We often highlight specific diversification ideas, but this month we want to pull back and take a broader view: why do we diversify a portfolio in the first place?

Most investors would like to be invested in the top-performing market segment year-after-year. In pursuit of this goal, many chase performance by continually shifting their portfolios toward what’s hot. For example, as Large/Growth companies — such as Facebook, Amazon, and Apple — have outperformed recently, investors have piled into the funds and indexes that highlight these stocks.

A common problem with this kind of “performance chasing” is that many investors get into a hot segment just as it is about to cool off! As that segment falls from favor, those investors experience a lot of volatility in their concentrated portfolios and end up with poor relative returns. Disappointed, they jump to the next hot segment and repeat the cycle.

While there’s a place for emphasizing what’s currently working in the market within your portfolio (all of SMI’s active strategies contain an element of this “momentum” approach), it’s crucial to do that from within a diversified framework.

Diversification ensures that some of your money will always be in the best-performing segment. Of course, some will be in other segments as well, including those that aren’t so hot at the moment. While that may not be as exciting as loading up on the “latest and greatest,” diversification provides a less risky and more even-keeled way to make your money grow over time.

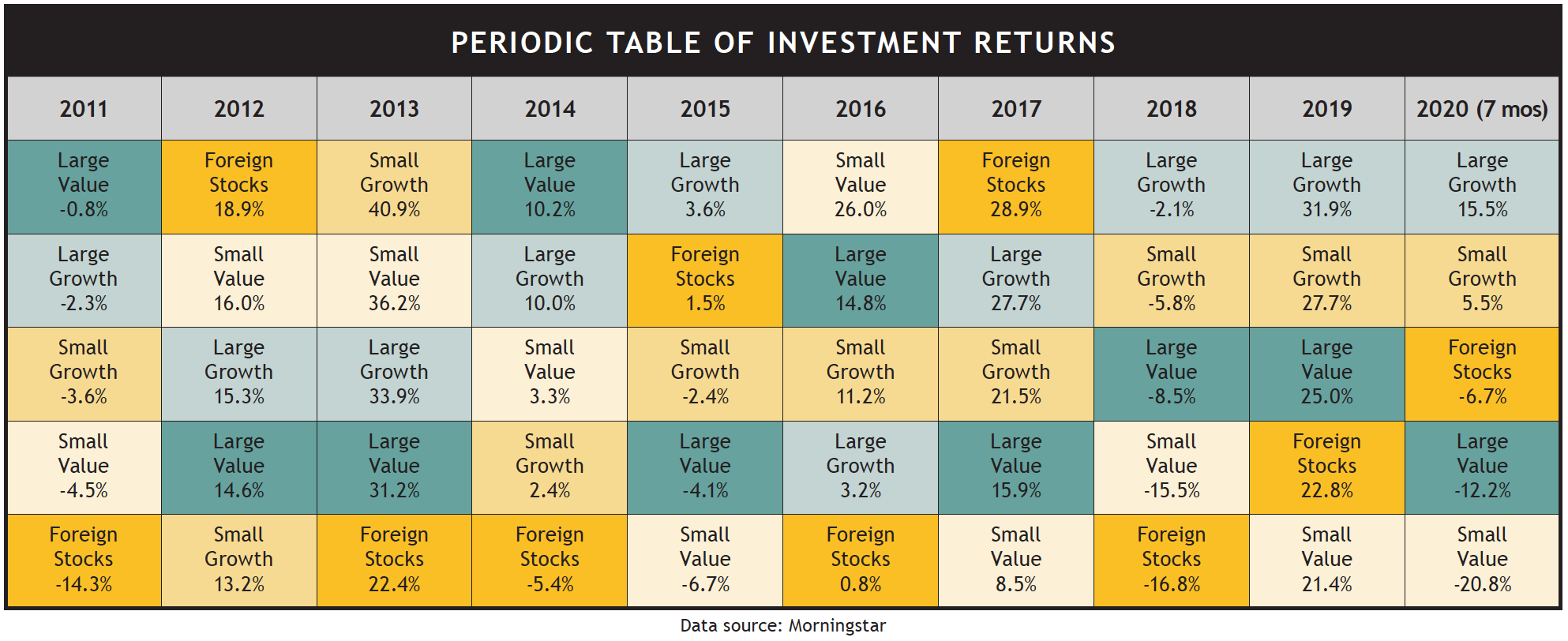

Reviewing a decade of performance

The chart below is a variation of the “Periodic Table of Investment Returns.” We’ve modified the table to include only the five major stock-risk categories tracked by SMI’s Stock Upgrading strategy. The columns show the year-by-year average returns for all the mutual funds in each of those five categories, with the best-performing category at the top and the worst at the bottom.

The first column is a summary of 2011 — not a great year for investors. In the top square, you’ll see that the best performer — Large/Value funds — lost -0.8% that year. Each subsequent square below shows the returns for another risk category. The bottom-dweller in 2011 was the Foreign funds category, posting a loss of -14.3%.

Click Table to Enlarge

The table layout makes it easy to see how each category has fared relative to the others over the past decade (or nearly a decade). The colors help you visually track a particular category from year to year.

As you can see, each market segment has gone through years of strength and years of weakness. Each of the five enjoyed at least one year as the top performer, but three of the five also spent time at the bottom.

Further, the chart illustrates how a segment’s relative performance can be volatile from one year to the next. An example is the relative performance of the Small/Value and Foreign categories. In 2015, Small/Value funds were the worst performers, while Foreign funds were second best. In 2016, this reversed strongly, with Small/Value taking the top spot, Foreign the bottom spot, and Small/Value outperforming Foreign by a whopping 25 percentage points! Then in 2017, the script had flipped yet again: Foreign was back on top, Small/Value was the worst, and this time Foreign was winning by about 20 percentage points.

There is such a thing as a free lunch

When a particular market segment is hot, many investors understandably are enticed by the performance numbers. Diversification seems dull by comparison and not as lucrative. So they shift their holdings to what’s hot, only to later suffer the consequences of being overly concentrated in a particular slice of the market when that slice falls out of favor.

The better path for most investors is to spread their money more broadly across the primary market segments. Yes, this ensures your overall portfolio result won’t match the hottest performer’s returns in any given year, but it also guarantees you’ll never miss out on participating to some degree in each year’s hot area.

The real beauty of diversification is that it produces long-term returns similar to the individual risk categories while smoothing out volatility along the way. This muting of sharp ups and downs is crucial. It helps protect you from the most dangerous obstacle you face as an investor — your own emotions.

So the next time you’re tempted to load up on a particular investment type (or wonder if it’s really necessary to own funds in all five SMI risk categories), remember the periodic table of investment returns and the diversification lessons it holds.

Diversification is often called “the only free lunch in investing.” That’s because it costs virtually nothing to diversify, yet diversification yields great benefits — namely, a reduction in portfolio volatility plus a degree of protection from overall losses. At the same time, you get to enjoy having at least some of your money invested in the market’s top-performing segment year-in and year-out.