The United States of America remains the center of the investing universe. However, recent changes to the international world order raise questions about the degree to which this will continue.

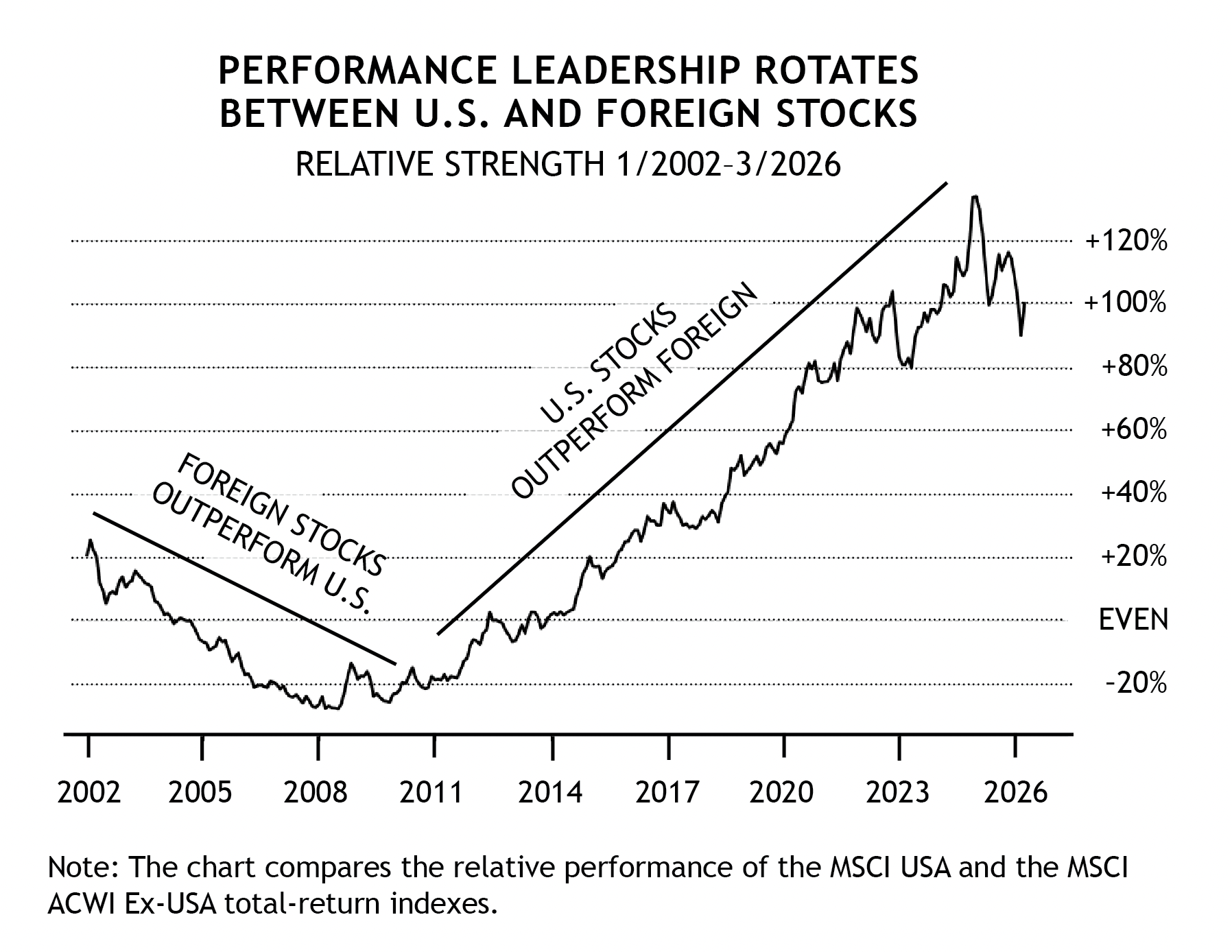

U.S. stocks have outperformed their international peers by a wide margin since the 2008 Global Financial Crisis, but this dynamic has reversed since the start of the Trump presidency, a trend that could persist if foreign investors allocate more capital toward their home markets.

The economy of the United States remains the largest and strongest in the world. The U.S. is blessed with abundant natural resources, relative political stability, a large and educated workforce, and a culture of entrepreneurship. Indeed, these are the primary elements that helped make the 20th century the American century. No nation has ever dominated the world’s economic landscape as the U.S. has for the past 100 years.

America’s financial markets have also long been the envy of the world. Backstopped by a reliable rule of law and a regulatory system generally favorable to investors and business, the U.S. stock and bond markets have attracted massive amounts of foreign investment. The size and scope of the U.S. Treasury market, coupled with the U.S. Dollar’s unique position as the global reserve currency, has made the U.S. bond market unique — no other bond market offers the type of trading depth and liquidity that massive pools of capital and other nations rely on for their regular transactions. And over the past decade or so, the appeal of America’s largest technology stocks has captured the imagination of investors around the world, attracting trillions of dollars of foreign capital into U.S. stocks.

But as America’s role as global leader shifts, largely voluntarily, back toward history’s normal condition of a multi-polar world, there are real questions about the willingness, or even ability, of foreigners to keep funneling capital into U.S. markets. The “Tariff Tantrum” of 2025 and most recently the impact of the Iran War on U.S. relationships with our allies in Europe and the Middle East are raising real questions about whether foreign governments and investors will need/want to shift some of the capital currently parked in U.S. assets back home. We’ve already seen isolated examples of large international asset managers publicly selling some of their investment in U.S. assets, and it’s not difficult to understand how the foreign perception of being overweight U.S. tech stocks may have shifted from savvy to unpopular.

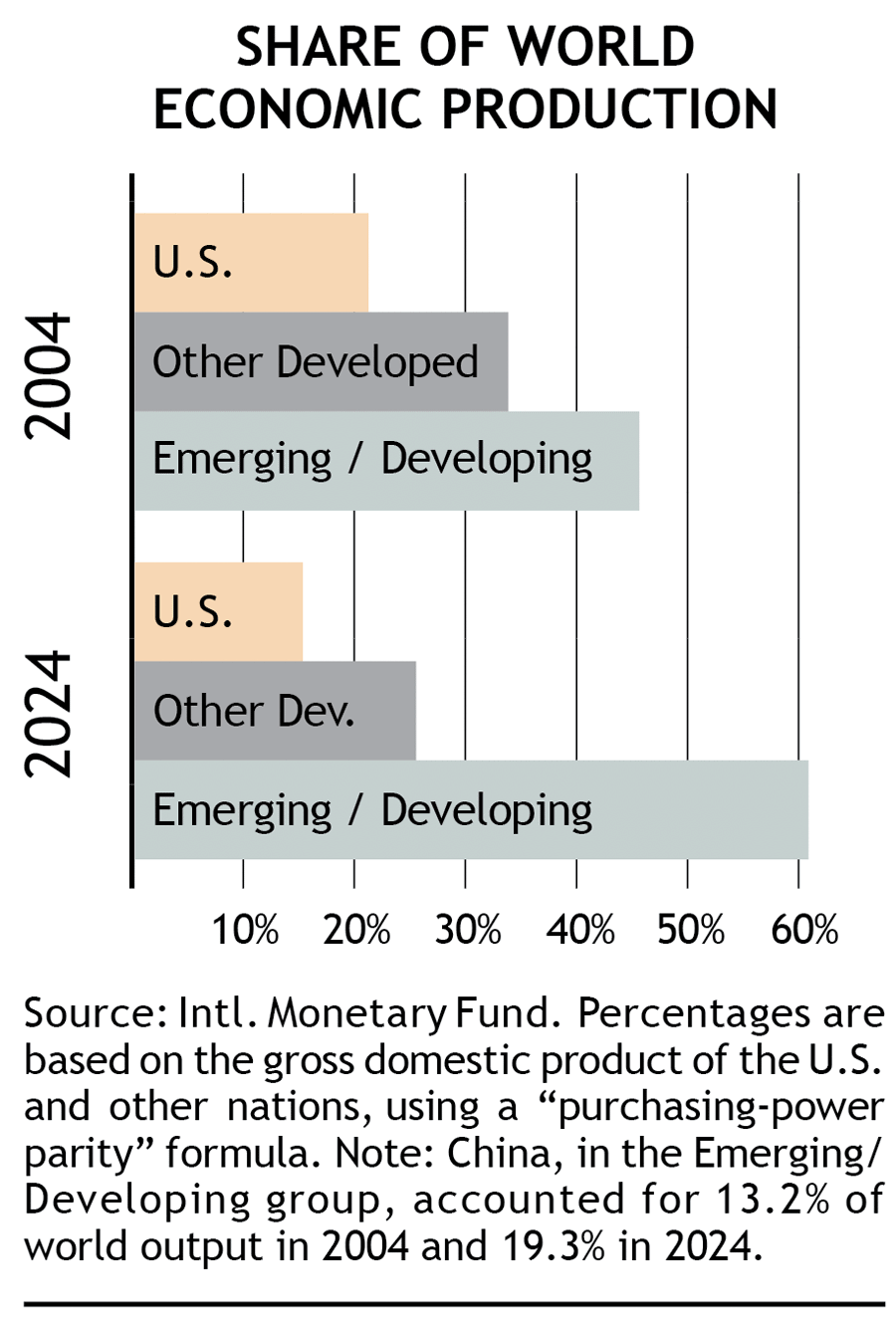

While it’s an open question how much of that may occur, or how quickly, what’s indisputable is that the conditions of the past few decades have created a huge imbalance in terms of America’s share of global financial assets relative to our share of global economic production. Consider this: As of early 2026, the total value of almost all of the stock shares in the world — i.e., “global market capitalization” — was about $109 trillion, according to the research firm MSCI. U.S.-based stocks represented a bit less than 64% of that amount. That’s four times greater than all of Europe, the Middle East, and Africa combined.

As the chart nearby shows, this share of financial assets is totally disproportionate to the U.S. share of economic production, which is closer to 15% (after accounting for the strength of the U.S. dollar in “purchasing power parity” terms, which we’ll get to shortly).

Make no mistake, there’s nothing that says a country’s share of financial markets has to equal its share of actual economic production. But there is a big difference between a 64% share of stock market assets and 15% of economic production. As we’ll see shortly, investor preferences for foreign vs. domestic stocks ebb and flow. It’s very possible that global preference for U.S. stocks is near a high point. The significant realignment currently underway in global economic, military, and trade could be a catalyst to tip these percentages back in favor of the rest of the world for a time.

Diversification + opportunity

Everything we’ve discussed so far has been primarily through the lens of U.S. assets being at risk to an outflow (or even just slower inflow) of foreign capital. But as a U.S. investor, there’s another side to this coin — the current opportunity presented by participating in foreign markets.

As the “Share of World Economic Production” chart shows, an increasing proportion of global industry has shifted to so-called “developing” economies. For example, stock shares in “emerging markets” — including India, Mexico, South Korea, and Brazil — now account for more than 10% of global stock value. It’s a safe bet that most Americans have nowhere near 10% of their stock portfolios invested in emerging markets. Their home bias means they’re potentially missing opportunities.

For many years, the primary reason for owning foreign stocks was to provide additional diversification. In the distant past, U.S. and Foreign stock markets used to move somewhat independently of each other. However, this has greatly diminished over the past 30 years or so. While the degree of correlation still ebbs and flows, U.S. and foreign markets tend to move directionally together more often than not these days. So it really comes down to which markets are moving faster in whatever direction they are all traveling in.

This makes sense, given that the world economy has become so interconnected. There is also much less of a distinction between the economies of the U.S. and the so-called “developed” and “developing” countries. Finally, technology has lowered or removed many of the barriers that used to restrict the flow of money across national boundaries.

Today, the pure diversification argument in favor of owning foreign stocks has largely given way to a different benefit: foreign stocks offer broader growth opportunities than investing exclusively in U.S. companies. With such a huge proportion of global economic activity happening outside of the U.S. economy, and with the entire global order in the process of being reset before our eyes, it’s important for us to be aware of these foreign opportunities.

Fluctuating dollar implications

Before moving on, it’s worth addressing the important impact of the dollar on the returns of foreign investments to U.S. investors. Because most Americans earn and spend exclusively in dollars, we tend to be insulated from — and not even notice — fluctuations in its value relative to other currencies. But this matters a lot in evaluating foreign investment returns.

To illustrate, let’s walk through a real-life example from last year. Let’s say that on Jan. 1, you invested $1,000 in the German stock market.1 First, your U.S. money was converted to euros. On the day you made your purchase, one euro could be exchanged for about $1.04 in U.S. money — or, stated another way, one U.S. dollar was worth .966 euros. So your $1,000 became 966 euros that were then invested in German stocks on the Frankfurt stock exchange.

After six months passed, you were able to sell your German holdings for 1,154 euros — a tidy +19.5% profit. Well done! After the sale, you converted your euros back into dollars. Fortunately (for you), the euro had gained against the dollar over those 6 months — a euro was worth about $1.18...rather than $1.04. That means your 1,154 euros converted to $1,361.

Rather than enjoying a 19.5% profit, you actually gained 36%! You not only made money on the growth of your German investments, you nearly doubled your earnings because of the relative weakness of the dollar during the span you were invested. So, as you can see, a 10% increase in the value of the euro against the U.S. dollar makes the same profit contribution to an American investor with holdings in German stocks as if the German market itself had risen 10%.

The big takeaway is this: A weaker dollar is a net negative with respect to overall U.S. purchasing power, but it boosts the profitability of an investor’s foreign holdings. That was the case during the first half of 2025 when the dollar fell 10% relative to a basket of foreign currencies. Correspondingly, returns to U.S. investors in foreign stocks were outstanding during this period. A weaker dollar makes U.S. manufacturers more competitive globally, so given President Trump’s focus on "re-shoring" American manufacturing, it’s reasonable to assume the Administration will favor weak dollar policies (including lowering U.S. interest rates).

Getting your money out there

Mutual-fund and ETF investors have four main types of international funds from which to choose (we list each type separately in our monthly Fund Performance Rankings — available online to all SMI web members):

World funds have the greatest latitude — they can invest around the globe, anywhere they find attractive opportunities. This means that many of these funds actually have substantial U.S. holdings. So if you invest in a world fund, you can’t be sure how much of your money will end up abroad. When our Stock Upgrading portfolio recommends an international fund, we want that money in foreign stocks, so we don’t recommend world funds for this purpose, as they may have heavy U.S. holdings.

Foreign funds, which are what we typically recommend in the Situational group in Stock Upgrading, invest almost exclusively outside the U.S. Normally, these funds are the place to look if you want to invest across a number of countries through a single fund. (It’s up to each fund whether to set limits on how large a percentage of assets can be invested in any single nation or region.) With a foreign fund, you don’t have to call the shots about which countries and companies to invest in. Instead, you rely on the expertise of a fund manager who makes decisions about the most promising areas of the world, outside the U.S., at any given time.

SMI’s Dynamic Asset Allocation strategy uses an exchange-traded foreign fund (ETF) with the ticker symbol SCHF for its international stock exposure. SCHF is an index fund, designed to track the well-known FTSE Developed Ex-U.S. index (Canada, U.K., Europe, Australasia and Far East). This index covers all of the developed markets besides the U.S., but does not provide exposure to the so-called emerging markets, discussed below.

Regional funds, as the name suggests, narrow the geographical focus even more by investing in a particular region of the world (Europe, Asia, Latin America) or even a specific country (China, Japan, Canada). As such, regional funds tend to have greater volatility than funds with more geographically diversified holdings.

Emerging markets: a growing power on the world economic stage

The fourth type of international fund concentrates its investing in “emerging markets.” Although the term doesn’t have a strict definition, when it first started being used widely, it generally referred to 20+ nations in various parts of the world experiencing significant levels of economic development and reform. Twenty to thirty years ago, there was a vast gulf between the economies and societies of these countries and those of the so-called “developed” nations. Today, that gap is much less distinct.

The huge populations and growth potential of China and India make them the center of any emerging markets discussion. The largest Emerging Markets ETF allocates 22% to China and 12.6% to India. Surprisingly though, South Korea (17%) and Taiwan (23%) have large weights in these indexes as a result of the importance of their semiconductor industries. Brazil (5%), South Africa (3%), Saudi Arabia (2.8%), and Mexico (2%) are the other large allocations, with smaller positions in another dozen countries included as well.

As with the rest of the international investing narrative, the emerging markets story has changed over the decades. It’s still true that emerging market economies tend to be correlated more closely to their commodity exports. However, it used to be that emerging markets were compelling because they were rising from a relatively low base of development in comparison with advanced economies, so they held significant growth potential. Today it’s hard to argue that a country like South Korea is vastly different from its “developed” market peers in Europe or North America, yet the long-standing labels have remained in place.

And while many emerging market countries have modernized dramatically in recent decades, there’s still a huge growth story there as billions of people move up the economic ladder out of poverty and add electricity, heating/cooling, vehicles, and everything else we associate with modern life in the west. The sheer numbers of people aspiring to live as we do — complete with developing infrastructure, improved education, and a growing middle class — make the emerging markets a compelling growth story.

One of the big risks to investing in emerging markets in the past has been significant volatility, driven by large money flows that come and go. While this has improved in recent decades, many emerging markets still have a relatively small investor base within the country itself, so they simply aren’t large enough to take it in stride when huge sums of money from outside investors suddenly pour into the country in search of profit opportunities — and then often retreat just as quickly.

The “demographics is destiny” angle clearly favors the emerging markets over the older developed ones. America is in better shape demographically than many developed markets (such as Japan and much of Europe), but even here we face massive headwinds given our current debt levels and rapidly aging population.

Contrast the U.S. or European situation with that of India and other emerging markets where the labor force is young, deep and still relatively cheap. Economic growth can be boiled down to two factors: growth in labor force productivity and the size of the working-age population. Given these dynamics, it’s no surprise that the share of economic output has been steadily shifting from developed countries to emerging markets in recent decades, as shown by the chart shown earlier.

A quick word about China

China’s role as an investment avenue is hotly debated. While China’s economic story has been incredible, that hasn’t always translated to its financial markets. Generally speaking, the long-term performance of Chinese stocks hasn’t been very good, despite enormous economic growth. Despite this, many investors remain interested simply because there are a large number of Chinese companies that are outstanding at what they do and their growth potential seems vast.

However, given China’s unique form of state-directed capitalism, there are also real concerns about the degree to which investing in Chinese companies aids their government in achieving goals contrary to the values of most SMI readers. But even apart from that, SMI thinks the risks of investing in China outweigh the potential rewards. Especially after watching Russia get financially canceled following its Ukraine invasion in 2022, it doesn’t seem worth the risk that someday we could wake up to find our investments in Chinese stocks similarly frozen following an invasion of Taiwan, or otherwise winding up at odds with the U.S. It seems clear, the U.S. and China are engaged in a great powers conflict that is unlikely to resolve anytime soon, so we prefer to just sidestep the issue. There are plenty of other attractive places to make money.

To that end, SMI’s Dynamic Asset Allocation strategy allocates to Emerging Markets when momentum dictates that we should. However, when we do, DAA uses the Emerging Markets Ex-China (EMXC) ETF for that exposure.

Pendulum swing: A compelling international opportunity?

Over the past several decades, performance leadership has passed back and forth between U.S. and international stocks. These swings often last quite a while. In SMI’s January 2024 cover article, titled Uncomfortable Regime Shifts, we included a Bank of America chart showing this history back to 1950, which clearly showed U.S. stocks outperforming significantly during the “Nifty Fifty” era of the 1960s, foreign stocks outperforming for most of the 1970s and ‘80s, U.S. stocks taking the lead for the 1990s, and foreign retaking it in the early 2000s. But the degree of U.S. stock dominance relative to foreign stock since the end of Global Financial Crisis in 2009 has been unprecedented.

As the chart below shows, U.S. stocks have outperformed their foreign counterparts by a massive margin over the past 15 years or so. In fact, from June 2008 through the end of 2024, U.S. stocks gained 495% while the rest of global equities gained just 76%. While foreign stocks have outperformed U.S. by a 35% to 19% margin since the start of 2025, you can see that has barely begun to correct the huge imbalance built up since the GFC in 2008. (For context, the “Even” line, which we are still roughly 100% above, is the historical balancing line between U.S. and foreign stocks since 1950!)

Getting international exposure into your portfolio

While it’s difficult to pinpoint the exact percentage of a portfolio that should be in international assets, the right answer for most U.S. investors is likely “more.” Fortunately, SMI members already have a reasonable level of foreign stock and bond exposure.

Dynamic Asset Allocation allocates one-sixth (16.7%) of its portfolio to international stocks when their momentum warrants inclusion. This can either be all in developed foreign markets (SCHF) or split between SCHF and emerging markets ex-China (EMXC), as is currently the case.

In addition, the SMI 3Fourteen REAL Asset Allocation ETF (RAA), which comprises the other half of DAA’s portfolio, can invest as much as 30% of its portfolio in foreign stocks and another 10% in foreign bonds. This combined total was 11% of RAA’s portfolio in February of this year. Practically speaking, this meant that another ~5% of DAA’s overall allocation was in international assets, which when added to the 16.7% from SCHF/EMXC, meant roughly 22% of DAA was invested in international assets.

Stock Upgrading allocates to international funds/ETFs when their momentum shows them to be compelling alternatives to U.S. stocks. This has been the case lately, as 20% of Stock Upgrading has been invested in international ETFs. In addition, it’s not unusual for Stock Upgrading to have a few “hidden” percentage points of international exposure among their other holdings. For example, Aegis Value has been a standout holding, gaining over +77% since it was added at the end of March 2025. Digging into its holdings, Aegis’ last reported portfolio was roughly 70% foreign stocks, which means Stock Upgrading was recently 27% international, as opposed to the 20% from the foreign ETFs alone.

Bond Upgrading started allocating to international bonds for the first time in 2026. The Eaton Vance Global Macro Absolute Return fund (EAGMX), which is 25% of Bond Upgrading’s portfolio, currently is about 75% international.

Add it all up and a typical 50% DAA, 40% Upgrading, 10% Sector Rotation blended SMI portfolio would have been allocated roughly 22% to international assets. This would be roughly the same whether or not Bond Upgrading was being utilized within the Upgrading sleeve. (Note: A May fund change with Stock Upgrading will reduce this total from 22% to 18%.)

That’s considerably more than many U.S. investors likely have, though perhaps less than some would suggest given the economic and market disparities noted at the start of this article. While there’s room for this allocation to climb higher via RAA’s allocation or the addition of another foreign fund in Stock Upgrading, readers who desire more foreign exposure can easily boost their allocations to the foreign funds and ETFs SMI recommends within its strategies.

For most SMI readers, though, there’s no need to adjust portfolios based on this article. Foreign stocks look attractive relative to U.S. stocks right now, given their growth potential and cheaper valuations. But SMI readers already have solid exposure to this worthy asset class — and a built-in process to increase or reduce that exposure as market trends dictate.