The cartoon shows a man looking over his retirement-account statement. The caption reads: “According to your latest figures, if you were to retire today, you could live comfortably until 2 p.m. tomorrow.”Accumulating enough money for retirement doesn’t happen by accident! It requires developing and implementing a realistic long-term plan. We hope you’ll be challenged and encouraged as we review proven strategies you can use as you move toward — and into — retirement.

It’s safe to say that most people would like to have a financially secure retirement. Reaching that goal, however, requires careful planning and diligent effort in the years before retirement. Implementing each of the following can help guarantee financial health and stability during your retirement years.

Get completely out of debt by the time you retire, including your home mortgage and any college-related debt you may have incurred for your children. Debt, especially a mortgage payment, will limit your investment options and lifestyle flexibility in retirement.

Maximize your contributions to your company’s retirement plan. Contributing to a personal IRA is a good idea as well, especially if you’re already taking full advantage of any employer-provided matching contributions offered within a company plan.

Fully fund an emergency-savings fund. A robust savings fund provides a means of meeting emergency needs without borrowing and incurring related interest costs.

Investing during retirement

Here is a key question: Which is of greater concern to you — potentially losing principal in the short run or losing purchasing power to inflation over your retirement lifetime?

Some retirees are uncomfortable with the idea of ever losing any of their investment money. This mindset limits them to fixed-income investments, such as bonds, CDs, and savings accounts. But with interest rates at historic lows and with people living longer in retirement, most retirees need to continue investing some of their money in stocks to keep up with inflation. (More about that shortly.)

Of course, retirees should have fixed-income investments too. For the non-stock portion of one’s portfolio, these strategies can increase income without increasing capital risk:

Don’t automatically settle for your local bank’s savings account. Instead, compare local rates to the higher rates available from online-only banks. The difference may be only 0.50%-0.75%, but since retirees often carry large savings balances, even a small percentage difference is worthwhile. Bankrate.com and depositaccounts.com are helpful places to search for higher yields.

Shop nationally for the highest CD rates. Interest rates paid on otherwise comparable certificates of deposit can vary widely. Ignoring this difference is essentially giving up free money. Shop using the websites mentioned above.

Build a CD-savings “ladder.” Longer-term CDs typically pay higher rates than short-term ones. An excellent way to obtain a higher rate without sacrificing liquidity is to build a portfolio of CDs with staggered maturities — e.g., investing in four CDs that mature in six months, one year, 18 months, and 24 months. If you wish, you can extend out as long as five years to get the highest rate (although given today’s low rates, it may be better to keep maturities shorter initially). As each CD matures, use the proceeds to buy the most distant maturity you feel comfortable with.

Buy individual bonds or “Bulletshares.” Under normal conditions, a five-year corporate bond might pay 1%-2% more than a five-year CD. Unfortunately for retirees, that’s not the case right now. The combination of low rates and aggressive intervention by the Fed in the bond market this year means most high-quality corporate debt currently doesn’t yield much more than the best CDs. Other than higher yields, which may return eventually, the advantage of buying individual bonds is that while bond values go up and down as interest rates change (as rates rise, bond prices fall, and vice versa), as long as you hold your bond until it matures, you avoid the risk of loss.

For diversification, consider no-load bond funds. Bond funds buy multiple issues of different types of bonds. Their portfolios can be short-term, intermediate-term, or long-term, and vary in the quality of their holdings. One drawback of investing through bond funds is they never reach maturity, so you can’t avoid a potential loss of principal by merely holding a fund long enough. As a result, you must be emotionally prepared for some fluctuations in principal value.

Weigh the tax consequences. Although municipal bonds pay lower rates, the interest earned is exempt from federal income taxes. Also, municipal bonds issued within your state may save you money on state income taxes. You can invest in municipal bonds directly or via tax-free money-market and bond funds.

A “total return” approach

As noted earlier, a retired investor must weigh the relative importance of two competing concerns. Income-oriented strategies, such as those listed above, address one of those concerns: avoiding losses. But they don’t address the other.

For most retirees, the more pertinent concern is the possibility of exhausting one’s retirement money. The way to address that concern is by constructing a retirement portfolio that will grow with inflation, thus protecting one’s purchasing power and standard of living. In other words, a portfolio that continues to invest in stocks even after retirement.

Aren’t stocks risky, especially for older people? The traditional (and oversimplified) answer is “yes.” Stocks typically are more volatile than bonds. But the uneven performance of the stock market is only one kind of risk. Inflation poses a risk as well — perhaps an even greater one.

Over time, inflation erodes a dollar’s purchasing power. As prices rise, a dollar buys less than before. Consider medical care, a category of particular impact for retirees. In the 30 years from 1990 through 2019, medical care prices rose 206% (increasing about 4% per year on average), according to the U.S. Bureau of Labor Statistics. In dollar terms, a medical-care outlay of $10,000 in 1990 would cost more than $30,000 now!

Given today’s longer lifespans, many retirees could have a retirement that lasts 30+ years. As the past three decades illustrate, the income generated by an initially impressive-looking nest egg will buy less and less over the 30 years ahead — unless you take countermeasures.

We understand that many retirees are cool to the idea of investing in stocks. In addition to their worries about risk, they may think stocks don’t generate enough income, especially with dividends at low levels. They would prefer to “live off the interest” of a fixed-income portfolio and “never touch the principal.” But that isn’t realistic, except for the very wealthy.

For that reason, we suggest that most retirees take a “total return” approach to their income needs. Let’s unpack that. Would you rather own a bond that yields 3% or a combination stock-and-bond portfolio that yields 2%? The bond at 3% seems like the logical choice: earning 3% on a $100,000 bond would generate $3,000 a year. In contrast, the 2% yield on the $100,000 stock/bond portfolio offers only $2,000 in income.

However, the amount of “current income” obtained from a particular investment isn’t the only consideration. Using historical performance as a guide, we can be reasonably confident that the total return (yield plus capital gains) from a stock portfolio will exceed the return from an all-bond portfolio in most years.

What if — thanks to gains in stock holdings — your $100,000 stock-and-bond portfolio grew by 5% ($5,000) during the year? Adding the appreciation of $5,000 to the portfolio’s income of $2,000 would give you a total return of $7,000 — considerably more than the $3,000 return from the bond. (If you needed $3,000 of income to help meet your living expenses, you could withdraw the difference from the stock/bond portfolio, selling stock- or bond-fund shares.)

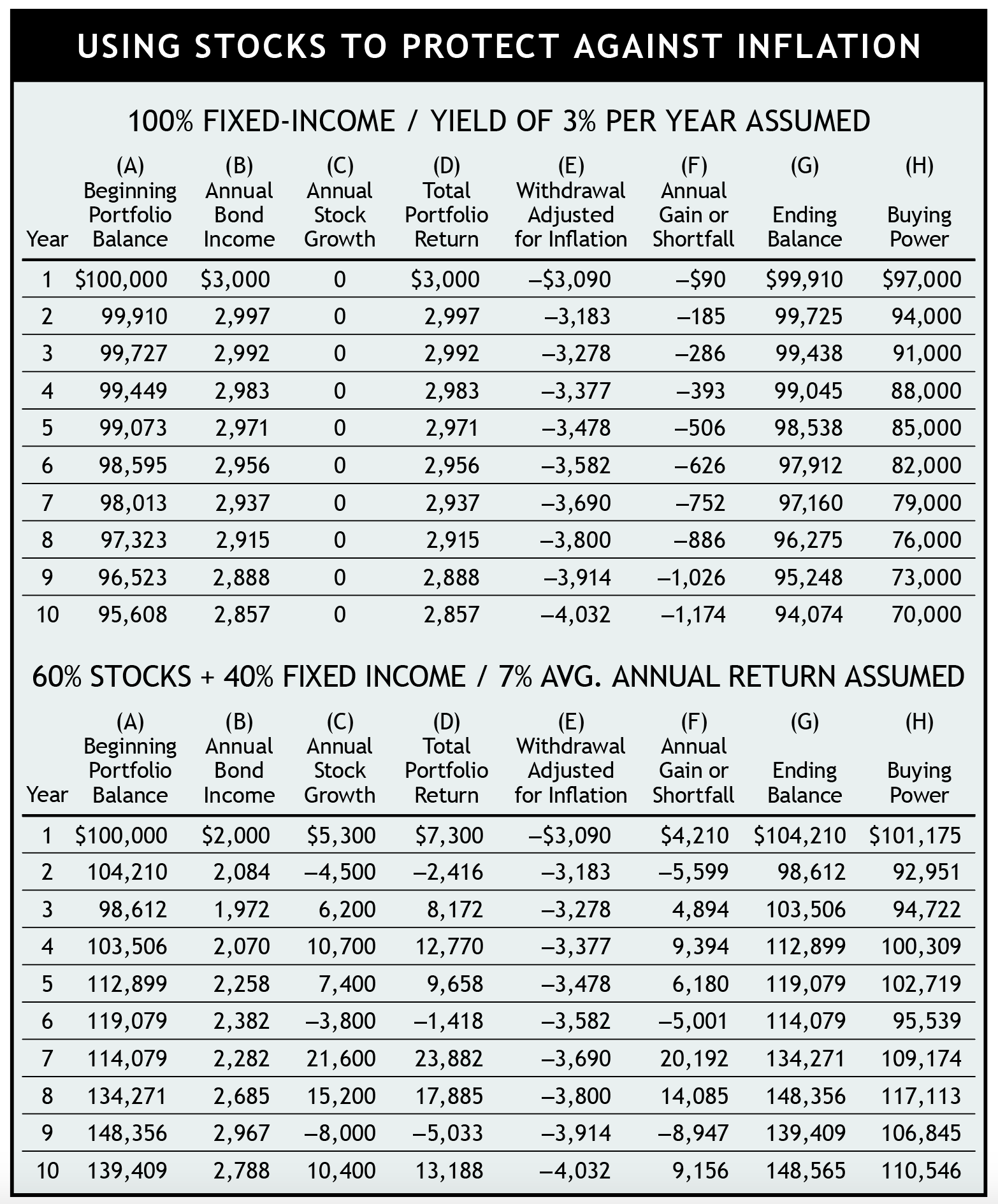

The table below presents two 10-year scenarios. In each case, a retiree makes an annual withdrawal for living expenses. Each year, the withdrawal is adjusted upward to keep pace with a 3% rate of inflation. For example, since $3,000 is withdrawn in the first year, $3,090 would be required at the end of Year 1 to maintain the same purchasing power. (A 3% rate is higher than the official overall U.S. inflation rate of recent years. But as we noted earlier, inflation in certain costs of particular importance to retirees have been higher.)

Click Table to Enlarge

The “fixed income” strategy shown in the top half of the table relies exclusively on bonds and CDs. We’re assuming an average rate of return of 3%. That’s low compared to historical averages but high compared to today’s yields. In other words, we’re choosing something of a “middle ground” figure for our 10-year projection.

Note that this fixed-income strategy falls behind almost immediately. After adjusting for inflation, the first year’s withdrawal (Col. E) is more than the amount earned (Col. D). Therefore, our retiree must sell a small dollar amount of securities (Col. F) to fund the full payout. This leaves less in his account to remain invested in Year 2 (Col. A), which leads to a greater shortfall that year. Again, he must sell securities to fund the payout fully.

The cycle continues, slowly eating into his principal. Further, his “ending balance” (Col. G) in Year 10 doesn’t tell the full story. After adjusting for 3% annual inflation, his purchasing power (Col. H) has been reduced to an even greater extent.

Now let’s look at the “total return” portfolio, consisting of 60% stock funds and 40% bond funds. (We’re using a 60/40 portfolio mix in this example because SMI recommends it for investors with five or less years until retirement, assuming one can emotionally accept the risk — see Table 1 on page 155 in this issue). Returns vary from year to year, but we’ll assume they average 7% per year over the entire decade. Again, this return assumption is lower than the historical average, but reflects the lower growth expectations many analysts have for the stock market in the decade ahead.

The first year all goes well. The retiree’s account goes up in value (Col. G), despite withdrawing $3,090 (Col. E). But stocks take a hit in Year 2 (Col. C), pulling the entire portfolio down. He must sell securities (Col. F) to fund the payout. (The securities sold are selected to maintain the 60%-to-40% balance going into Year 3.) Briefly, the 60/40 portfolio is looking worse than the portfolio using the fixed-income strategy.

But this isn’t a short-term game. Over the long haul — i.e., periods of 10 years and longer — stocks have consistently produced positive results. And that’s what we see as the table progresses, despite three years of setbacks (Year 2, Year 6, and Year 9).

As shown in Col. G, at the end of the 10 years, the stock/bond portfolio is worth $148,565 compared to $94,074 for the fixed-income strategy. More importantly, the 60/40 portfolio has maintained its purchasing power — it’s worth $110,546 in constant dollars. Even after adjusting for inflation, and despite short-term losses, the account had attained a purchasing power 10.5% greater than it had at the beginning of Year 1.

Making withdrawals

Using a stock-and-bond portfolio to provide a stream of regular income needn’t be complicated. Indeed, it can be as simple as telling your brokerage firm to sell enough shares of a particular stock fund or bond fund each quarter to generate a specific dollar amount. Then, by rebalancing your portfolio once a year, you can ensure that your target stock/ bond allocation stays on track despite the periodic withdrawals.

This approach, which runs on autopilot once set up, is attractive in its simplicity. But we understand that some investors may prefer a process that’s more responsive to what’s happening in the markets. Of course, the ideal situation for a retiree generating income from a mixed stock/bond portfolio would be to sell stocks at peaks in the stock market, thus getting top dollar with every sale. But since identifying the market’s absolute high points isn’t realistic, another approach is required.

The key to selling into market strength, and avoiding selling during downturns, is to employ a “bucket” approach to retirement-account withdrawals. As we’ve described before, such a strategy uses a bank money-market account (MMA) in tandem with your stock/bond portfolio. By moving an amount roughly equal to three years worth of quarterly withdrawals into an MMA (in other words, the portion of your living expenses to be funded from investment accounts), you won’t need to sell any long-term investments for income until you’re ready — i.e., when an attractive market opportunity presents itself. (Establishing a four- or five-year fund, if you could afford it, would provide even greater flexibility, although setting so much aside in cash likely would lower your overall long-term rate of return.)

Of course, this idea is workable only if one’s overall portfolio is large enough. If setting aside living expenses in cash reduces one’s stock holdings too much, the remaining holdings may not grow enough to meet future cash needs.

The amount in your MMA would fluctuate between zero and the full three-year amount. During times of poor stock-market performance, you would draw living expenses from your MMA rather than selling any stock holdings. This might last for a year or longer. When the market is doing well, you could sell selected stock holdings and put the proceeds into the MMA, bringing it back to full strength.

Since the stock market tends to have significant peaks and valleys every three-to-four years on average, it would be rare that a retiree would ever need to sell when prices are low. Even if that did become necessary, any such sales would occur once the MMA is exhausted, meaning fewer sales would occur during a downturn than otherwise.

So what exactly constitutes an attractive selling opportunity? Remember, we’re not talking about calling market tops. For the sake of example, consider a retired couple in the mid-1990s whose budget required them to supplement their Social Security and pension income with money from their stock/bond portfolio. In December 1996, former Federal Reserve Chairman Alan Greenspan made his “irrational exuberance” speech, suggesting that stock prices had gotten extraordinarily high.

At that point, our retirees sold some of their stock holdings and built their MMA savings to the maximum level. (Withdrawing a substantial amount of one’s nest egg to fund a “cash bucket” may be emotionally challenging. But having that living-expense money tucked away can help retirees avoid sabotaging their portfolio through panicked selling during bear markets.)

As the market continued higher from 1997-1999, they continued to sell a little from their stock holdings to keep the MMA full. They sacrificed some return late in that bull market by having money parked in savings, but the upside was their MMA was fully funded when the bear market began in early 2000.

Because they had enough savings to cover their living expenses, our retirees didn’t feel any need to sell as prices fell in 2001 and 2002. After two years, their savings account had been reduced substantially, but since they started with three years of reserves, they still had enough to weather another year without selling stocks or bonds. As the market recovered in 2003, they continued to sit tight, further drawing down savings as their stock/bond portfolio regained lost ground.

Our retirees then started to sell a little from their stock/ bond portfolio in 2004 as their MMA savings finally were depleted. An SMI Upgrading portfolio would have recovered to its pre-bear market high mid-way through 2004, so for this couple the bear market seemed like a relatively small bump in the road. As the market continued higher in 2006 and 2007, they refilled their MMA savings by selling from their stock holdings at the higher levels.

With replenished savings, they were in good shape to ride out the bear market of 2008-2009. They spent down their savings until 2011 or 2012, at which point they started selling stocks and bonds again to fill it back up.

While this is just a simple example, you can see that without having to be precise about the turns in the market, a retiree can sell into strength and sit tight during weakness if funds to cover immediate living expenses are available in savings.

Retirees and IRAs

Taxes may be the last thing on your mind as you approach retirement. After all, your income likely will be lower than while you were working, right? Not necessarily. Suppose you retire with significant assets in Traditional IRAs, or in company retirement plans to be rolled over into IRAs upon retirement. The “required minimum distribution” rules that now kick in at age 72 could push you into a higher tax bracket than you expect. Fortunately, there are ways to prepare for this.

One way is to take advantage of a critical distinction between Traditional IRAs and Roth IRAs: With a Roth, there are no mandatory minimum distributions to be taken at any point. The trick then is to convert any Traditional IRAs you may hold (including rollover IRAs from a company retirement plan) into Roth IRAs.

Here, the idea of using a money-market account to stockpile living expenses again comes in handy. This time, as you prepare to retire, you would load the MMA with enough money to cover all living expenses for several years. By not selling any investments the first few years of retirement, and ideally delaying your Social Security retirement benefits, your taxable income should be quite low. You can take advantage of this low income by converting large chunks of your Traditional IRA into a Roth. You’ll have to pay income tax on the converted amounts, but you’ll pay at lower tax rates. (If you don’t convert, you’ll pay the taxes later — perhaps at higher rates — when withdrawing funds from the Traditional IRA.)

What you gain from a Roth conversion is substantial. For starters, money moved to a Roth IRA will grow tax-free as opposed to merely tax-deferred. Further, when required minimum distributions from any remaining Traditional IRAs kick in, they will be smaller, meaning lower taxes and greater flexibility. And finally, if you’ve delayed receiving Social Security retirement benefits during this process, your eventual monthly benefit will be larger.

Naturally, deciding on the best approach to these kinds of retirement preparations requires careful thought. For many near-retirees, paying a qualified CPA or financial planner for advice is money well spent.

Summary

A financially secure retirement doesn’t just happen. Like all worthy goals, it takes planning and managing. If you are not retired yet, a planning weekend with your spouse to discuss what you would like your retirement to look like and what you need to do now to prepare for that kind of retirement lifestyle may be in order. (Many SMI members have found the MoneyGuide software to be helpful in their retirement planning. It’s available to SMI Premium-level members for a one-time $50 fee.)

If you’re in retirement already, ask yourself, “What worries me most about my retirement situation?” If one of the concerns is losing purchasing power, rethink your investment asset-allocation decisions and consider making equities a greater portion of your portfolio. Careful planning and wise investing are crucial to making your retirement years golden.