If you have a college-bound child or grandchild in your life, you may benefit from recent changes in the financial-aid application process. Beginning with the 2017-2018 school year, the federal government’s Free Application for Federal Student Aid (FAFSA) is available three months earlier than in the past, and the financial information required by the form will pertain to an earlier period than before.

Those arcane-sounding changes yield important benefits for many parents and grandparents.

Earlier application availability

FAFSA is the primary form that determines if your student qualifies for any need-based aid, including federal grants and loans, state and school scholarships, and college work-study programs. All college students, regardless of their family’s income, are encouraged to complete the form.

In the past, the FAFSA was made available beginning in January of the year a student intended to attend school. For example, under the old rules, a student who intended to take part in the 2017-2018 school year could have completed the FAFSA no earlier than January of 2017. Under the new rules, that same student could have completed the form as early as October 1, 2016.

There were two problems with the old rules. First, in January few people had their completed tax information for the just-ended prior year. Estimates often were used, which had to be revised later. Second, by January, many students had already applied to their schools of choice, but couldn’t yet submit the FAFSA information needed for schools to make financial-aid decisions. Making the FAFSA available three months earlier is designed tomake the application process more efficient, while giving students more time to apply for, receive, and consider various financial-aid offers.

Note: The new timing does not reflect a new deadline for completing the FAFSA — only earlier availability. Still, it’s important to take advantage of this because some financial aid is provided on a first-come, first-awarded basis.

New tax-year information used

The other change to the FAFSA pertains to which year’s financial information is required on the form. In the past, it was the immediate prior year’s information. Under the old rules, a student planning to attend school in the 2017-2018 school year had their financial aid eligibility based on their (and their family’s) 2016 financial information.

Under the new rules, the required financial information is from two years prior. (In the government’s vernacular, this is the prior-prior year.) So, for students planning to attend the 2017-2018 school year, their FAFSA now requires 2015 financial information.

This change not only will eliminate the time-consuming process of updating a FAFSA once tax information is in hand, it should speed up the process of completing the online application the first time. Under the new rules, since a family’s taxes for the “prior prior” year already have been filed by the time the FAFSA is available, applicants should be able to use the online IRS Data Retrieval Tool (IRS DRT) to import much of the required information electronically from the IRS database. (The online FAFSA makes this easy with a few mouse clicks.)

Special benefit for grandparents

This second change to the FAFSA — using the tax information from two years prior rather than one year — will have an important positive impact on grandparents’ ability to contribute to their grandchildren’s college costs without negatively impacting the student’s financial-aid package.

According to the rules for parent-owned 529-plan accounts, withdrawals are not treated as income to the student. In contrast, withdrawals from grandparent-owned 529-plan accounts, are added to the student’s income in the year the transfer is made. Half of such “income” is included in the formula for the federally determined Expected Family Contribution toward college costs. The net effect has been that money from grandparents (if given from a 529 plan) would reduce the student’s financial-aid package.

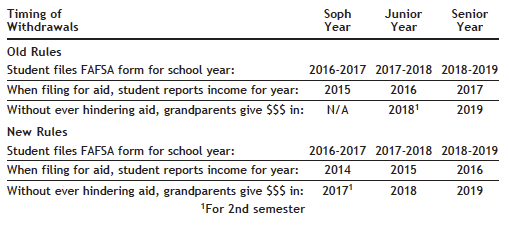

For an example of how the new guidelines might change aid eligibility, see the table below. Under the old rules, money withdrawn from a grandparent’s 529-plan account in 2018 could be used to help pay for the second half of the student’s 2017-2018 school year without negatively impacting that school year’s financial aid. That’s because the student would report his/her 2016 income on the FAFSA form when applying for aid, and 2016 was unaffected by the 529 money.

Later, when the student filed for aid for the 2018-2019 year, he/she would report income for 2017, also a year when income was unaffected by the grandparents’ 529 withdrawal. That’s why, under the previous FAFSA rules in which prior-year financial data was required, grandparents typically were advised to hold off on any 529-plan withdrawals until the calendar year in which their grandchild would begin his or her final year of college.

Under the new rules, in which prior-prior year financial information is required, grandparents can make 529-plan withdrawals starting a year earlier — the calendar year when their grandchild begins his or her junior year (2017 in the example in the table) — without negatively affecting their subsequent financial aid. From a FAFSA perspective, 529 money given in 2017 now won’t affect financial aid awarded until the 2019-2020 school year, but the student would have graduated in June of 2019, so any impact on 2019-2020 financial aid would be irrelevant. This means grandparents’ can now contribute to two and a half years’ of their grandchild’s college costs (the second half of their grandchild’s sophomore year and all of their junior and senior years) without negatively impacting the student’s other financial aid.

These FAFSA rule changes are just the latest example of the increased complexity involved in paying for college. Given the ever-rising college price tag, it’s never been more important to understand such rules and to take advantage of them.