The stock market is celebrating today's PPI (Producer Price Index) larger-than-expected decline, a day after yesterday's better-known CPI (Consumer Price Index) also showed that inflation is finally slowing.

Be careful what you wish for.

Yes, it's good news that inflation is finally cracking, even if yesterday's year-over-year 5% inflation rate is still more than double the Fed's target of 2%. But it's not great that falling demand and a slowing economy are the factors driving it lower. Predictable, but still not great.

I would say that at this point everyone seems to be aware that a recession is coming, except that isn't quite true. Treasury Secretary Janet Yellen, the White House, and apparently, The Economist still don't see it.

Pretty much everyone else has come around to that point of view though, as the economic data is painting a fairly clear picture. There's been a notable slowdown from January to February to March, and the pace of the slowdown appears to have accelerated during the last few weeks.

Stock market investors also seem to be in the recession-denial camp, although I think for many it's more a case of misunderstanding the sequence of events than an expectation that we'll actually avoid a recession. I've seen quite a bit of confusion on this point, so it's worth quickly going through.

For most of the last year, the thing stock investors have pined for is the Fed to stop hiking interest rates. The reasoning is simple: a pause in rate hikes leads to rate cuts, and over the past decade, rate cuts have meant the stock market races higher. So this week's soft inflation data has reignited hope that this process will commence once again.

The problem with that thinking is it misses the difference between recessionary bear markets and other times when the Fed has cut interest rates. SMI's January 2023 cover article, From Inflation to Recession: The Outlook for a Continuing Bear Market in 2023, explored this in detail.

Analysis that lumps all the times the Fed has paused/pivoted from hiking interest rates and spits out stock market average performance following misses this important nuance. It doesn't help that the one example of a Fed pivot that most investors remember — 2019 — was a non-recession example when the market soared after.

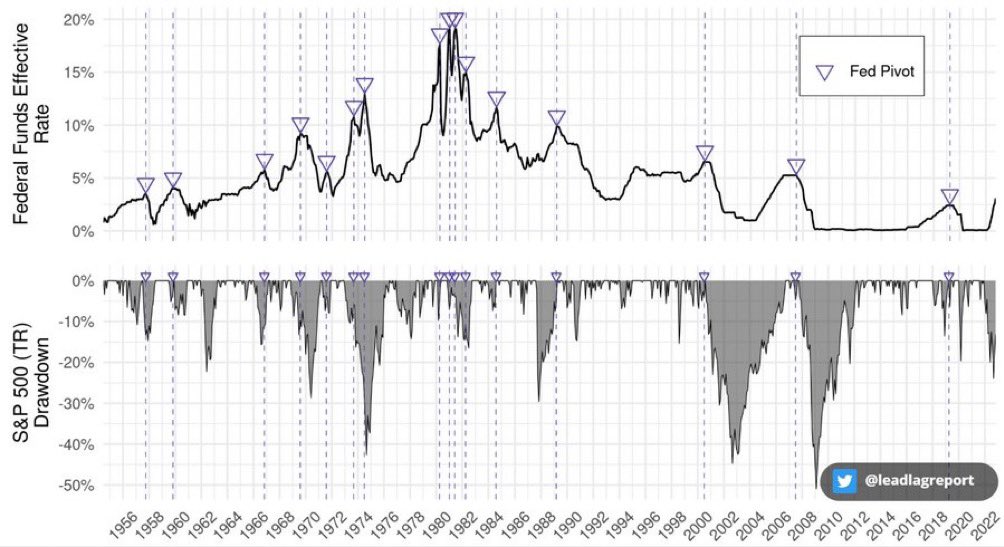

A picture is worth a thousand words on this topic, and thankfully Michael Gayed has a chart for us:

The top panel is the Fed Funds rate, with the arrows showing when the Fed pivoted from hiking to cutting rates. The bottom panel is the one to focus on, showing how those Fed pivots correspond to S&P 500 declines. They don't always come immediately before big market drawdowns — the 2019 example I just discussed shows that, as do the couple in the mid-late 1980s. Those are non-recessionary examples.

But wow are the recessionary bear market examples nasty! 2008, 2000, 1973, 1970 — these are nasty examples of the Fed cutting interest rates early in recessionary bear markets and the bear market ignoring the cuts and continuing to plunge.

All of which brings us back around to the central question SMI posed at the beginning of this year — are we headed into a recession or not? Because if we are, our expectations regarding how events from here play out need to be set accordingly.

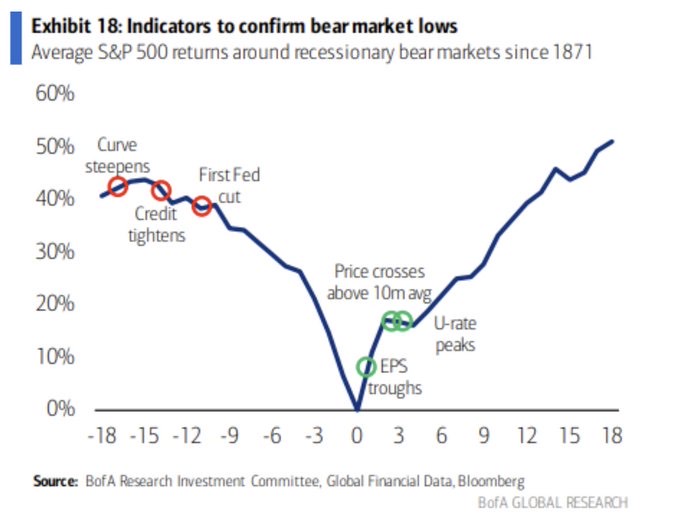

Bank of America gets the difference — their analysis correctly (in my view) draws a distinction between recessionary bear markets and other Fed pivots and bear markets that were not accompanied by a recession. Hide the women and children, because this next chart is ugly.

Since the bank crisis a month ago, there has been a notable tightening of credit. That's the second red circle on the chart. We've not yet had a Fed pause, much less a cut, yet. Much like the 2000-2002 bear market, we had a market adjustment for higher interest rates last year, followed by a long pause in the bear market while the "long and variable lag" of Fed rate hikes filtered through the economy. Now, it appears those rate hikes are starting to show up in slowing growth, signaling a recession ahead.

If that proves to be an accurate interpretation, the optimism stock investors are displaying today is likely to be short-lived. They're assuming this will play out like 2019 — the Fed will pivot and stocks will roar higher on lower rates and more stimulus. Based on past recessionary bear markets though, it seems more likely that we have a valley of pain to traverse before those sunnier days return for stocks.

That doesn't mean this will start tomorrow. The SMI strategies actually added a bit more risk exposure for April, which helps on a day like today when stocks are roaring. But we're not under any illusions that those moves were anything more than a short-term trade. Time will tell, but we think the voices saying last October was the bear market bottom and we're in a new bull market are going to be unpleasantly surprised as recession shows up in the months ahead.