The recent announcement that Mint, the popular (and free) online money-management system, will shut down on Jan. 1, 2024, took the personal-financial-management world by surprise — including Mint’s millions of users. Mint’s owner, Intuit, is encouraging users to switch to another Intuit-owned platform, CreditKarma. But even though CreditKarma will take on some of Mint’s features, it won’t provide what many Mint-ers want: the ability to create a monthly budget and track spending by category. (If desired, Mint users can download and preserve their existing data.)

For those seeking a Mint alternative — and for other readers looking for a financial management platform — here is an SMI overview of four popular options: the FaithFi App, EveryDollar, YNAB, and Tiller.

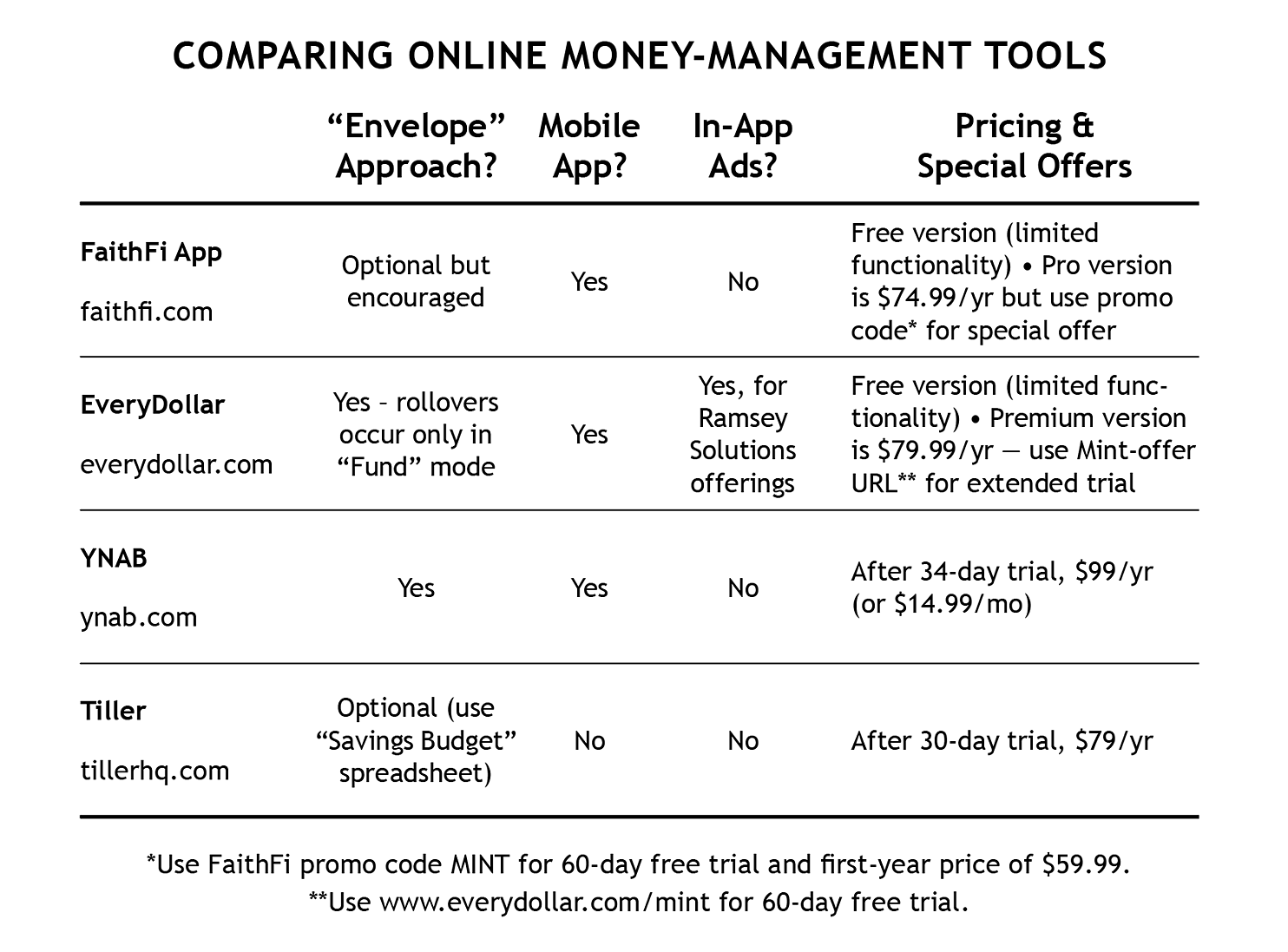

Two (FaithFi and EveryDollar) offer no-cost versions, but those free versions have limited functionality. All four platforms support browser-based access. Three (see table below) also have smartphone/tablet versions.

Bear in mind that each platform has a significant learning curve. Getting up to speed requires time and effort. Fortunately, each offers an introductory trial period. They also provide online training sessions, including regular live webinars that allow users to ask questions.

The FaithFi App

Sound Mind Investing has had a long-standing relationship with FaithFi (formerly MoneyWise), the organization behind this app. (SMI has been a long-time underwriter of FaithFi's daily radio program, but SMI has no economic relationship or incentive to promote their product.)

As the “FaithFi” moniker suggests, this app is aimed at helping Christians be faithful in financial management. To that end, the app provides (in both the free and Pro versions) an ever-growing library of stewardship-oriented articles plus access to an online forum where users encourage one another in their financial discipleship.

Another feature that sets the FaithFi App apart from other platforms is that it allows users to choose among three “system types” for tracking/managing money: “Track-Only,” “Monthly Spending Plan,” and “Envelope System.”

“Track Only” is handy for people new to budgeting who need to track their spending for a month or two before creating a spending plan. The “Monthly Budget” mode (functionally similar to Mint) allows users to set up a monthly cash flow plan and track transactions by spending category. The “Envelope System” keeps closer tabs on actual cash flow by not allowing a category (“envelope”) to be fully funded until the user has the cash available in a bank account. The “Envelope System” also carries forward any surplus or deficit within a category from one month to the next, giving a more accurate picture of cash flow over periods longer than a month.

Posting transaction data to the FaithFi App can be done in three ways. A user can input transactions manually or — in the Pro version of the app — import transactions automatically (via third-party financial services company Plaid).

Users can manually categorize transactions or create “rules” to categorize transactions automatically. As necessary, a transaction can be split among multiple categories (for example, assigning part of an expenditure to “groceries” and the rest to “household supplies”).

FaithFi is encouraging Mint users to try the app by offering a 60-day free trial plus a discounted price on a one-year subscription (see table below).

EveryDollar

The EveryDollar platform from Ramsey Solutions (founded by financial author and talk show host Dave Ramsey) stresses “zero-based” budgeting.

EveryDollar requires users to assign each dollar of monthly income a “job.” For example, a specific number of dollars might be “assigned” to pay the mortgage. The “job” of other dollars could be to purchase groceries. And so on. When the total cost of each of these “jobs” is subtracted from total income, the result should be zero. This approach aims to help users 1) cover all necessary expenses and 2) avoid impulse spending by laying out a plan of what will happen with every dollar that comes in.

In the free version of EveryDollar, users must enter transaction data manually using a pop-up screen that prompts for the amount spent and the budget category to which it should be assigned. The Premium (paid) version of EveryDollar can automatically access data from linked accounts (via data supplier Finicity, owned by MasterCard). After transaction data is imported, users can “drag and drop” each transaction to its appropriate spending category.

EveryDollar allows any category to be set as a “Fund.” With this option, a user can track progress toward a financial goal — such as saving toward a future major purchase. The amount in a category marked as a “Fund” will roll over from one month to the next.

To attract Mint users, Ramsey Solutions is offering the premium version of EveryDollar free for 60 days (see table below).

YNAB

Like EveryDollar, YNAB — pronounced why-nab — is based on the zero-based budgeting model of giving every dollar of income a job (the letters originally stood for You Need a Budget). But the YNAB approach emphasizes looking beyond recurring monthly expenses. It underscores taking into account the infrequent outflows that people often fail to plan for (insurance premiums, gift-buying) and less predictable expenditures, such as car repair.

Unlike other apps, YNAB stresses “aging your money,” i.e., increasing the time between when money is earned and when it is spent. The system nudges users toward (eventually) having at least a one-month financial cushion — money earned in January is for February, money earned in February is for March, and so on. This approach aims to end the “living paycheck to paycheck” cycle.

YNAB users can input their transaction data manually or use an auto-import function that pulls data from third-party aggregators MX and Plaid. When a credit card transaction occurs, YNAB will designate it as such and automatically earmark the amount spent on the credit card for the next card payment — a “nudge” that prompts users to pay their charges in full each month. If a category is overspent, YNAB asks which other category the money should come from, thus helping users keep their overall spending from exceeding their income.

Click to zoom

Although YNAB isn’t offering a special deal for Mint-ers, it does have a 34-day free trial that allows any new user to try out the platform. At the end of the trial period, a new user isn’t subscribed automatically. The person must choose to subscribe or not. (YNAB offers a one-year free trial for college students.)

Tiller

Instead of using an off-the-shelf system designed by someone else, many people prefer to manage their money via a “homegrown” spreadsheet. The downside is that spreadsheets typically require tedious manual entry of transactions.

Enter Tiller. Tiller pairs spreadsheet budgeting with automated transaction posting. The system works with Google Sheets (which requires a Google account) and Microsoft Excel.

Tiller’s primary offering is a robust spreadsheet called the Foundation Template. A user can build on that “foundation” by adding homegrown sheets and/or by selecting sheets designed by other Tiller users (“Tiller Community Solutions”).

Once a user’s bank and credit card accounts are linked to Tiller, transaction data (imported via third-party Envestnet/Yodlee) will flow into a spreadsheet tab called “Transactions.” Users can manually categorize each transaction (via a pull-down menu) or create keyword rules that enable auto-categorization. Cash transactions, of course, must be entered manually. Users can split any transaction among two or more categories.

Tiller users who wish to use an “envelope system” approach — with month-to-month rollovers — can implement the “Savings Budget” from Tiller’s Community Solutions area. This addition to the Foundation Template tracks money left over in a given category at the end of a month and rolls it over to the same category for the next month (or reallocates it to a different category if the user chooses). If there is a shortfall within a category, the deficit is subtracted from the next month’s allocation, thus helping the user gain a clearer picture of cash flow.

Tiller offers a 30-day free trial for new users.

A free option from your bank?

Increasingly, banks are adding money-management resources to their websites, including no-cost tools for budgeting and tracking (even tracking transactions related to “external” accounts at other banks and financial companies). So, if you’re committed to finding a free option that pulls in transactions automatically, check with your bank.

Unfortunately, the bank-based tools we looked at restrict users to a handful of budget categories and offer sharply limited options for reports and customization. But if you don’t mind a less flexible system, an online tool from your bank (if available) may be sufficient.