Few investors had ever experienced anything like the second quarter of 2025. And yet, an investor who fell asleep on March 31 and woke up to check their account statement on June 30 could be excused for thinking it was a rather ordinary period!

We’re referring, of course, to the tumult caused by the massive tariff announcement on “Liberation Day,” April 2. On that same day, OPEC announced a major acceleration in its rate of production, which sent oil prices plunging.

Financial markets reacted violently, with U.S. stocks, bonds, and the dollar falling sharply over the following week. After a broad tariff “pause” was announced on April 9, U.S. stocks and bonds stabilized and began to recover.

The fireworks weren’t quite over, however. In June, Israel launched a series of direct attacks on Iran, which ultimately culminated in the U.S. bombing Iran’s major nuclear sites.

An investor who knew all this would happen during the 2nd quarter might easily have expected stocks to be down -20%, -30%, or more. And in fact, at the April low, the S&P 500 Index was down -21.3% from its February high. But the market came roaring back over the remainder of the quarter, ultimately ending the quarter at a new all-time high.

Such massive swings — from a booming market early in 2025, to plummeting in March and April, and back to booming again by June — are unfriendly conditions for trend-following strategies. But with one painful exception, SMI’s strategies have navigated 2025’s volatile waters reasonably well.

Just-the-Basics (JtB) & Stock Upgrading

SMI’s JtB strategy outperformed the U.S. broad market (Wilshire 5000 Index) during the second quarter as well as the first half of 2025. While small-company stocks have been poor performers overall in 2025 (the small-company Russell 2000 index fell -1.8% during the first half of the year), foreign markets have helped make up for that, rising +18.5%. The falling U.S. Dollar has amplified foreign stock returns for U.S. investors, effectively giving them a currency “boost” as the returns of foreign markets are translated into relatively weaker U.S. dollars.

Stock Upgrading gained +7.6% during the second quarter, but was up just +2.2% for the first half of the year overall. Both of those numbers trailed the U.S. broad market.

Indicative of the strain such volatility puts on active trend-following strategies, all five of SU’s March holdings (other than FCTE) were replaced by the end of June. FCTE also experienced significant turnover in the individual stocks it “upgrades” within its ETF wrapper. FCTE trailed Upgrading’s other fund holdings during the second quarter, but slightly outperformed them overall during the first half of the year (FCTE +2.7%, SU +2.2%).

The broad allocations within Stock Upgrading shifted notably over the course of the second quarter. From a starting point of 70% large companies, 20% small companies, and 10% commodities at the end of the first quarter, SU shifted to 60% large, 10% small, 20% foreign, and 10% commodities by the end of the quarter. This directly reflected the strength of foreign stocks relative to U.S. stocks early this year. These allocation changes were too recent to impact SU’s second-quarter performance, but we believe this flexibility to pursue the strongest momentum between categories will pay off in the long run.

Bond Upgrading (BU)

There hasn’t been a lot to discuss regarding our bond holdings of late. Since the start of 2023, interest rates have experienced at least seven distinct mini-trend changes (from higher rates to lower, or vice versa). That’s a remarkable amount of volatility in the direction of rates, tied directly to repeated shifts in investor concerns about the likelihood of a future recession.

The lack of a sustained trend explains why we pivoted BU’s active holding to Bulletshares in May 2024. While not particularly exciting, it’s less rate sensitive and avoids the ups and downs caused by these repeated rate cycle reversals. Bond Upgrading beat the Bloomberg U.S. Bond Index slightly in the second quarter when rates were rising, lagged it slightly for the first half as a whole, and is dead even with the index over the past 12 months at +6.1%.

Dynamic Asset Allocation (DAA)

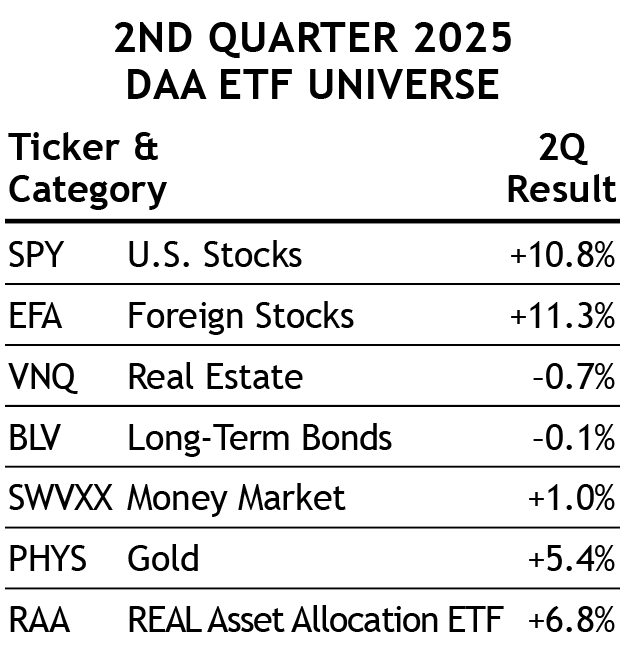

DAA took a slight breather during the second quarter, gaining “only” +6.9%. This was largely due to gold slowing its rapid ascent, though it still gained +5.4% during the 2nd quarter.

Overall, DAA was clearly the star performer of the first half of 2025, gaining +10.9%, and outperforming SMI’s other strategies as well as all the relevant indexes. DAA’s performance was driven by gold’s incredible +25.9% first-half gain (it’s up nearly +40% over the past 12 months). Foreign stocks were also up sharply at +20.3% during the year’s first half.

DAA’s blend of assets during the second quarter is worth reviewing. Gold and Foreign Stocks were each recommended throughout the entire quarter. The strategy’s third slot initially appeared to be a brilliant stroke, as it pivoted out of U.S. Stocks and into Cash at the end of March, just days prior to the April 2 swoon!

While that was initially great for DAA investor emotions, the market’s remarkably fast rebound eventually left that slot flat-footed. At the end of April, DAA transitioned from cash to bonds, then at the end of May from bonds back to U.S. Stocks.

March's new addition to DAA — the SMI 3Fourteen REAL Asset Allocation ETF (RAA) — is off to a good start. Its second-quarter gain of +6.8% roughly held pace with DAA’s stock-heavy portfolio (+6.9%), which was no small feat given the twists and turns of the quarter and the fact that RAA shifted its allocations pretty defensively initially in response to the market tumult.

One of RAA’s smallest holdings — Bitcoin, which comprised just ~3% of the ETF during the quarter — made a significant contribution to its performance. Bitcoin gained +30% during the second quarter, meaning RAA’s 3% allocation contributed almost +1.0% of the ETF’s overall quarterly gain of +6.8%.

Sector Rotation (SR)

As noted earlier, SR got off to a miserable start for the quarter as a result of the April 2 news that OPEC was accelerating its plans to boost oil supply much faster than had been previously communicated. This push to expand OPEC’s market share lowered energy prices — great for U.S. consumers, but terrible for the leveraged energy stock fund SR had purchased just days prior based on its recent strength.

After taking that nasty punch, SR responded well. At the end of April, SR pivoted into defense stocks, which have been strong performers, gaining +12.7% in May and another +6.0% in June.

As a side note, our partners at SMI Advisory Services have spent considerable time recently building infrastructure to allow for more efficient testing of various trend-following scenarios. (SMI Advisory Services and the SMI newsletter are separate but affiliated companies.) This type of testing has always been an incredibly time-consuming and laborious process, limiting our ability to explore various strategy tweaks and alternatives.

The initial focus of this testing has been on SR, given its weak recent performance. After looking at SR many different ways — faster and slower momentum formulas, higher and lower levels of diversification, various selling disciplines, etc. — two things are clear.

First, the current version of SMI newsletter SR (one holding, 1mo+3mo+6mo MOM score, using the top quartile selling discipline), has been generating solid signals. Second, as reported in recent SR write-ups, efforts to reduce the strategy’s volatility and occasional rough outcomes by selecting less aggressive/volatile funds have hampered SR’s realized performance significantly in recent years.

The takeaways from this extensive recent research are clear. Nothing in our testing indicates SR should perform any less robustly going forward than it did during its first 15 years when it ran circles around the indexes and all of SMI”s other strategies. However, a word of caution is warranted. We’re reiterating the “old SR rules” which dictated that SR risk management has to come from limiting your personal allocation to the strategy, because we’re no longer going to try to mitigate SR risk by shying away from the most aggressive funds in SR, even at times when market risk appears acute. That may mean an allocation of less than 10% may be appropriate for less aggressive investors (see next section).

50/40/10 (with 60/40 stock-bond Upgrading)

This portfolio refers to the specific blend of SMI strategies — 50% DAA, 40% Upgrading, 10% Sector Rotation — that SMI has often discussed as a general guideline, or starting point, for member strategy allocations. In 2024, we started reporting this portfolio using a 60/40 split between Stock and Bond Upgrading within the 40% Upgrading allocation. This is a reasonable reflection of how most SMI investors utilize such a “whole portfolio” blend and is an example of the type of diversified portfolio we encourage SMI readers to consider.

(Note: Blending strategies adds complexity. Some members may prefer the automated approach offered by SMI Private Client, a separate company from the SMI newsletter.)

This version of a 50/40/10 portfolio was dragged down considerably by SR’s poor 2025 returns. That said, it still gained +5.1% during the second quarter, and +4.2% year-to-date through the end of June. Those returns are lower than we’d prefer, but not disastrous.

Conclusion

Hopefully, markets will have the chance to build the type of sustainable trends that SMI’s strategies can capitalize on during the second half of the year. The past year or so has been an extremely trying period for most trend-following approaches, with many experiencing some of the worst performance of their history. We’re grateful that DAA has been such a strong performer (+19.4% over the past year), helping to take that edge off within our diversified portfolios.

We continue to dig deep into our existing strategies, looking for ways to improve and strengthen them. As evidenced by the additions of FCTE and DAA this past year, we’re not averse to making significant changes if we think they will prove beneficial to SMI investors.

When markets start turning vertical and are hitting new all-time highs seemingly daily, it’s easy to forget the very real risks investors are constantly exposed to. Some of the threats lurking in the years ahead are potentially of the “generational” variety — the uncertainty surrounding the rise of AI, runaway national debts, a shift away from free trade, the dollar and U.S. Treasuries serving as the backbone of the global financial system, etc. Our endeavor is to create robust portfolios that can withstand those challenges and help SMI members reach their long-term financial goals.