Markets slipped on the ice in December, but that didn’t detract much from a strong year of absolute gains for SMI investors. Stock Upgrading, Just-the-Basics, and Dynamic Asset Allocation each set new all-time highs late in 2024. Given these strategies comprise the bulk of most SMI portfolios, it’s likely many SMI members set new personal highs in 2024, too.

As with many things in life, our satisfaction with returns depends significantly on what they’re being compared to. Again in 2024, the Magnificent Seven giant tech stocks were the biggest winners. This narrow group of heavyweights now comprise more than one-third of the S&P 500 Index, exposing a potentially dangerous lack of diversification in this supposedly “broad U.S. market” index.

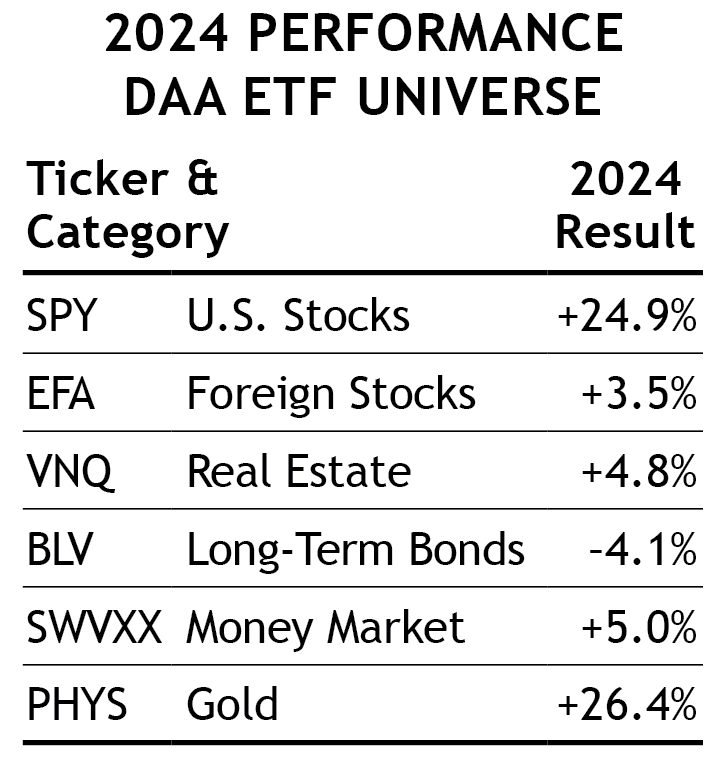

That “concentration risk” is evident in 2024’s index returns. The capital-weighted S&P 500 Index (where companies with greater market value count for more) soared +25.0% in 2024. However, the equal-weight version of the S&P 500 Index was up only about half as much, at +13.0%. The small-company-focused Russell 2000 Index gained even less, at +11.5%. Foreign stocks barely gained at all, up just +3.5% (EFA).

While 2024 was a second consecutive banner year for U.S. stocks, bonds continued the weakness that began in 2021. The Bloomberg U.S. Bond Index gained a scant +1.25% in 2024, dragging down returns for investors with high bond exposure through conventional 60/40 or similarly constructed portfolios.

Let’s briefly review the performance and current status of each SMI strategy.

Just-the-Basics (JtB) & Stock Upgrading

Given the weakness in smaller-company and foreign stocks, JtB acquitted itself quite well last year, gaining +17.8%. The fact that its large-company allocation is invested directly in an S&P 500 Index fund certainly helped. As noted last month, we’ve altered JtB’s allocations to more closely reflect the U.S. market weightings between large and small stocks, while de-emphasizing foreign stocks somewhat. The trends for small-company and foreign stocks will surely revert back eventually, but we’d prefer to adjust our portfolios after the pendulum changes direction, as opposed to positioning for it in advance.

Stock Upgrading was similarly strong in 2024, also gaining +17.8%. In August, SMI added a second distinct approach to the upgrading process with the new Full-Cycle Trend ETF (FCTE). Full-Cycle Trend is really a separate strategy within the broader Stock Upgrading strategy, which can be reasonably thought of as “Upgrading for individual stocks.”

Apart from its larger 50% allocation, the way FCTE is displayed to SMI members makes it look like any other stock fund holding within Upgrading. That isn’t actually the case, as FCTE is implementing the Full-Cycle Trend process on the individual stocks in its universe within that single ETF. The other half of the Stock Upgrading portfolio continues to upgrade from one fund to another based on the recent momentum scores of each fund. (See Stock Upgrading’s current recommendations here.)

To summarize, we now have two separate systems operating side-by-side under the Stock Upgrading umbrella. Half the portfolio is being run using stock funds as before, the other half is now running a different system applied to individual stocks within FCTE.

This two-strategies-in-one Stock Upgrading approach worked well in 2024, despite SMI newsletter members not being able to access the new FCTE holding until the second half of the year. That was unfortunate, as it was the superior performer through the first nine months of 2024. Subsequently, the “traditional” fund side of the portfolio contributed strong gains late in the year as FCTE tailed off. Our expectation is that including both approaches within Stock Upgrading will provide us with strong performance and a diversification benefit as well.

A final note on Full-Cycle Trend: after a strong third quarter, the fourth quarter of 2024 was the strategy’s worst performance relative to the S&P 500 Index in the strategy’s history. However, the silver lining is that historically Full-Cycle Trend has tended to bounce back strongly after experiencing a negative quarter (+5.5% on average in the following quarter). No surprise, then, that through the first three weeks of January, FCTE beat the S&P 500 Index by a +5.9% to +2.9% margin. Since its inception last July, FCTE was ahead of the index by +1.1% (through Jan. 21).

Bond Upgrading

Investing in bonds has been tough in recent years, but Bond Upgrading has done a reasonably good job of turning lemons into lemonade. It’s been our contention that government spending in response to COVID ended the decades-long bond bull market, ushering in a new era of higher inflation and correspondingly higher interest rates. Over the past three years, investors in long-term Treasury bonds (TLT) have lost a shocking -35.0% of their money. The Bloomberg U.S. Bond Index is down -7.1% over those three years. Bond Upgrading has done better than both, with a modest loss of only -0.6% (it gained +1.35% in 2024, slightly better than the broad bond index).

Still, losing any money over a three-year period is hardly what conservative bond investors expect. This is why SMI frequently focuses on the impact of inflation and higher interest rates. It’s also why SMI portfolios have been intentionally structured to rely less on static bond allocations and more on alternative approaches like DAA.

Dynamic Asset Allocation (DAA)

DAA was a surprisingly strong performer in 2024, gaining +17.3%. We say “surprisingly” due to this strategy’s defensive reputation and historical tendency to lag during strong bull markets.

Driving DAA’s strong 2024 performance was its large allocations to S&P 500 stocks and gold. As the table shows, both experienced dramatically higher gains than the other asset classes. In fact, none of the other three classes (foreign stocks, real estate, or bonds) were able to keep pace with a simple money market fund last year. This explains why one-third of the DAA portfolio shifted to cash for January.

Sector Rotation (SR)

SR lagged SMI’s other stock-oriented strategies in 2024, while posting a gain that wouldn’t look out of place most years. Despite a significant loss in December, SR’s exceptionally strong post-election bounce in November helped it salvage a 2024 gain of +9.6%.

While that gain was unimpressive relative to the market and SMI’s other strategies, a thorough review of the SR process last year did reveal reason for optimism going forward. To summarize, in an effort to curb SR’s volatility, refraining from using leveraged funds has hurt SR’s recent returns. Going forward, we expect a return to SR’s higher gaining, high volatility ways.

50/40/10 (with 60/40 stock-bond Upgrading)

This portfolio refers to the specific blend of SMI strategies — 50% DAA, 40% Upgrading, 10% Sector Rotation — discussed in our article, Higher Returns With Less Risk, Re-Examined. In 2024, we started reporting this portfolio using a 60/40 split between Stock & Bond Upgrading within the 40% Upgrading allocation. This is a reasonable reflection of how most SMI investors utilize such a “whole portfolio” blend and is a great example of the type of diversified portfolio we encourage most SMI readers to consider. (Note: Blending strategies adds complexity. Some members may prefer the automated approach offered by SMI Private Client.)

This version of a 50/40/10 portfolio gained +13.9% in 2024, with nearly all of that gain coming from the equity side of the portfolio. That gain compares favorably with the +11.2% a well-diversified 60/40 JtB portfolio would have earned, or the +10.6% of a 60/40 Upgrading portfolio.

Conclusion

As we discussed at length in January's cover article, Trump 2.0: Using Objective Investing Models to Guide Us Through Anticipated Disruption, the new administration policies have the potential to throw any number of curveballs at investors this year. Correctly anticipating the outcome of those policies is unlikely, but we have confidence that SMI’s trend-following strategies will adapt to whatever this administration and markets send our way.