For the second year in a row, investors had to navigate a significant external market shock early in the year. Last year, it was investors’ reactions in April to new tariffs on imports which caused the S&P 500 Index to plunge -19%. This year was the Iran War. At the lows, the S&P 500 Index fell -8.5% from its late-January high, while the tech-heavy Nasdaq Index dropped -13.0% from its late-October high.

The good news is SMI’s strategies navigated these stormy seas with aplomb! Our trend-following processes steered us out of the more speculative stocks early in the year, in favor of higher quality and “real economy” sectors. That helped us build a significant lead over the market before the war began. While we gave back some of those gains during March, our commodities and natural resources exposure helped limit losses.

Both the Stock Upgrading and DAA processes came close to calling for adjustments by the end of March, but fortunately the required momentum scores were never quite reached. That turned out to be very beneficial once the cease-fire was announced, as the April rebound rally has been the strongest that the stock market has experienced since the end of the Global Financial Crisis. Being fully invested as markets have recovered has been great.

Just-the-Basics (JtB) & Stock Upgrading

The strength of foreign and small-company stocks early in the quarter helped offset the fact that foreign stocks fell more than U.S. stocks in March after the war began. Most foreign countries are more heavily dependent on energy imports and were at higher risk from a prolonged closure of the Strait of Hormuz.

That said, looking at the quarter overall, JtB’s foreign holding was the standout at +2.3%, despite the rough March. JtB’s extended market holding fell slightly at -1.3%, while the S&P 500 component was down -4.4%. JtB’s overall loss of -1.8% compared favorably to the broad market’s first quarter decline of -4.0%.

Stock Upgrading was the star of the first quarter, gaining +5.8% while the market fell -4.0%. That’s a considerable difference for a single quarter!

Upgrading’s commodities holding provided tremendous diversification, gaining +11.6% in March alone (when most everything else was falling), and finishing the quarter with a +23.7% gain.

Aegis Value, which gained +74% during its first year recommended (through 3/31), also owns many commodity-producing companies. It gained a similarly impressive +16.3% during the first quarter.

As noted earlier, foreign funds were great during January and February, then fell sharply in March once the war started. The good outweighed the bad for Stock Upgrading’s two active foreign holdings though, as they finished the first quarter with gains of +9.8% and 5.7% respectively.

Both of Stock Upgrading’s large company holdings outperformed the market during the quarter. FCTE limited its loss to just -1.0% while the S&P 500 Index fell -4.4%. Upgrading’s “index switching” holding (IWD) gained +2.0% on the strength of its pre-war performance. Overall, it was a rare quarter where everything worked for Stock Upgrading!

Bond Upgrading (BU)

SMI introduced a new Bond Upgrading approach in January of this year, designed to take better advantage of the higher bond market volatility witnessed since rates started rising in 2021. When rates were falling steadily between 1982-2020, a heavily indexed bond approach made sense. But that hadn’t worked well in the new post-COVID interest rate environment, so SMI pivoted to a new collection of active bond managers, each specializing in a slightly different bond niche.

We’re happy to report this new approach is off to a good start. Despite continued high interest rate volatility — rates fell sharply during January and February before spiking higher in March — Bond Upgrading managed a +0.7% gain for the quarter. That’s pretty decent in an absolute sense, but looks even better in light of the Bloomberg U.S. Aggregate Bond Index’s quarterly loss of -0.1%.

We don’t plan to regularly focus on the individual components of BU, as the point is to blend their various specialties into a bond portfolio we can live with through all different types of interest rate environments. But it’s worth noting that BU’s foreign bond holding, Eaton Vance Global Macro Absolute Return (EAGMX), paid off immediately with a first quarter gain of +2.3%. It’s the first time SMI has specifically recommended a foreign bond holding, so we’re glad it got off on the right foot!

Dynamic Asset Allocation (DAA)

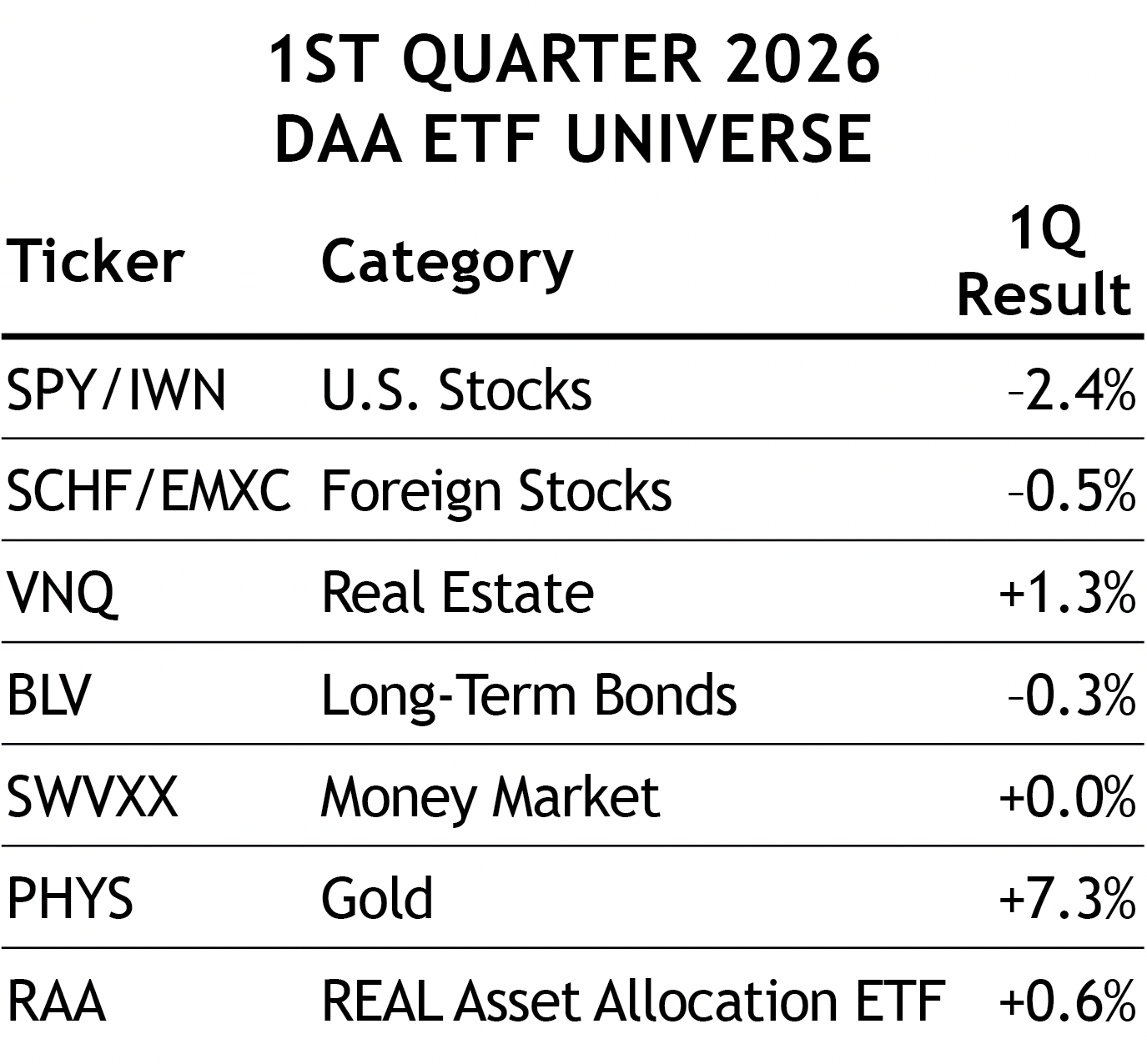

DAA has been hitched to a golden rocket for a while now. Driven largely by Gold’s stunning +158% gain over the prior two years since DAA first recommended it (at the end of February 2024), DAA entered the war boasting the best recent performance of any SMI strategy.

But not even rockets are immune to occasional speed bumps. That was true for Gold (and DAA) as the war deepened during March. Gold was up +23% already in 2026 as of March 2, the first trading day after the war started. But it would give up that entire gain by March 26, before a month-end rally helped it notch a +7.3% quarterly gain.

As noted earlier, Foreign Stocks also were strong early in the quarter, only to give back those gains during March.

While Gold and Foreign Stocks were volatile during the quarter, DAA’s other half — the SMI 3Fourteen REAL Asset Allocation ETF (RAA) — did exactly what we would have hoped, managing the extreme volatility of the quarter to provide market-beating performance. RAA’s gain of +0.6% handily outperformed the -2.6% loss of a 60% stock, 40% bond benchmark portfolio.

Sector Rotation (SR)

Sector Rotation posted strong first-quarter performance, gaining +5.3%. That’s a greater than +20% annualized rate, but is even more impressive given the broad market’s loss of -4.0%. As impressive as that was, being invested in SR’s current holding as April’s huge rally took hold has been even better. As this is being written, SR’s current holding is up +14.8% year-to-date, vs. just +3.2% for the S&P 500 Index (through 4/16).

50/40/10 (with 60/40 stock-bond Upgrading)

This portfolio refers to the specific blend of SMI strategies — 50% DAA, 40% Upgrading, 10% Sector Rotation — discussed in our April 2018 cover article, Higher Returns With Less Risk, Re-Examined. In 2024, we started reporting this portfolio using a 60/40 split between Stock & Bond Upgrading within the 40% Upgrading allocation. This is a reasonable reflection of how most SMI investors utilize such a “whole portfolio” blend and is a great example of the type of diversified portfolio we encourage most SMI readers to consider.

(Note: Blending strategies adds complexity. Some members may prefer the automated approach offered by SMI Private Client.)

This version of a 50/40/10 portfolio — i.e., with a 60/40 allocation within Upgrading — gained a solid +2.6% during the first quarter, which compares very favorably to the -2.6% loss of a generic 60% stock, 40% bond indexed portfolio. With all three of SMI’s active strategies posting first quarter gains while both the broad stock and bond markets were losing ground, it was a great quarter for SMI members!