It pains me to title an article this way. So many of the market’s — and broader society’s — current problems can be traced back to the increasingly activist role the Federal Reserve has taken in the markets over the past 35 years. I sincerely wish their actions didn’t matter so much to the market’s course of action.

But the Fed is the elephant in the investing room. Ignore it at your peril.

To employ another metaphor, these are the cards we have been dealt, even if they’re not the cards we want. It’s our job to play those cards correctly, so we’d better understand the current rules of the game.

It’s been pretty obvious the financial markets have been riding the wave of Fed (and other global central banks) liquidity higher since the March 2020 lows. In addition to lowering interest rates to near zero in the U.S. (and below zero in much of the world — there is roughly $13 trillion of negative-yielding debt globallly), the Fed has also been buying $80 billion of Treasury securities and another $40 billion of mortgage-backed securities every month since March 2020. It’s an extraordinary and unprecedented level of support to financial markets.

This incredible degree of Fed (and Government) support, coupled with a strong economic rebound from last year’s COVID shutdowns, produced nearly perfect conditions for financial assets. The market has roughly doubled from its March 2020 lows, in a span of just over 16 months. SMI tilted hard into small-company stocks to ride that wave and was rewarded, as the market followed the same script as during the 2003 and 2009 post-bear market recoveries, with riskier small-company stocks outperforming.

Back to the Fed. I’ve written about the "Fed Flinch" that occurred at the mid-June meeting, exactly eight weeks ago. The impact of Fed Chairman Powell’s speech that day has been stark, as I’ll show below. In a nutshell, Powell told the market that the Fed wasn’t going to be as slow to react to rising inflation as the market believed (as a result of being repeatedly told as much by Fed speakers). This recalibration of the risk of the Fed tightening monetary policy sooner than expected has been the most important market event so far in 2021.

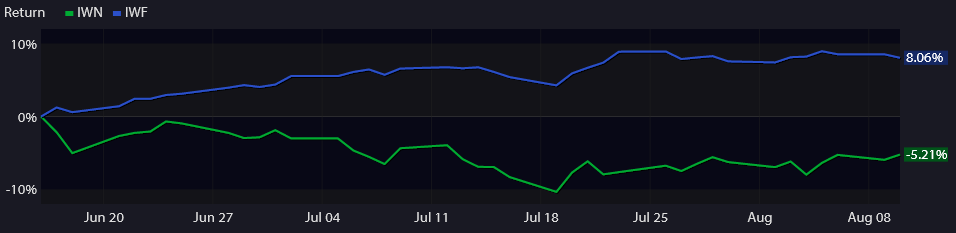

Think I’m overstating my case? Consider the following two charts that compare the performance of the small/value ETF (IWN) and the large/growth ETF (IWF).

Here’s the comparison from November 5, 2020 (the day of the first positive vaccine news) through June 16, 2021 (the day of the Fed Flinch).

Click Graph to Enlarge

This is the "re-opening" trade in a single chart. As the prospect of the end of the pandemic came into view, investors pushed smaller-company stocks and more economically sensitive value stocks massively higher. Large-growth stocks? Meh, they were fine too. But the real action was in the more volatile stuff.

That ended on a dime when the Fed said they were thinking about tapering their support sooner than later. Here’s the same comparison from June 16 through yesterday (8/10):

Click Graph to Enlarge

Just a whiff of Fed tightening was enough to put an end to the re-opening trade and get investors rotating back into the perceived safety of large/growth stocks. (Rightly or wrongly, today’s FAANG stocks are perceived to be the safest haven in the stock market these days.)

Probabilities, not certainties

While the degree of Fed largesse today is unprecedented, the general pattern is one investors have been dealing with for a dozen years now. Past cycles of Fed stimulus/tightening offer clues as to what we might expect going forward.

First, as the charts above indicate, the "hyper-growth" portion of the recovery is likely over. There’s plenty of data to support the conclusion that economic growth peaked in the second quarter of this year and, while growth is still above its long-term trend, the rate of that growth is now slowing. Translation: growth is still good, but it’s no longer great and it’s no longer accelerating. History tells us that the initial burst that markets get from those initial conditions is past now, which (combined with the objective data in the charts above) is why the SMI strategies have been pivoting away from being way overweighted to small stocks and have shifted toward allocations that look more like the broad market composition (which is weighted roughly 75% large stocks and 25% small stocks).

Second, we don’t know exactly when the Fed will actually start tapering their support or how aggressive they’ll be when they do start. But they are certainly making a lot of noise about it. Nearly every day it seems there’s another Fed speaker saying something about tapering. I doubt this is accidental. Major policy shifts often have been announced at the Fed’s Jackson Hole conference, which is coming up at the end of August. With headline inflation continuing to come in hot, the Fed is increasingly under pressure to get moving.

Third, we have two prior tapering/tightening cycles to evaluate in the post-Great Financial Crisis era since 2009. (Additional clues can be gleaned from the market’s response when the first few Quantitative Easing cycles ended, but those were structured differently with pre-defined endpoints that were known from the beginning, so I’m ignoring those.)

Episode 1: The Fed started gradually tapering its asset purchases in December 2013. After gaining +33.1% in 2013, the market continued to rise at a slower rate in 2014 (+12.7%) before suffering back-to-back corrections in late-2015 and early-2016. (It’s worth noting the Fed also hiked interest rates for the first time in December 2015, between the two market corrections.)

Episode 2: The second policy tightening episode began in October 2017 and it was a little different. Whereas the earlier episode was tapering, or slowing the rate of growth of additional new asset purchases (i.e. the Fed’s balance sheet was still growing, just at a slower rate), the 2017-18 actions were actually designed to shrink the Fed’s balance sheet. Just under a year later, in September 2018, the market started to roll over into a correction that culminated in a nearly -20% drop over the following three months.

One takeaway from this is that even if the Fed does begin to taper, that’s not a definite signal that markets will immediately decline. Fed policy operates on a lag, meaning its impact doesn’t show up in the economy for a number of months.

But risk clearly did increase in both of these instances. The broad stock market has notched double-digit gains every calendar year since 2011 except two: +0.7% in 2015 and -5.3% in 2018. Suspicious timing, given the two efforts to tighten Fed policy in the past decade ran ahead of those significant corrections by 12-24 months.

Conclusion

It could certainly play out differently this time around. By most measures, the market has never been more richly valued than it is today.

The main point of this post is not to lay out a specific road map. It’s to orient readers to the big picture dynamic currently in play.

On that score, the message is clear. The Fed is obviously signaling to the market that it wants to rein in its staggering level of support. When the Fed has tightened monetary policy in the recent past, that has led fairly directly to weaker market returns punctuated by a higher risk of corrections.

Investors are well aware of these dynamics, which is why we’ve seen the type of market rotation illustrated by the charts above over the past eight weeks. Measures of investor concern (primarily focused on hedging via the options market) show that many investors are hedging against potential losses at a significant rate. (Ironically, this actually suggests that the risk of a significant market decline is likely relatively low today, simply because big declines usually don’t occur when investors are heavily hedged against that outcome.)

But the landscape has clearly shifted. Investing always gets harder when markets get a year or two removed from the last bear market. The SMI portfolios are adjusting to reflect those changing (and higher) risks and we’re confident they’ll continue to steer us appropriately through whatever comes next.