For nearly 30 years, declining inflation and interest rates have perpetuated a massive bull market in bonds, producing excellent total returns. But with interest rates driven to dramatic lows by Federal Reserve policy, it’s only a matter of time until the pendulum reverses course and bond investors will be forced to deal with a new landscape of rising interest rates.That means it’s more important than ever to understand the basics of bonds and the factors that influence the bond market’s risks and returns. Let us introduce you to the often poorly understood world of investing in bonds.

It was wonderful to be young and working on Wall Street in the 1980s: never before had so many unskilled twenty-four-year-olds made so much money in so little time.... There has never before been such a fantastic exception to the rule of the marketplace that one takes out no more than one puts in.

So begins Liar’s Poker, Michael Lewis’ fascinating and often hilarious book on his experiences working in the bond market. He starts by telling of an incident that took place in 1986, and which he claims became a legend at the firm he worked for, Salomon Brothers. To dispel any pre-conceived notions you may have that the bond market is too boring to warrant your interest, I’m going to share part of it with you.

It begins when John Gutfreund, Salomon’s chairman, walks out onto the bond trading floor to have a few words with John Meriwether, one of his top bond traders.

He whispered a few words. He said, “One hand, one million dollars, no tears.” Meriwether grabbed the meaning instantly. Gutfreund wanted to play a single hand of Liar’s Poker, a bluffing game played with the serial numbers on dollar bills. For a million dollars! Normally his bets didn’t exceed a few hundred dollars. A million was unheard of. The final two words of his challenge, “no tears,” meant that the loser was expected to suffer a great deal of pain, but wasn’t entitled to whine about it. He’d just have to keep his poverty to himself. It seemed an act of sheer lunacy.

Meriwether was the King of the Game, the Liar’s Poker champion of the entire bond trading floor. He and the young traders who worked under him were obsessed by the game. They regarded it as their game. And they took it to a new level of seriousness.

People like John Meriwether believed that Liar’s Poker had a lot in common with bond trading. It tested a trader’s character. It honed a trader’s instincts. The game has some of the feeling of trading, just as jousting has some of the feel of war.

The bond traders of Morgan Stanley, Merrill Lynch, and other Wall Street firms all played some version of Liar’s Poker. But the place where the stakes ran highest, thanks to John Meriwether, was the New York bond trading floor of Salomon Brothers.

I’d like to tell you what happened that fateful day, but that would spoil the fun. If you’re interested, buy Lewis’ book. You’ll learn a lot about Wall Street, the bond market, and the revolutionary changes that took place in the 1980s. (Warning: Rated PG-13 for offensive language. A lot of the people who work on Wall Street seem to have limited vocabularies.) I won’t promise that if you pay attention to what follows, you’ll end up playing Liar’s Poker on Wall Street. But I am sure that you’ll have a better understanding of bonds: what they are, how they work, and why they should be included in your portfolio if increased stability is your goal.

Bonds are simply IOUs

America’s largest banks and corporations (not to mention our local, state, and federal governments) need your help — they’d like to borrow some of your money. To make sure you get the message, their ads are everywhere. The government promotes safety of principal and has created certain kinds of bonds with special tax advantages. Banks want your deposits and want you to know your money is safe with them because it’s “insured.” Bond funds tantalize you with suggestions of still-higher yields, although in their small print they remind you that “the value of your shares will fluctuate.” And of course, insurance companies promote the tax-deferred advantages of their annuities. You’re in the driver’s seat. To all these institutions, you’re a Very Important Person.

Does the thought of “renting” out your money seem strange? Chances are, you do it all the time. You probably think of it as buying a certificate of deposit (or Treasury bill, bond, or fixed annuity), but actually, you’re making a loan. The “rent” you’re being paid is called interest. In the financial markets, investors with extra money (lenders) rent it out to others who are in need of money (borrowers). The borrowers give their IOUs to the lenders.

Bonds are basically IOUs, kind of like bank CDs. They are a promise to repay the amount borrowed at a specified time in the future. The date on which the bonds will be paid off is called the maturity date and may be set at a few years out or, believe it or not, for as long as 100 years away. On the maturity date, the holder of the bond gets back its full face value (called par value). In order to make bonds affordable to a larger investing public, these IOUs are usually issued in $1,000 denominations.

Bonds promise to pay a fixed rate of interest (called the coupon rate) until they mature (are paid off). This rate doesn’t vary over the life of the bond. Remember that. Once the rate is set, it’s permanent. That’s why bonds are referred to as “fixed-income” investments. As we’ll soon see, it’s the unchanging nature of the interest rate that causes bonds to go up and down in value.

Why buy bonds?

If you want to protect your principal and set up a steady stream of income, then bonds, rather than stocks, are the answer. Current income is traditionally the most important reason people invest in bonds, which usually generate greater current income than CDs, money-market funds, or stocks.

They also can offer greater security than most common stocks since an issuer of a bond will do everything possible to meet its bond obligations. (Even Donald Trump accepted a humbling at the hands of his banks in order to gain the money necessary to meet his bonds’ interest payments.)

The interest owed on a corporate bond must be paid to bondholders before any dividends can be paid to the stockholders of the company. And it’s payable before federal, state, and city taxes. Being first in line helps make the investment safer.

While time is passing, many things can happen to interest rates or to the bond issuer (whoever borrowed the money from investors in the first place) to affect the value of the bonds. The more distant the maturity date, the more time for things to potentially go wrong. That’s why bonds with longer maturities carry more risk than ones with shorter maturities.

A bond investment example

Let’s learn how bond values fluctuate by working through an example. Assume XYZ Inc. wants to borrow $200 million for advanced research and doesn’t want to have to pay the loan back for 30 years. Banks generally don’t like to lend their money out for such long periods of time, so the company decides to issue some bonds. Let’s say that XYZ agrees to pay a coupon rate of 6% annual interest. Bond traders would call these bonds the “XYZ sixes of ’45.” (XYZ will pay 6% interest and repay the loan in 2045.) No matter what happens to interest rates over the next 30 years, XYZ is obligated to pay investors 6% per year on these bonds. No more. No less. If you purchase one of these new XYZ bonds, you will receive $60 per year from XYZ on your $1,000 investment (6% times $1,000). Since bond interest is usually paid twice a year, you would receive two checks for $30 spread six months apart.

The simplest transaction would work this way. Assume that when XYZ first sells its bonds (through selected brokerage firms), you buy one of these brand-new bonds at par value. In effect, you lend XYZ $1,000. You collect $60 interest every year for 30 years. It doesn’t matter how high or how low interest rates might move during this period, you’re still going to get $60 a year because that was the deal that you and XYZ agreed to. Finally, in 2045, XYZ pays back your $1,000. You made no gain on the value of the bond itself; your profit came solely from the steady stream of fixed income you received over the 30 years.

XYZ bond risk #1: You might not get all your money back

The pros call it “credit risk” because you’re depending on the creditworthiness of the borrower. You’re taking the risk that the issuer of the bond might go into default. This means the borrower is not able to keep up its interest payments or even pay off the bonds when they mature. This is the worst-case scenario that faces all bond investors.

To help evaluate this risk, ratings are available that help determine how safe the bonds are as an investment. Standard & Poor’s and Moody’s are the two companies best known for this. There are nine possible ratings a bond can receive. Most bond investors limit their selections to bonds given one of the top four ratings — AAA, AA, A, and BBB. As you might expect, the lower the quality, the higher the rate of interest investors demand to reward them for accepting the increased risk of default. (While these ratings are the best readily-available measure of a bond’s safety, be aware that these ratings proved to be unreliably optimistic for a small number of high-profile companies during the 2008 financial crisis.)

By definition, all other domestic borrowers are less creditworthy than the U.S. government. Therefore, borrowers who are in competition with the federal government for your money must pay you more to give you an incentive to lend to them instead of Uncle Sam. That’s why U.S. Treasury bills (most commonly 90-day IOUs) establish the floor for interest rates. Other rates are higher than the T-bill rate depending on how creditworthy the borrower is.

Returning to our earlier example, if XYZ gets into trouble due to poor management and earnings, its ability to pay off its bond debts may come into question. Assume its quality rating is lowered from AAA to A, and that shortly thereafter you need to sell your XYZ bond to meet an unexpected expense. A buyer of your bond will now want a greater potential profit to reward him for the greater perceived risk of default. As a practical matter, it may seem to be a very minor increase in risk, but the buyer will want compensation nevertheless.

But remember, the interest that XYZ pays on these bonds is fixed at $60 per year and can’t be changed. The only way anyone buying your bond can improve his profit potential is if you will lower the price of your bond. Then, in addition to the interest received from XYZ, the buyer will also reap a profit when he ultimately collects $1,000 (if all goes well) for a bond he bought from you for only, say, $900.

Thus, as the quality rating of a bond falls, sellers must lower their asking prices to make the bond attractive to potential buyers. Always remember that a bond can become completely worthless if the issuer gets into financial difficulty and defaults.

How can you minimize the credit risk? One way to virtually eliminate it is to stick solely with U.S. Treasuries. The drawback, however, is that because U.S. government bonds are regarded as the world’s safest fixed-income investments, the interest rates they pay investors are lower than those of corporate bonds. The most common way to minimize the credit risk is to add safety through diversification. Spread your holdings out among many different bond issues. That’s one of the primary advantages of investing in bonds through a mutual fund.

XYZ bond risk #2: Getting locked into a below-market yield

This is referred to as the “interest-rate risk.” It’s the same dilemma you face when trying to decide how long you should tie up your money in a bank CD, but it has even greater significance when investing in bonds. If you invest in a two-year CD and it turns out that rates go up and a six-month CD would have given you more flexibility to take advantage, you’re only missing out on better rates for 18 months. Try making that 18 years, and you get an idea of how painful it can be to hold long-term bonds during a period of rising interest rates when new bonds are being issued with higher coupon rates.

A fear of inflation leads to rising long-term interest rates. Just for the moment, assume that you’re back in 1980 and inflation is running at 12% per year. Now ask yourself this question: Would you be willing to pay full price for a 30-year Treasury bond with an 8% coupon rate? Not likely. A $1,000 bond would be paying you only $80 in interest per year at a time when you need $120 just to keep up with inflation. You’d be agreeing to a deal that would guarantee you a loss of purchasing power of $40 each year. Eventually, you’d get your $1,000 back, but it wouldn’t buy nearly as much in the future as it does now.

But what if the seller would lower the price of the bond so you could buy that bond at a big discount? If you only had to pay $665 for a $1,000 bond, it might make economic sense. The $80 interest per year — remember, the coupon rate stays fixed throughout the life of the bond — would represent a 12% return ($80 received in interest divided by the $665 invested). Now, at least you’re even with inflation. Plus, when the bond matures down the road, you get a full $1,000 back for your $665. That’s 50% more than you paid for it.

So you can see that high inflation (or even the fear of high inflation) causes bond buyers to demand a higher return on their money to protect their purchasing power. And to create that higher return, bond sellers must lower their asking prices. That’s why the bond market usually goes down when any news comes out that could reasonably be interpreted as leading to higher consumer prices. And it’s why bonds tend to perform so well when inflation expectations are low, as has been the case in recent years.

Here’s how this affects your XYZ bond. Although you originally intended to hold onto your XYZ bond for the full 30 years, real life is rarely quite that simple. Very few investors hold onto their bonds for so long a period of time. Let’s say that you decide to sell your XYZ bond and use the money to take the family to the beach this summer. You want your money back now, not in 2045.

Where do you sell it? In the bond market where older bonds (as opposed to new ones just being issued) are traded. Your broker can handle it for you. Assuming that XYZ is still in tip-top financial condition with an AAA credit rating, you might expect to get all of your $1,000 back. Well, maybe you will, and maybe you won’t. The big question is: what is the rate of interest being paid by companies that are now issuing new bonds?

If the rate of interest being paid on new bonds is higher than what your bond pays, you’ve got a problem. Assume that interest rates have gone up since you bought your XYZ bond, and that new bonds of comparable quality are now paying 7%. Why would any investor want to buy your old XYZ bond that will pay him only $60 per year in interest when, for the same price, he can buy a new one that will pay $70? Obviously, he wouldn’t. So, to sell your bond you will have to reduce your asking price below $1,000 to be competitive and attract buyers.

On the other hand, if interest rates have fallen, to let’s say 5%, then the shoe is on the other foot. Your old bond that pays $60 per year looks pretty attractive compared to new ones that pay only $50. This means you can sell it for a “premium,” meaning more than the $1,000 par value you paid.

Here’s the lesson: anytime you sell a bond before its maturity date, it will either be worth more than you paid for it (because interest rates have gone down since you bought it) or worth less than you paid for it (because interest rates have gone up since you bought it). That’s why it’s possible to lose money even with investments like U.S. Treasury bonds. For example, the average long-term government bond temporarily lost approximately -11% in only three months during the summer of 2013 as the Fed began talking about ending its stimulative Quantitative Easing program. In that case, just the prospect of higher future interest rates was enough to cause the bond market to decline sharply. Treasuries are safe from default, but no bond can fully protect you against rising interest rates unless you hold it until it reaches maturity. That’s why if you hold onto your XYZ bond until 2045, it will be worth $1,000. At that time, XYZ will repay the par value to whoever owns its bonds.

However, the longer you must wait until maturity, the longer you are vulnerable. The closer you get to a bond’s maturity date, the more the bond’s price reflects its full face value. That’s why interest rates eventually lose their power to affect the market value of a bond. How can you shorten the wait and reduce the risk? Buy old bonds that were issued many years back and are now only a few years from their maturity. There are “short-term” bond funds that specialize in just such securities. The shorter the maturity, the less volatile a bond’s (or bond fund’s) price will be.

Buying bonds through mutual funds

There are many varieties of bonds. You can choose from among high-quality bonds or higher-risk, higher-yielding ones of lower quality. You can vary the maturities — seeking to keep your average maturities at four years or less, or going for better yields (and more risk) with maturities of 20 years or more. The interest paid on some bonds is tax-free, and for others the interest is taxable. Some bond investors limit themselves to the U.S. market, whereas others invest overseas. Now imagine that you started mixing and matching all these possibilities to see how many different combinations are possible. The answer? A lot!

Why worry about all this when you can have a professional bond manager put together a portfolio for you? Investing in a pre-assembled portfolio via a bond fund offers convenience and professional management, plus you get great diversification which adds to safety. But there is one drawback you should know about — bond funds never reach maturity. Whereas the diversification you get in a bond fund lowers risk, the lack of an ultimate maturity date increases risk, Here’s why.

The job of the bond fund manager is to maintain the average maturity of the fund’s portfolio at the level stated in its prospectus. For example, look at our three recommended bond funds on page 26. Note their “duration,” third column from the right. Duration is expressed in years, similar to the maturity date, but one that additionally takes into account the interest being received along the way. The duration of a bond fund can tell you roughly how much its value is likely to change in response to a change in interest rates. For every percentage point (1%) change in interest rates, the fund’s value will move in the opposite direction by a percentage roughly equal to the fund’s duration. For example, our recommended short-term bond fund, BSV, recently had an average duration of 2.7. This duration figure means that if interest rates were to rise one percent this year, the value of the bonds in this fund would fall approximately 2.7%. As with the maturity date, the longer the duration, the greater the risk of the bond fluctuating in value.

Each of the three current recommendations is tailored to either a short-, medium-, or long-term emphasis. As time goes by and bonds get closer to their maturity dates, the portfolio manager will replace some of the shorter-term bonds with longer-term ones in order to keep the average within the stated range. That’s why, although time is passing, bond funds never get close to a day when the entire portfolio matures and cashes out whole. There is no final maturity date when all the IOUs in the portfolio will be paid off, and thus no guarantee you’ll get all of your investment back.

This is different from what takes place if you buy an individual bond. Assume you invest in a bond that has a 15-year maturity. Each year, it moves closer to the date when it will be paid off. That means the tendency of your bond to experience wide price swings in its current market value (due to fluctuations in interest rates) is reduced year by year. Eventually, there will come a time when you will receive all your money back. This is not an assurance that investors in most bond funds have.

SMI’s approach to bond investing

All of this naturally leads to the question, what maturities should you buy, particularly in light of today’s incredibly low (by historical standards) interest rates? SMI’s latest answer to this question was provided last month in the article detailing our new bond Upgrading approach. After relying on Vanguard bond index funds for a number of years, SMI introduced a couple of actively managed funds to our Upgrading lineup in 2014. This shift was begun in anticipation of what many expect to be a rising interest-rate environment over the next several years.

However, those rising interest rates have yet to materialize. With much of the global economy struggling under the weight of massive debt loads and unfavorable demographic trends, it’s an open question whether the next few years will involve higher interest rates — as most experts have expected, and continue to expect — or whether these deflationary forces will keep interest rates low for a while longer.

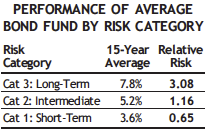

It’s a crucial question, given the significantly higher returns and risk involved with longer-term bonds. Both of these facts are illustrated in the table. Long-term bonds have provided significantly better returns, but there’s little question that they will suffer much more when interest rates finally start rising. Because of this uncertainty, our desire was to move away from the fixed bond allocations SMI has utilized in the past. We found what we believe will be an effective way to do so by implementing an Upgrading approach to the bond market that will rotate part of our bond holdings among bond funds of different types and maturities. This Upgrading recommendation is paired with constant allocations to Vanguard’s short-term and intermediate-term index funds, which provide a core of stability to our bond portfolios.

It’s a crucial question, given the significantly higher returns and risk involved with longer-term bonds. Both of these facts are illustrated in the table. Long-term bonds have provided significantly better returns, but there’s little question that they will suffer much more when interest rates finally start rising. Because of this uncertainty, our desire was to move away from the fixed bond allocations SMI has utilized in the past. We found what we believe will be an effective way to do so by implementing an Upgrading approach to the bond market that will rotate part of our bond holdings among bond funds of different types and maturities. This Upgrading recommendation is paired with constant allocations to Vanguard’s short-term and intermediate-term index funds, which provide a core of stability to our bond portfolios.

At present, SMI’s bond Upgrading recommendation is Vanguard’s long-term bond index fund. But if rates rise, the momentum scores of the various bond options will shift, and the built-in Upgrading mechanism will tell us to sell that fund and move into a different, presumably lower-volatility, alternative. (Warning: don’t invest in this long-term bond index fund unless you are planning to keep up with SMI’s monthly bond upgrading recommendations! This is not a buy-and-hold-forever type of recommendation.)

In our Just-the-Basics strategy, we use a middle-of-the-road approach by investing in a bond fund that currently has a duration of just under six years. On the risk ladder, it falls into our intermediate-term bond group (bond Category 2). For the 15 years ending December 31, 2014, it generated an average annual return of 5.5%, right in line with the average for that group. Furthermore, it did so with less volatility.

And of course, our Dynamic Asset Allocation strategy also is invested in bonds at times. This strategy utilizes bonds somewhat differently, however, in that it will always utilize long-term bonds (when it calls for bonds at all). When DAA calls for exposure to a category, it wants that exposure to be pronounced! Of course, the protection within that approach is the ability to exclude bonds altogether when they aren’t performing well.