At the end of SMI’s June article, What the Flattening Yield Curve Says About the Economy and Markets, I wrote the following:

Despite the strong predictive track record of the inverted yield curve, every time it occurs a group of experts step up to explain why it doesn’t apply this time. This is predictable, given that the yield curve normally inverts while economic conditions are still strong.

Consider the last two times it happened, in early 2000 and late 2006. Both of those periods, like today, were periods of strong economic growth and optimism about the economic future.

So I was amused to note the following conclusion to Caroline Baum’s article, "The Fed’s verbal gymnastics include loads of back flips," when it popped up less than a week later:

My final bit of unintended humor from the May minutes was the Fed’s flirtation with the four scariest words in finance: This time is different.

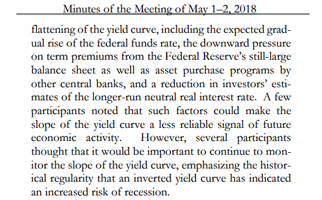

The reference was to the factors contributing to the flattening of the yield curve: specifically the Fed’s prior purchases of long-term Treasuries, which “could make the slope of the yield curve a less reliable signal of future economic activity.”

Don’t count on it.