Hank and Hannah Homeseeker are considering buying a $225,000 house. They’re currently renting for $1,300 per month. There are many factors that could sway their decision, but which decision would make the most financial sense?

To find out, we’ll make the following ownership assumptions (the numbers in Table A are close to the median national existing home price and 2-BR rental cost. Your local market is likely different — perhaps dramatically so. This article provides a framework for you to easily run numbers for your local area):

Time Period

Time Period

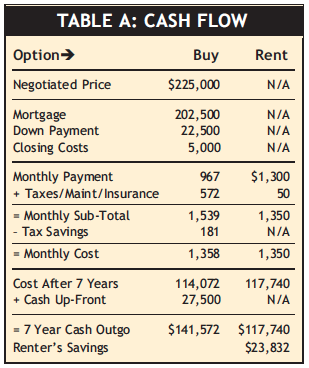

If they buy, they’ll stay put for at least seven years. Five years is generally the minimum amount of time homebuyers need to stay to recoup their closing costs. We’re extending their stay to seven years because that’s roughly the average length of time homeowners stay in a given home.Mortgage

They’re able to get a 30-year fixed rate loan at 4%, which would cost $967 per month.Up-front Costs

They have enough cash to put 10% down and also cover closing costs of $5,000. So, initial outlay would come to $27,500.Taxes/Ins/Maintenance

They’re budgeting $572/month. That includes: property taxes amounting to 1% of the purchase price, or $187.50 per month; homeowner’s insurance of $100 per month; private mortgage insurance (PMI) — since their down payment is less than 20% of the purchase price — amounting to .5% of the loan amount, or $84 per month; and $200 per month for maintenance and repairs.Tax Implications

Other than $10,000 in annual charitable contributions, the Homeseekers have no other tax deductions, so they’ve been taking the standard deduction (currently $12,600). If they buy, they can add $11,298 in deductions (property taxes $2,250, mortgage interest $8,035, and PMI $1,013) to the $10,000 in contributions (Congress has made PMI tax deductible through 2016, subject to certain income limitations). So, rather than taking the “standard deduction,” they could deduct a total of $21,298. Given their 25% tax bracket, this additional $8,698 in deductions ($21,298 minus the previously used $12,600 standard deduction) would save $2,175, or roughly $181 per month in taxes.

Renting, of course, does not come with a property-tax bill or private mortgage insurance. Let’s assume monthly costs of $25 for renter’s insurance and $25 for maintenance. We’ll also assume the rent increases 2.5% each year, so the “Cost After 7 Years” of $117,740 reflects that.

After crunching the numbers, the Homeseekers find their monthly housing costs would be only $8 more if they bought than if they continued renting ($1,358 vs. $1,350). That’s largely due to today’s low mortgage rates and the tax deductions available via ownership. Still, after seven years, owning in this scenario requires a Net Cash Outgo of $23,832 more than renting due to the down payment and closing costs.

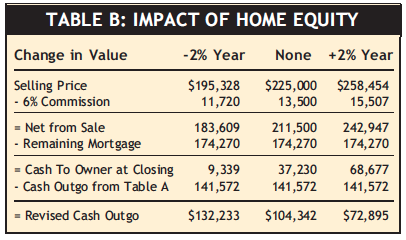

Owning builds equity

Now we need to factor in the impact of the equity created by making mortgage payments instead of rent payments. In Table B, we present three scenarios. The first column assumes the Homeseekers buy during a temporary peak in the housing market, and the home loses 2% of its value annually over the next seven years. The second column assumes the home’s value stays the same, and the third column assumes the home appreciates by 2% each year.

Let’s look at the first column in Table B, the one where the home loses value. After paying off their mortgage, the Homeseekers receive $9,339 at the closing. That partially offsets the $141,572 Cash Outgo (from Table A), leaving the couple with a revised cash outgo of $132,233 for the seven years of home ownership. Since this is higher than the Cash Outgo for renting for the same seven years of $117,740, renting would have cost much less than owning under this “home loses value” scenario. However, if the home retains or increases in value, the numbers seem to favor buying (the revised outgo numbers for the second and third columns are less than $117,740). But we’re not done.

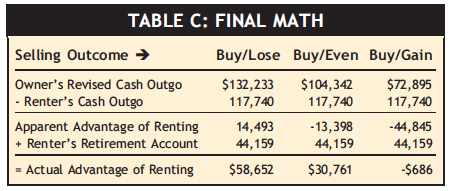

Investing the down payment money

There’s one final factor we need to account for: If the Homeseeker’s rent rather than buy, they could invest the $27,500 they would otherwise have spent for a down payment and closing costs. In Table C, we show how that would have grown to $44,159, assuming a 7% average annual return in a tax-advantaged retirement account.

After adding the value of that account, if they purchased a home that lost value over the next seven years (“Buy/Lose”) or simply maintained its value (“Buy/Even”), they would have come out ahead financially by renting instead (see the bottom line of Table C). Only if the home grows in value (“Buy/Gain”) would it have been financially advantageous to own—and even then, just barely.

Many moving parts

Of course, it’s impossible to know what will happen to home values in the future, and that unknown variable will play a key role in how this decision ultimately turns out.

Another significant factor is how much maintenance and repairs will cost if they buy. The $200 per month we budgeted would cover fairly standard needs — lawn care, minor plumbing or electrical issues, painting, etc. However, needing to replace the roof, air conditioner, or furnace would change the math quite a bit.

On the rental side, a higher monthly rental amount — for example, if they rented a house rather than an apartment — would quickly alter the outcome as well, tipping the scales more in favor of buying.

Of course, there are nonfinancial factors to consider as well. Some people derive greater satisfaction from owning. Others feel more freed up by renting since they don’t have to worry about the potential for expensive repairs and it gives them greater flexibility to move.

To be sure, this simple example doesn’t cover all the realities of the situation — lower interest deductions in later years, less favorable tax treatment of investing earnings, etc. It’s also worth considering how owning affects your flexibility in light of potential future job changes. If this is a decision you’re facing, run your own numbers and prayerfully decide, based on your particulars and assumptions, which path — renting or buying — is best for you.