The SMI strategies did a solid job of limiting losses during the first quarter of 2022, as the bear market we’ve anticipated since our January cover article kicked off. While most of SMI’s strategies registered small first-quarter losses, they were significantly less severe than the broader market.

Importantly, this occurred while our holdings were transitioning from a bullish market regime to a bearish one, the type of market turning point that is often the most difficult part of the cycle for our trend-following strategies. In light of that fact, it was a highly successful quarter.

Given all that has transpired in recent months — Russia’s invasion of Ukraine, record inflation, energy prices spiking, and so on — it’s easy to forget the S&P 500 index was still rising as the year began. It would register a new all-time high in early January, which meant our portfolios began the year positioned in the sectors that had been working over the bull run of the prior 18 months. The most obvious of which was large/growth stocks.

Thankfully, the SMI strategies had already picked up on declining momentum within the more speculative corners of the market, which helped us avoid the worst of the damage in smaller/growth stocks. And our bond positioning was on point as our strong tilt toward short durations and inflation protection helped immensely.

Just-the-Basics (JtB) & Stock Upgrading

Just-the-Basics posted the worst performance among the SMI strategies during the first quarter, and it’s not hard to see why. As an indexed portfolio, JtB lacks the ability to shift between various parts of the market, instead owning a fixed allocation of broad market exposure. Indexing tends to work fine during rising bull markets, but its limitations are exposed during bear markets.

JtB’s first-quarter loss of -6.7% was worse than the broad market’s -4.95% primarily due to its inability to distinguish between the growth side of the market, which had a terrible quarter, and the value side — which held up quite well.

A late-March rally rescued the S&P 500’s performance. The index had fallen as much as -13.7% from its January high but rebounded to end the quarter down “only” -4.6%. However, the quarter’s losses were worse for foreign stocks (-5.9%) and small-company stocks (-9.3%).

In contrast, Stock Upgrading successfully held its quarterly loss (-2.1%) to less than half that of the broad market (Wilshire 5000, -4.95%). It was able to accomplish this despite starting the year heavily overweight large/growth stocks, which hurt its performance during January before Upgrading pivoted sharply away from growth stocks and into value.

One reason Stock Upgrading was able to outperform during the quarter was that it had already sniffed out weakness among smaller growth stocks. As noted earlier, small-company stocks had a rougher first quarter than large-company stocks, and small/growth was the worst place to be. So it was extremely beneficial that Stock Upgrading had zero small/growth allocation during the quarter, having shifted all of its small-company exposure to value funds late last year.

To illustrate how important this growth/value distinction was, consider that the primary small/growth index (IWO) lost -12.7% during the first quarter, while the small/value index (IWN) lost just -2.5%. Upgraders endured some irritating flip-flops moving back and forth between growth and value during 2021 as COVID resurgences kept pumping the brakes on the global economic recovery. But the ability to shift our allocations between growth and value, introduced in the Upgrading revamp at the beginning of 2021, was added with the type of disparity we saw this quarter in mind. Being positioned with the dominant growth or value trend — and avoiding the laggard — can be a significant difference-maker at certain points in the market cycle.

The other huge first-quarter win for Stock Upgrading was its allocation to commodities, which gained a whopping +25.5%. To have that positive performance during a period when small-company (Russell 2000 index) and tech stocks (Nasdaq index) were slumping below the -20% bear market threshold (measured from their November highs) was extremely helpful to both our bottom line and morale!

Bond Upgrading

As tough as the quarter was for stock investors, it was even worse for bond investors, who finally woke up to the Fed’s increasingly strident “We will deal with inflation” message. The first quarter was the worst for bonds in decades, as the Bloomberg Aggregate Bond index fell -5.9% and longer-term bonds lost even more.

Ironically, all of this damage was inflicted despite the Federal Reserve making only one measly 0.25% rate hike during the quarter, and that not until March. But as is often the case, investors anticipated the Fed’s stronger actions to come, driving yields higher (and therefore prices lower).

Thankfully, Bond Upgrading dramatically limited losses during the quarter. While it was down -2.6%, that was less than half the loss of the broader bond market. The Upgrading-specific component lost just -0.7% during the quarter, the best performance of any bond product tracked within our Bond Upgrading universe (the static bond holdings that don’t change lost more).

It’s never pleasant losing money, especially in bonds, but Bond Upgrading was positioned as well as it possibly could have been. Unfortunately, the first quarter was as bad as it gets for the bond market, as raging inflation (which hit 8.5% in March) revealed that the Fed was dramatically behind the curve in raising interest rates from near-zero.

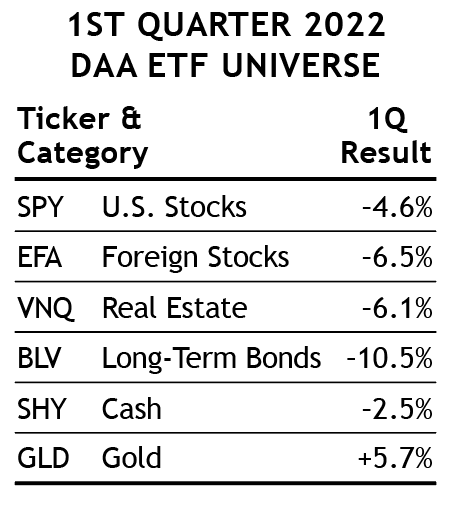

Dynamic Asset Allocation (DAA)

DAA’s loss of -4.5% for the first quarter was a little better than the broad market’s loss of -4.95%. The fact that it wasn’t even better is due primarily to the dynamic mentioned at the beginning of the article — DAA started the year positioned aggressively, based on the strong market trends of 2021. The transition during the quarter was clear, as DAA lost -5.8% in January (before it began to respond to the new bear market trends), -2.3% in February, and then gained +3.7% in March.

One of the more important moves of the quarter was DAA’s timely exit from Foreign Stocks at the end of January. That meant we were safely out of harm’s way when Russia invaded Ukraine later in February, which was especially painful for European markets. Along the same lines, another asset class that DAA didn’t own — Long-Term Bonds — had a miserable quarter, which DAA successfully side-stepped.

Gold chipped in a modest March gain after being added at the end of February. But DAA’s deliberate trend-following process was the key factor in the strategy ending the quarter so strongly in March, as both U.S. Stocks and Real Estate were retained despite weakness during January and February. U.S. Stocks may not survive much longer given the bearish market tilt, but Real Estate often is an outperformer during periods of market weakness. Given that bonds have been so unusually weak, it could be that Real Estate sticks around longer than normal despite the broader declining trends.

Sector Rotation (SR)

Starting the year in semiconductor stocks hurt SR during the first leg of the stock market decline in January. But a pivot into energy stocks for February and March produced a huge boost for this strategy, particularly after the Russian invasion of Ukraine lit a fire under energy prices. SR gained +8.3% in February and followed that up with a further +9.5% in March to end the quarter up slightly at +1.9%. That’s not a huge gain, but it was solid relative to the losses of the broader stock market and SR’s dramatic repositioning.

50/40/10

This portfolio refers to the specific blend of SMI strategies — 50% DAA, 40% Upgrading, 10% Sector Rotation — discussed in our April 2018 cover article, Higher Returns With Less Risk, Re-Examined. It’s a great example of the type of diversified portfolio we encourage most SMI readers to consider. (Blending multiple strategies adds complexity. Some SMI members may prefer an automated approach, such as offered by SMI Private Client.)

Given that all three of the component SMI strategies beat the broad market during the first quarter, it’s no surprise that this portfolio blend limited losses effectively, declining -2.9% vs. the market’s -4.95%. That’s not amazing performance, but as we’ve explained above, this was done while repositioning each of the strategies for what we suspect is more market downside to come.

Conclusion

While we don’t like ending on a negative note, it’s appropriate to reiterate our concerns regarding what comes next for markets. We’ve consistently pointed to the second and third quarters of this year as the likely point at which the Fed’s dilemma would become clear. After a dozen years of using monetary policy to drive the prices of financial assets — both stocks and bonds — to unprecedented heights, and after failing to respond in a timely manner to rapidly rising inflation last year, the Fed finds itself choosing between various bad options.

In recent decades, when the Fed tightened financial conditions, it was able to reverse its policy whenever the stock and/or bond market started to crack. This flexibility was largely possible due to the absence of inflation in the broader economy. Today, facing CPI inflation of 8.5% with a Fed Funds rate of just 0.5%, the Fed is woefully behind the curve, and crucially lacks this flexibility to change course, if markets begin to fall, without further inflaming the inflation problem.

As a result, it seems likely that at some point the Fed will have to choose between trying to save the financial markets from falling prices or saving the economy from the elevated inflation that already is crushing the general public. There’s little doubt which path they are gearing up for, which means investors need to brace for pain should the market deteriorate further, as the Fed isn’t likely to come to the rescue.

The probable catalysts for the next phase of the bear market are already in view. The Fed has already communicated its intention to begin “Quantitative Tightening” (selling bonds back into the market; i.e., shrinking the Fed’s balance sheet, which is the opposite of the stimulative Quantitative Easing that helped propel markets higher over the past dozen years). Meanwhile, the second-quarter earnings season is likely to be characterized by lower forecasts as impossibly high expectations collide with the reality of high inflation and softening economic growth.

The good news is that the SMI strategies are well underway in positioning for this bearish turn of events. Throughout the first quarter, SMI gradually shifted its holdings away from the types of more speculative growth stocks likely to suffer the most damage under this scenario, while moving into asset classes that may benefit as investors recognize the market outlook has changed in the quarters ahead. The bear market of 2000-2002 was largely a rotation out of tech/growth stocks and into previously ignored value stocks. We think similar dynamics could be in play again and saw evidence of this during the first quarter.

However the market trends may unfold from here, we’ll be watching closely and responding accordingly. Our disciplined approach of incrementally adjusting the risk exposure of our portfolios has paid off so far this year, and we’re confident those benefits will only expand should this bearish outlook materialize. On the other hand, if the market bounces back more strongly than we anticipate, we should be able to pivot back quickly, given that we haven’t shifted to an overly dramatic bearish posture (for example, by selling everything and moving to the sidelines).

Investors have faced a gauntlet of challenges over the past two years: COVID, economic shutdowns and reopenings, inflation, shortages, war, sanctions, soaring energy prices, and so on. The primary benefit of following a disciplined system such as SMI offers is clear: our process boils down all of these variables into tangible price signals and tells us how to respond in real-time. This keeps us on the right side of the major trends — while freeing you from the burden of having to try to understand each of these market factors in depth in order to position your portfolio accordingly.

SMI’s approach has been battle-tested and proven through multiple market cycles and past bear markets. Hopefully, that gives you confidence that whatever the market throws at investors next, we’ll be equipped to handle it and respond appropriately.