I’ve had some direct member requests for comment regarding "the stimulus and other Congressional goings-on and how this might all play out in the market both short and long-term" (to quote one that came in this weekend).

I write infrequently about these political aspects for two reasons. One, they generally aren’t as important to the market direction as people think. And two, I hate doing it because it gets me riled up, and I know it gets many of you riled up, and that’s not our game. There are plenty of places trying to make a living off of that outrage, but we’re not one of them.

But since you asked...

In all seriousness, when I write about the political angle of investing, usually it’s to encourage SMI members to fade their political leanings and not to let those influence their investing decisions. It’s well documented how members of both major U.S. political parties get super optimistic about both the economy and the stock market when one of their own becomes president, and then get super pessimistic when the other party takes over. Yet there’s very little historical correlation in market performance between political parties.

That’s not to say the policy differences don’t matter, it’s just to say those differences don’t normally show up immediately enough to dictate what the right investment decisions today are.

So with that in mind, my very brief commentary on the current Congressional circus "goings-on" is as follows. As it pertains to the markets, raising the debt limit is pure theater. This comes up every so often, the party out of power at the moment makes a huge deal about it, and eventually the limit gets raised. I know that sounds cynical, but that’s what happens and while the drama can weigh on the market temporarily, it’s not much of a longer-term factor.

The huge spending package currently being debated is a big deal in terms of the broader borrowing/spending trend. We’ve reached the point where I don’t think anyone seriously expects we’re going to pay the national debt off in real terms. We’re not likely to default on it either. Which is why so many believe the most likely path is that we "soft default" on the debt by inflating it away over time.

So while there are important implications about what this trend means to our country, the specific market implications of this bill passing (and at what exact dollar amount) probably aren’t all that great. Whatever the final dollar amount is — whether that’s $1.5 trillion, $3.5 trillion, or something in between — it’s going to be spent over a long period of time, like the next 10 years. And when we look at that actual amount of incremental spending, it’s just hard to think it’s really going to move the needle much.

Consider the worst-case scenario where the full $3.5 trillion package passes (which I don’t think it will and hope it doesn’t). Rolled out over the next 10 years, that would be $350 billion of additional spending each year. We can round that up to $30 billion per month. Do you realize the Federal Reserve has been buying $120 billion in bonds every single month for the last year-and-a-half and simply adding them to their balance sheet? The much-discussed Fed "taper" dwarfs the market impact of this additional spending (which when all is said and done will likely come in at half that level or less).

This is why I absolutely believe these things matter (and are worth fighting about) on a political level, but don’t really move the needle much on the market level. It’s why I don’t spend a lot of time focusing on political events as market drivers. As was the case in 2009, if you got out of the market a year ago because you thought Joe Biden was about to ruin everything, you’ve missed a very lucrative year for investors.

Energy policy

Changing gears slightly, you can throw everything I just said out the window when it comes to energy prices. Because political choices are absolutely wreaking havoc in the energy markets and I don’t see that stopping. As investors, that absolutely IS something we should be paying attention to.

I don’t think it’s controversial to acknowledge the "green agenda" that seeks to reduce/eliminate the use of fossil fuels as quickly as possible. This is an international effort with many tendrils that include boosting investment in green alternative energies, limiting the availability of capital to fossil fuel producers, etc. It’s been going on for decades but has really been gathering momentum over the past several years, in governments as well as investment circles (via "ESG" mandates).

We would need a whole book to cover this subject adequately, so instead I’ll summarize in a single pithy statement: In the push to green the world’s energy supply, the reality of how much conventional energy will be needed and for how long has been drastically underestimated.

Today we’re seeing the impact of years of starving conventional energy producers of capital while making it as difficult as possible for them to do business. There has been extremely little new investment in oil/gas exploration and development over the past several years, while efforts to block new pipelines and access to new production sites have been relentless. It feels like an episode of the Twilight Zone watching the president do everything in his power to make it impossible to produce energy in the U.S., only to turn around and implore OPEC to pump more oil because we don’t have enough.

Lest anyone think I’m just picking on Biden or the Democrats here at home, this has been happening globally for some time now and the effects are being felt globally. Gas prices have skyrocketed recently in the UK, and China is reverting to dramatically higher coal usage (and prices) in the face of their own shortages. And winter isn’t even here yet.

Rather than causing a fundamental re-think of the current transition trajectory from "old" to "new" sources of energy, many are instead using the current shortages and disruption as a reason to push for even faster de-carbonization. This Washington Post article excerpt summarizes this point of view succinctly:

The data shows that renewable energy in its various forms is getting inexorably cheaper to produce. A new report from the Centre for Research on Energy and Clean Air found that electricity generated from zero-carbon emission sources helped reduce Britain’s and the E.U.’s gas bill by tens of billions of dollars. “Skyrocketing prices is an incentive to get out of fossil fuels,” Sanzillo said.

Leading European politicians preparing for COP26 concur. They believe that the transition to more renewable energies will in the long run help protect European customers from the vagaries of oil and gas markets. “The wrong response to this would be to slow down the transition to renewable energy,” Frans Timmermans, the E.U.’s climate chief, said at a meeting of environmental ministers this week. “The right response is to keep the momentum and perhaps even look for ways to increase the momentum.”

Secretary of State Antony Blinken echoed that rhetoric. “We’re in the midst of a lengthy transition to renewables of various kinds, away from fossil fuels,” he said during an interview Wednesday. “During that transition you can have challenging, bumpy patches before you actually get to the point where you have all of these renewable energies that are online and able to fill the gap.”

Regardless of how you or I might feel about this, we need to be clear-eyed about one thing: this is the path today’s current politicians are traveling. Expect to see even more of this following the U.N.’s COP26 climate summit at the end of this month.

Here’s how I interpret this as an investor. Normally, when I see something double in price in a year’s time, it makes me nervous about getting in at that level. But after watching the conventional energy-sector companies get crushed and starved for new investment over the past decade, it’s hard for me to imagine these energy price issues don’t get worse before they get better. And if I’m going to have to pay at the pump and to heat my house this winter, I may as well offset those costs in my investment portfolio.

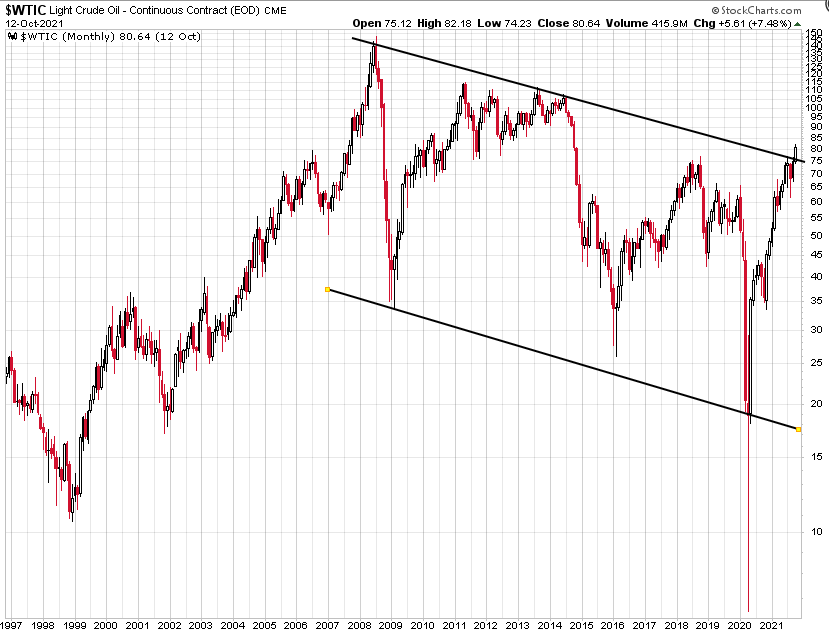

Here’s a long-term chart of U.S. oil prices:

Click Graph to Enlarge

I drew that channel on there, so don’t make too much of the specifics. I just wanted to illustrate the rough range oil has traded in since the 2008 peak. To my eye, after a dozen years of behaving itself within this downward sloping channel, oil is breaking out to the upside. I’m not a chartist, but looking at oil breaking above $80, I don’t see anything to suggest oil couldn’t be on its way to $100 or more. That’s +25% from here.

Here’s Natural Gas:

Click Graph to Enlarge

I’m sure I’m guilty of various chart crimes on this one, but again, given the current energy backdrop, why would $9 be out of the question here? Especially if we get a particularly cold winter, as some are predicting?

That’s certainly not to say these investments are without risk. One has only to look at the prior few times Natural Gas reached $5-$6 dollars on the chart above to see what happened next. Speculating in natural gas is a great way to become a millionaire...providing you start with $10 million!

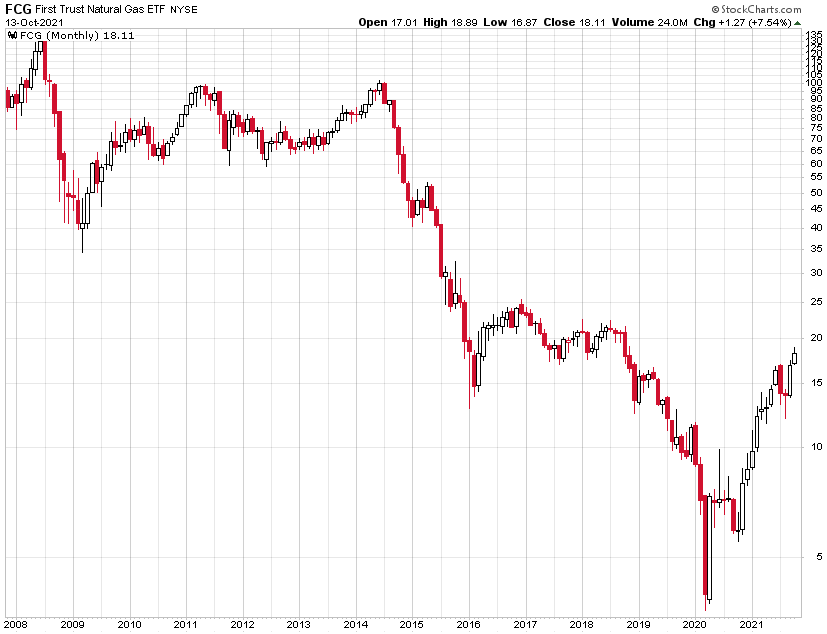

While I’m not inclined to speculate in the actual commodities (the strategy used within Upgrading to govern our commodities exposure invests directly in these commodity futures via the ETF we use there), the energy companies are certainly of interest. SMI members following Sector Rotation saw the top of those rankings increasingly dominated by these oil & gas funds at the end of September.

Here’s an ETF that tracks an index of natural gas companies. Note that while it’s up 3x over the past year, it still trades for less than one-fifth the valuation it had seven years ago.

Click Graph to Enlarge

More of the same

Make no mistake, pressure will continue to be applied to conventional energy companies. These green mandates aren’t going away, and the number of investment committees that divest of these carbon offenders is only going to increase. But when I see the current real-world mismatches in supply and demand and project a cold winter ahead, I see more opportunity than threat. (Full disclosure: SMI Private Client bought a few of these energy fund ETFs, including FCG, at the beginning of October as part of its expanded Sector Rotation implementation.)

These energy issues can’t be fixed with the snap of a politician’s fingers. There’s a difference between "real" stuff and the paper assets the Federal Reserve can push around on a moment’s notice. While much of today’s energy trouble is at least partially due to the unique problems with shipping and bottlenecks plaguing the rest of the economy, it’s also true that today’s troubles are the result of years of intentional decision-making. More importantly, there’s nothing to suggest the powers-that-be have changed their mind or are inclined to make different decisions going forward.

John F. Kennedy (perhaps incorrectly) popularized the idea that the word "crisis" in Chinese is made up of the characters meaning "danger" and "opportunity." We’ve got an energy crisis brewing and plenty of people are going to feel the danger if price trends continue in the present direction. But there’s also potential opportunity for those willing to bear the risk.

Keep an eye on upcoming Upgrading and Sector Rotation communications for official guidance related to these investments. (Upgraders already have some energy exposure via the currently recommended funds, but could get more direct exposure at month-end with a shift back into a direct commodities ETF.)