With Black Friday rapidly approaching, get ready for ads touting “0% financing.” From furniture marts to electronics retailers to home-improvement stores, 0% financing is a sales technique that is a proven winner — for sellers. For buyers? Well, it depends.

Bank credit cards also offer 0% deals, both for new purchases and balance transfers. In most cases, however, 0% credit cards work in a different manner than 0% in-store promotions. So it’s important to understand what kind of 0% deal you’re being offered.

The deferred-interest deal

Most 0% plans offered by retail stores are “deferred-interest” deals that involve applying either for a store-branded credit card or some other kind of in-store account. Deferred-interest deals typically involve “big-ticket” items, such as furniture, appliances, and even home-remodeling projects. (Deferred-interest arrangements are also common with “medical” credit accounts offered via doctors’ offices and other healthcare providers.)

The offer is simple: “If you pay for the purchase in full by the end of the promotional period, you’ll avoid all interest charges.” To be sure, such an offer can result in substantial savings (especially given typical retailer interest rates, which can run as high as 29.99% APR), but pay attention to the word “if”: “If you pay for the purchase in full by the end of the promotional period…”

In essence, deferred-interest deals are a race against the clock. Failure to pay the entire purchase price within the allotted time (typically 6, 12, 18, or 24 months) will result in interest being applied all the way back to the purchase date, regardless of how much you paid during the promotional period. Even if you pay 99% of the bill by the end of the designated period and come up just a few dollars short, the retailer will assess all the back interest.

That’s not the only way to have a deferred-interest deal go sour, however. In most cases, deferred-interest plans require the borrower to make at least minimum monthly payments during the promotional period. Miss a payment (or pay late) and the deal is off. The deferred interest will be assessed, just as if you had never signed up for a promotional plan — and the creditor may throw in a late-payment fee to boot.

There’s one more thing to watch out for. Because of how payments are applied, if you make additional purchases on the store-branded card — i.e., in addition to the special-financing purchase —you’ll increase the likelihood of not being able to pay off the promotional balance in time. By law (the Credit CARD Act of 2009), any payment greater than the minimum required payment will be applied first against higher-interest debt. So even if you make a large payment to pay down the promotional balance, a portion of that payment (perhaps most of it) will be applied against any other purchases you’ve made on the account. (Exception: During the final two billing cycles of a deferred-interest arrangement, payments above the minimum are applied to the promotional balance.)

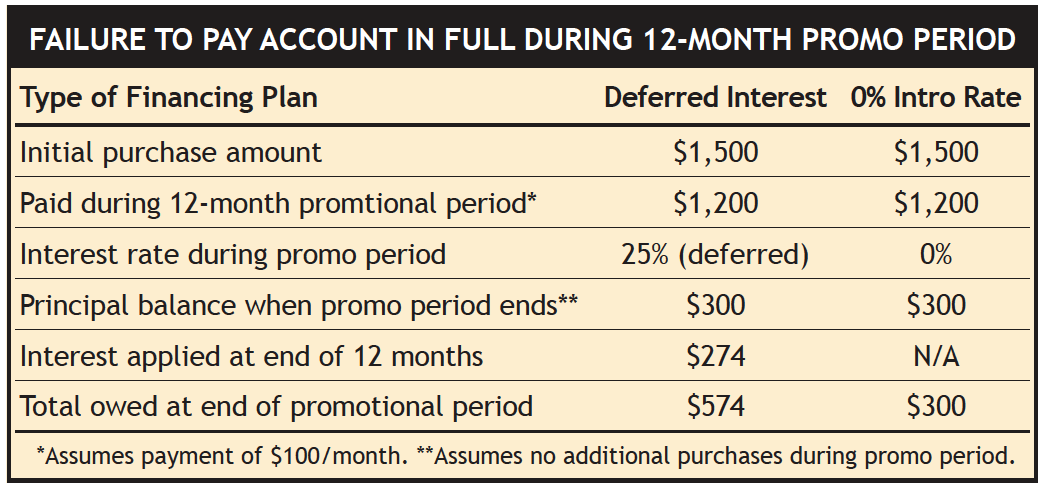

Click Table to Enlarge

The 0%-rate credit card

0% deals offered by bank credit-card issuers come in several permutations. “Balance-transfer” offers typically involve paying an upfront fee to move higher-interest debt to a new account that will assess no interest for a specified period (usually 12 to 18 months). Other 0% credit-card deals are “introductory” specials that charge no interest on new purchases for a specified period. (In some cases, card issuers combine a 0% balance-transfer deal with a 0% new purchases deal.)

The major difference between 0% in-store deals and 0% bank credit cards is that in most instances (read the fine print carefully!) bank-card offers don’t involve the possibility of incurring deferred interest. If an unpaid balance remains when the promotional period ends and the regular interest rate kicks in, the cardholder won’t be charged back interest.

The nearby table shows a comparison between a 12-month deferred interest deal and a similar 12-month introductory rate on a bank credit card. In both cases, the consumer made a $1,500 initial purchase and failed to pay the full amount by the end of the 12 months. But with the deferred-interest plan, the consumer owes a $274 in back interest at the end of the promotional period.

Let the buyer prepare

0% financing may work to your advantage if you pay close attention to the terms and act accordingly. Be we suggest you consider a 0% deal (especially if it’s a deferred-interest arrangement) only when the following are true:

1. You’re certain the price offered at 0% financing is the best deal around (the seller may be compensating for lost interest revenue by charging a higher price);

2. You have the full amount of the purchase price in savings already (that way, you’re not presuming you will have the money to make the payments — you do have the money);

3. You set up electronic reminders for when payments are due — especially the final payment! — so that you are sure to pay off your entire purchase amount on time.